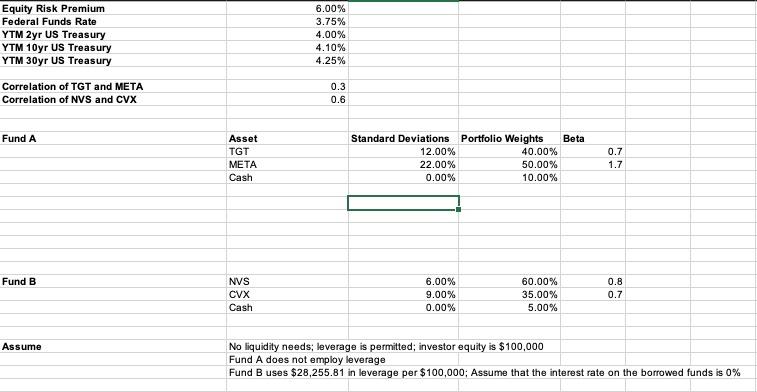

Question: Questions: 1. What is the expected return for each fund, to two decimal places? 2. What is the expected standard deviation for each fund? 3.

Questions:

1. What is the expected return for each fund, to two decimal places?

2. What is the expected standard deviation for each fund?

3. What is the Sharpe Ratio for each fund, assuming no leverage is employed?

4. Is there enough information to calculate the correlation between the two funds, if your client asked for it?

\begin{tabular}{l|l|} \hline Equity Risk Premium & 6.00% \\ \hline Federal Funds Rate & 3.75% \\ \hline YTM 2yr US Treasury & 4.00% \\ \hline YTM 10yr US Treasury & 4.10% \\ \hline YTM 30yr US Treasury & 4.25% \\ \hline \end{tabular} Correlation of TGT and META Correlation of NVS and CVX 0.3 Fund A \begin{tabular}{|l|r|r|r|} \hline Asset & Standard Deviations & Portfolio Weights & Beta \\ \hline TGT & 12.00% & 40.00% & 0.7 \\ \hline META & 22.00% & 50.00% & 1.7 \\ \hline Cash & 0.00% & 10.00% & \\ \hline \end{tabular} Fund B \begin{tabular}{|l|r|r|r|} \hline NVS & 6.00% & 60.00% & 0.8 \\ \hline CVX & 9.00% & 35.00% & 0.7 \\ \hline Cash & 0.00% & 5.00% & \\ \hline \end{tabular} Assume No liquidity needs; leverage is permitted; investor equity is $100,000 Fund A does not employ leverage Fund B uses $28,255.81 in leverage per $100,000; Assume that the interest rate on the borrowed funds is 0% \begin{tabular}{l|l|} \hline Equity Risk Premium & 6.00% \\ \hline Federal Funds Rate & 3.75% \\ \hline YTM 2yr US Treasury & 4.00% \\ \hline YTM 10yr US Treasury & 4.10% \\ \hline YTM 30yr US Treasury & 4.25% \\ \hline \end{tabular} Correlation of TGT and META Correlation of NVS and CVX 0.3 Fund A \begin{tabular}{|l|r|r|r|} \hline Asset & Standard Deviations & Portfolio Weights & Beta \\ \hline TGT & 12.00% & 40.00% & 0.7 \\ \hline META & 22.00% & 50.00% & 1.7 \\ \hline Cash & 0.00% & 10.00% & \\ \hline \end{tabular} Fund B \begin{tabular}{|l|r|r|r|} \hline NVS & 6.00% & 60.00% & 0.8 \\ \hline CVX & 9.00% & 35.00% & 0.7 \\ \hline Cash & 0.00% & 5.00% & \\ \hline \end{tabular} Assume No liquidity needs; leverage is permitted; investor equity is $100,000 Fund A does not employ leverage Fund B uses $28,255.81 in leverage per $100,000; Assume that the interest rate on the borrowed funds is 0%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts