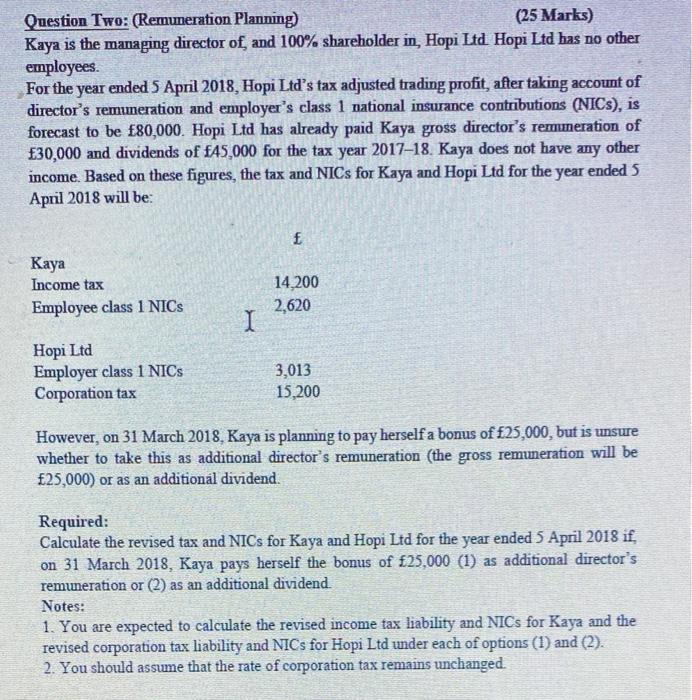

Question: Question Two: (Remuneration Planning) (25 Marks) Kaya is the managing director of, and 100% shareholder in, Hopi Ltd. Hopi Ltd has no other employees. For

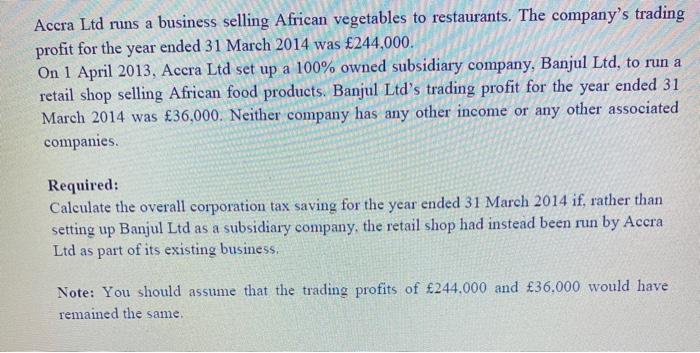

Question Two: (Remuneration Planning) (25 Marks) Kaya is the managing director of, and 100% shareholder in, Hopi Ltd. Hopi Ltd has no other employees. For the year ended 5 April 2018, Hopi Ltd's tax adjusted trading profit, after taking account of director's remuneration and employer's class 1 national insurance contributions (NICS), is forecast to be 80,000. Hopi Ltd has already paid Kaya gross director's remuneration of 30,000 and dividends of f45,000 for the tax year 201718. Kaya does not have any other income. Based on these figures, the tax and NICs for Kaya and Hopi Ltd for the year ended 5 April 2018 will be: f f Kaya Income tax Employee class 1 NICS 14,200 2,620 I Hopi Ltd Employer class 1 NICs Corporation tax 3,013 15,200 However, on 31 March 2018. Kaya is planning to pay herself a bonus of 25,000, but is unsure whether to take this as additional director's remuneration (the gross remuneration will be 25,000) or as an additional dividend. Required: Calculate the revised tax and NICs for Kaya and Hopi Ltd for the year ended 5 April 2018 if, on 31 March 2018, Kaya pays herself the bonus of 25,000 (1) as additional director's remuneration or (2) as an additional dividend. Notes: 1. You are expected to calculate the revised income tax liability and NICs for Kaya and the revised corporation tax liability and NICs for Hopi Ltd under each of options (1) and (2). 2. You should assume that the rate of corporation tax remains unchanged. Accra Ltd runs a business selling African vegetables to restaurants. The company's trading profit for the year ended 31 March 2014 was 244,000. On 1 April 2013, Accra Ltd set up a 100% owned subsidiary company, Banjul Ltd, to run a retail shop selling African food products. Banjul Ltd's trading profit for the year ended 31 March 2014 was 36,000. Neither company has any other income or any other associated companies. Required: Calculate the overall corporation tax saving for the year ended 31 March 2014 if, rather than setting up Banjul Ltd as a subsidiary company, the retail shop had instead been run by Accra Ltd as part of its existing business. Note: You should assume that the trading profits of 244.000 and 36,000 would have remained the same. Question Two: (Remuneration Planning) (25 Marks) Kaya is the managing director of, and 100% shareholder in, Hopi Ltd. Hopi Ltd has no other employees. For the year ended 5 April 2018, Hopi Ltd's tax adjusted trading profit, after taking account of director's remuneration and employer's class 1 national insurance contributions (NICS), is forecast to be 80,000. Hopi Ltd has already paid Kaya gross director's remuneration of 30,000 and dividends of f45,000 for the tax year 201718. Kaya does not have any other income. Based on these figures, the tax and NICs for Kaya and Hopi Ltd for the year ended 5 April 2018 will be: f f Kaya Income tax Employee class 1 NICS 14,200 2,620 I Hopi Ltd Employer class 1 NICs Corporation tax 3,013 15,200 However, on 31 March 2018. Kaya is planning to pay herself a bonus of 25,000, but is unsure whether to take this as additional director's remuneration (the gross remuneration will be 25,000) or as an additional dividend. Required: Calculate the revised tax and NICs for Kaya and Hopi Ltd for the year ended 5 April 2018 if, on 31 March 2018, Kaya pays herself the bonus of 25,000 (1) as additional director's remuneration or (2) as an additional dividend. Notes: 1. You are expected to calculate the revised income tax liability and NICs for Kaya and the revised corporation tax liability and NICs for Hopi Ltd under each of options (1) and (2). 2. You should assume that the rate of corporation tax remains unchanged. Accra Ltd runs a business selling African vegetables to restaurants. The company's trading profit for the year ended 31 March 2014 was 244,000. On 1 April 2013, Accra Ltd set up a 100% owned subsidiary company, Banjul Ltd, to run a retail shop selling African food products. Banjul Ltd's trading profit for the year ended 31 March 2014 was 36,000. Neither company has any other income or any other associated companies. Required: Calculate the overall corporation tax saving for the year ended 31 March 2014 if, rather than setting up Banjul Ltd as a subsidiary company, the retail shop had instead been run by Accra Ltd as part of its existing business. Note: You should assume that the trading profits of 244.000 and 36,000 would have remained the same

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts