Question: Questions and Problems: ( Note: students will be responsible for checking each question to make sure it is free of mistakes with regard to numbers

Questions and Problems:

Note: students will be responsible for checking each

question to make sure it is free of mistakes with regard to

numbers and information

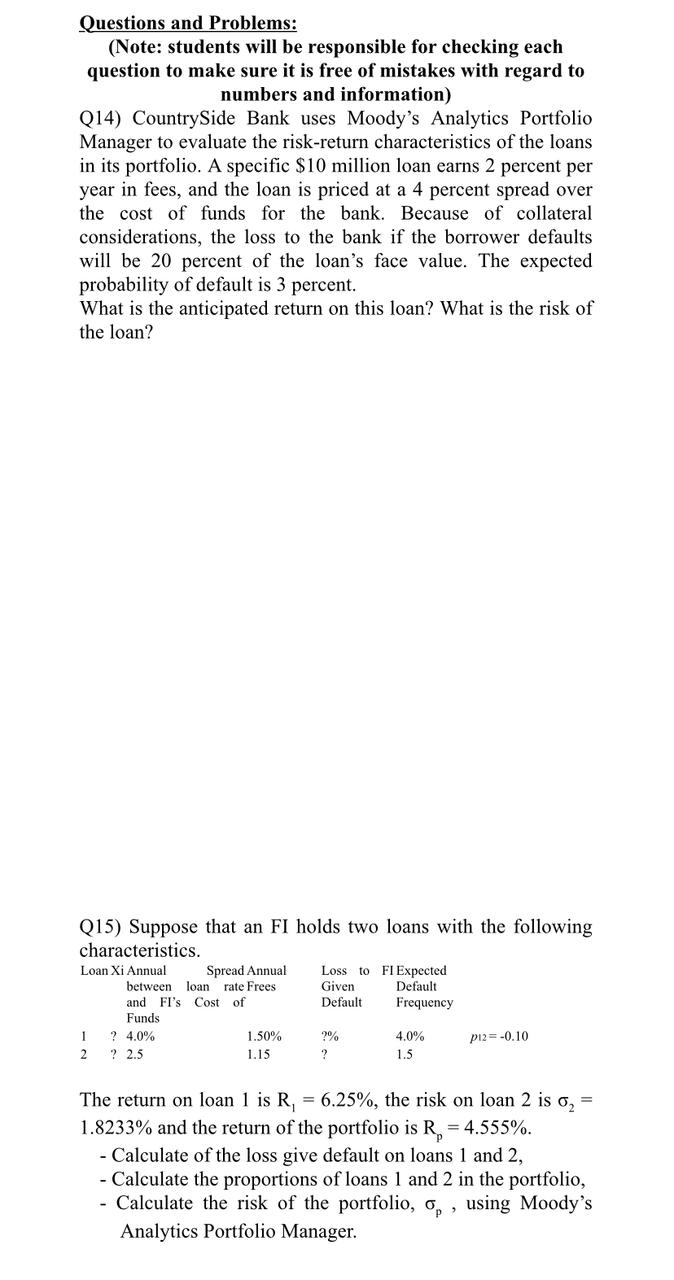

Q CountrySide Bank uses Moody's Analytics Portfolio

Manager to evaluate the riskreturn characteristics of the loans

in its portfolio. A specific $ million loan earns percent per

year in fees, and the loan is priced at a percent spread over

the cost of funds for the bank. Because of collateral

considerations, the loss to the bank if the borrower defaults

will be percent of the loan's face value. The expected

probability of default is percent.

What is the anticipated return on this loan? What is the risk of

the loan?

Q Suppose that an FI holds two loans with the following

characteristics.

The return on loan is the risk on loan is

and the return of the portfolio is

Calculate of the loss give default on loans and

Calculate the proportions of loans and in the portfolio,

Calculate the risk of the portfolio, using Moody's

Analytics Portfolio Manager.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock