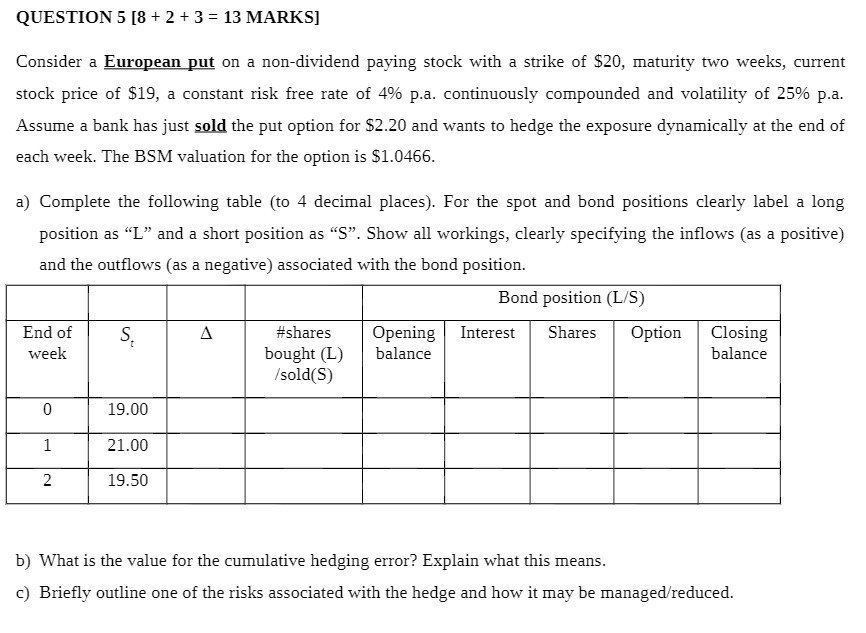

Question: QUESTIONS [8+ 2 + 3 = 13 MARKS] Consider a European put on a nondividend paying stock with a strike of $20, maturityr two weeks,

![QUESTIONS [8+ 2 + 3 = 13 MARKS] Consider a European](https://s3.amazonaws.com/si.experts.images/answers/2024/06/6667191ab42ec_6666667191a91d8e.jpg)

QUESTIONS [8+ 2 + 3 = 13 MARKS] Consider a European put on a nondividend paying stock with a strike of $20, maturityr two weeks, current stock price of $19, a constant risk free rate of 4% pa. continuously compounded and volatility of 25% p.a. Assume a bank has just sold the put option for $2.20 and wants to hedge the exposure dynamically at the end of each week. The BSM valuation for the option is $1.0456. a) Complete the following table (to 4 decimal places}. For the spot and bond positions clearly label a long position as \"L\" and a short position as \"S\". Show all workings, clearly specifying the inflows [as a positive) and the outows [as a negative) associated with the bond position. End of SE Opening Interest Shares Option Closing week balance balance b) What is the value for the cumulative hedging error? Explain what this means. c) Briey outline one of the risks associated with the hedge and how it may be managedr'reduced

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts