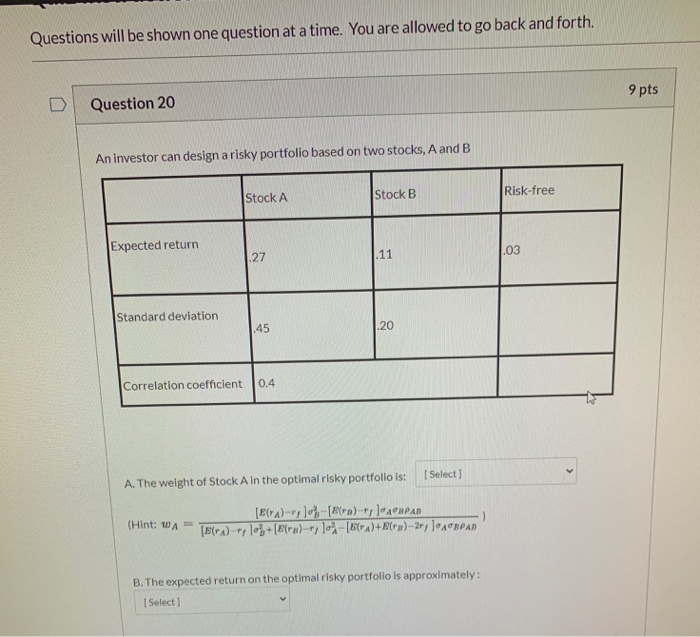

Question: Questions will be shown one question at a time. You are allowed to go back and forth. 9 pts Question 20 An investor can design

Questions will be shown one question at a time. You are allowed to go back and forth. 9 pts Question 20 An investor can design a risky portfolio based on two stocks, A and B Stock A Risk-free Stock B Expected return .27 .11 .03 Standard deviation .45 .20 Correlation coefficient 0.4 [ Select A. The weight of Stock A in the optimal risky portfolio is: (Hint: WA [E()-10-[WEB), AUPAD [EX)--y loy+[E(ra)-102-[5(+2)+(ra)-2r, ATBPAD B. The expected return on the optimal risky portfolio is approximately: Select

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock