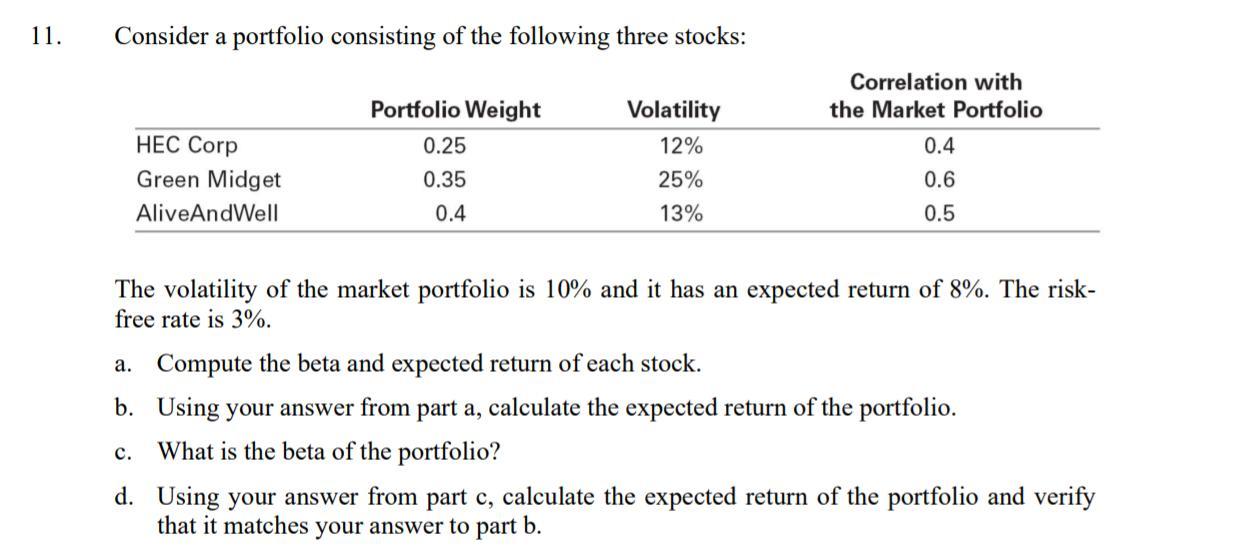

Question: 11. Consider a portfolio consisting of the following three stocks: Correlation with Portfolio Weight Volatility the Market Portfolio HEC Corp 0.25 12% 0.4 Green

11. Consider a portfolio consisting of the following three stocks: Correlation with Portfolio Weight Volatility the Market Portfolio HEC Corp 0.25 12% 0.4 Green Midget 0.35 25% 0.6 AliveAndWell 0.4 13% 0.5 The volatility of the market portfolio is 10% and it has an expected return of 8%. The risk- free rate is 3%. a. Compute the beta and expected return of each stock. b. Using your answer from part a, calculate the expected return of the portfolio. C. What is the beta of the portfolio? d. Using your answer from part c, calculate the expected return of the portfolio and verify that it matches your answer to part b.

Step by Step Solution

There are 3 Steps involved in it

To address the question properly lets compute the required values stepbystep a Compute the beta and expected return of each stock Beta calculation The ... View full answer

Get step-by-step solutions from verified subject matter experts