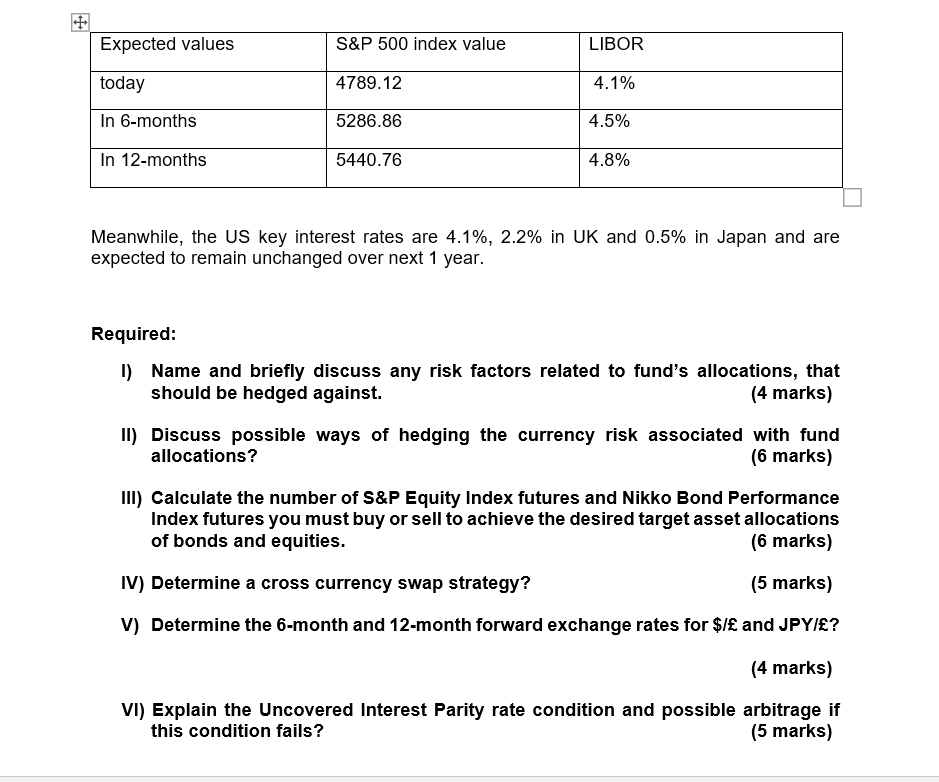

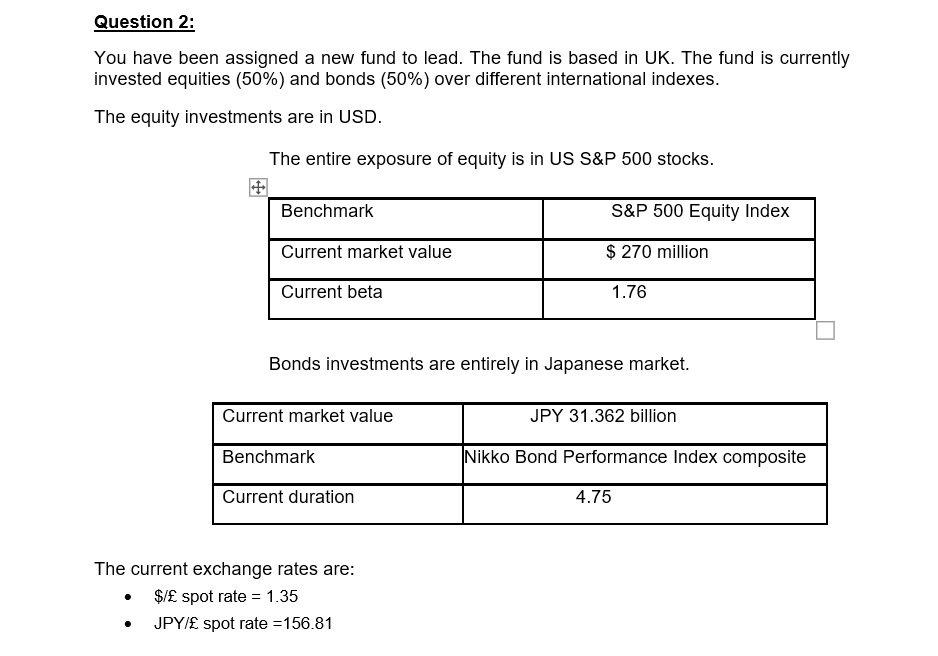

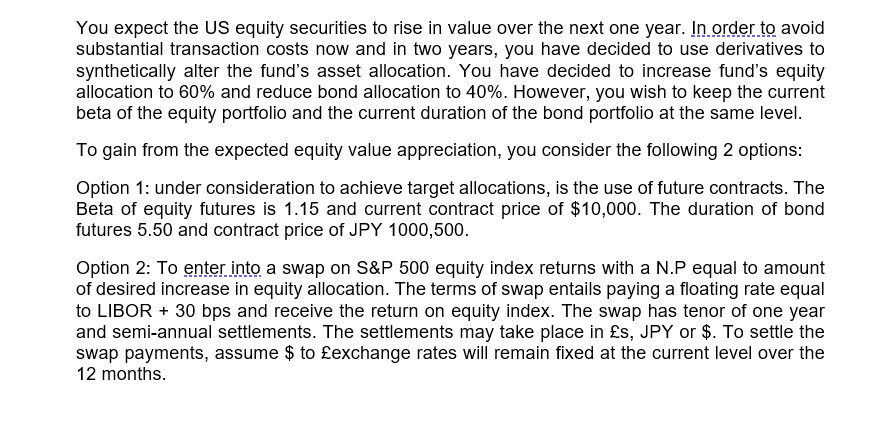

Question: Question no 1 Expected values S&P 500 index value LIBOR today 4739.12 4.1% In 6-months 5286.86 4.5% In 12-months 5440.76 4.8% Meanwhile, the US key

Question no 1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock