Question: Question1. Question2 this all the information the professor provided. An investor buys, for a premium of 187.06, a call option on a non-dividend-paying stock whose

Question1. Question2 this all the information the professor provided.

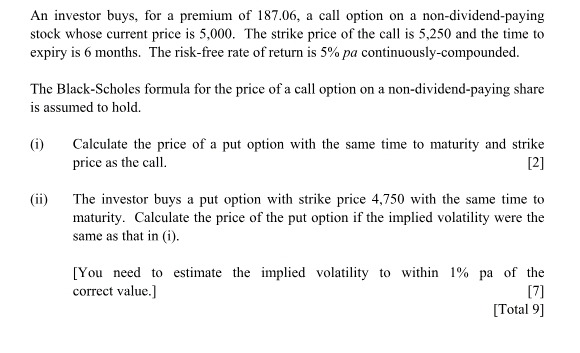

An investor buys, for a premium of 187.06, a call option on a non-dividend-paying stock whose current price is 5,000. The strike price of the call is 5,250 and the time to expiry is 6 months. The risk-free rate of return is 5% pa continuously-compounded. The Black-Scholes formula for the price of a call option on a non-dividend-paying share is assumed to hold. (i) Calculate the price of a put option with the same time to maturity and strike price as the call. [2] (ii) The investor buys a put option with strike price 4,750 with the same time to maturity. Calculate the price of the put option if the implied volatility were the same as that in (i). [You need to estimate the implied volatility to within 1% pa of the correct value. ] [7] [Total 9]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts