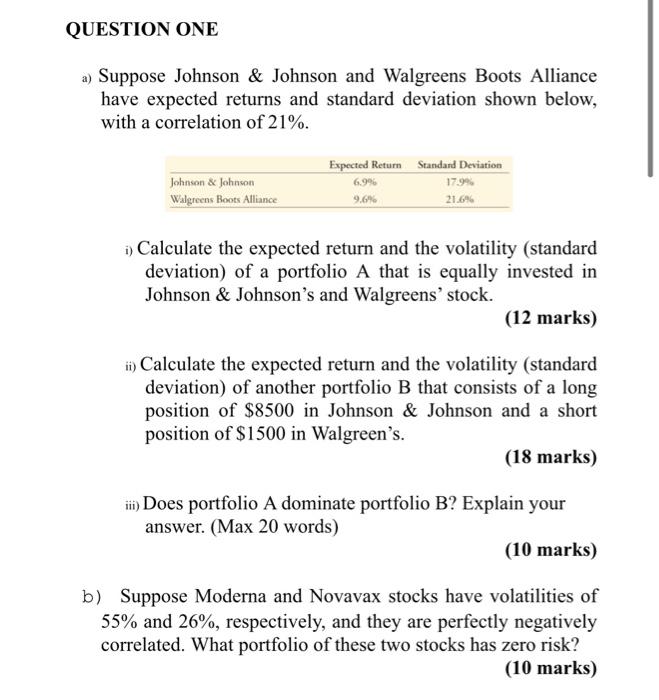

Question: QUESTION ONE a) Suppose Johnson & Johnson and Walgreens Boots Alliance have expected returns and standard deviation shown below, with a correlation of 21%. Expected

QUESTION ONE a) Suppose Johnson & Johnson and Walgreens Boots Alliance have expected returns and standard deviation shown below, with a correlation of 21%. Expected Return Standard Deviation 6.9% 17.9% Johnson & Johnson Walgreens Boots Alliance 21.6% i) Calculate the expected return and the volatility (standard deviation) of a portfolio A that is equally invested in Johnson & Johnson's and Walgreens' stock. (12 marks) ii) Calculate the expected return and the volatility (standard deviation) of another portfolio B that consists of a long position of $8500 in Johnson & Johnson and a short position of $1500 in Walgreen's. (18 marks) iii) Does portfolio A dominate portfolio B? Explain your answer. (Max 20 words) (10 marks) b) Suppose Moderna and Novavax stocks have volatilities of 55% and 26%, respectively, and they are perfectly negatively correlated. What portfolio of these two stocks has zero risk? (10 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts