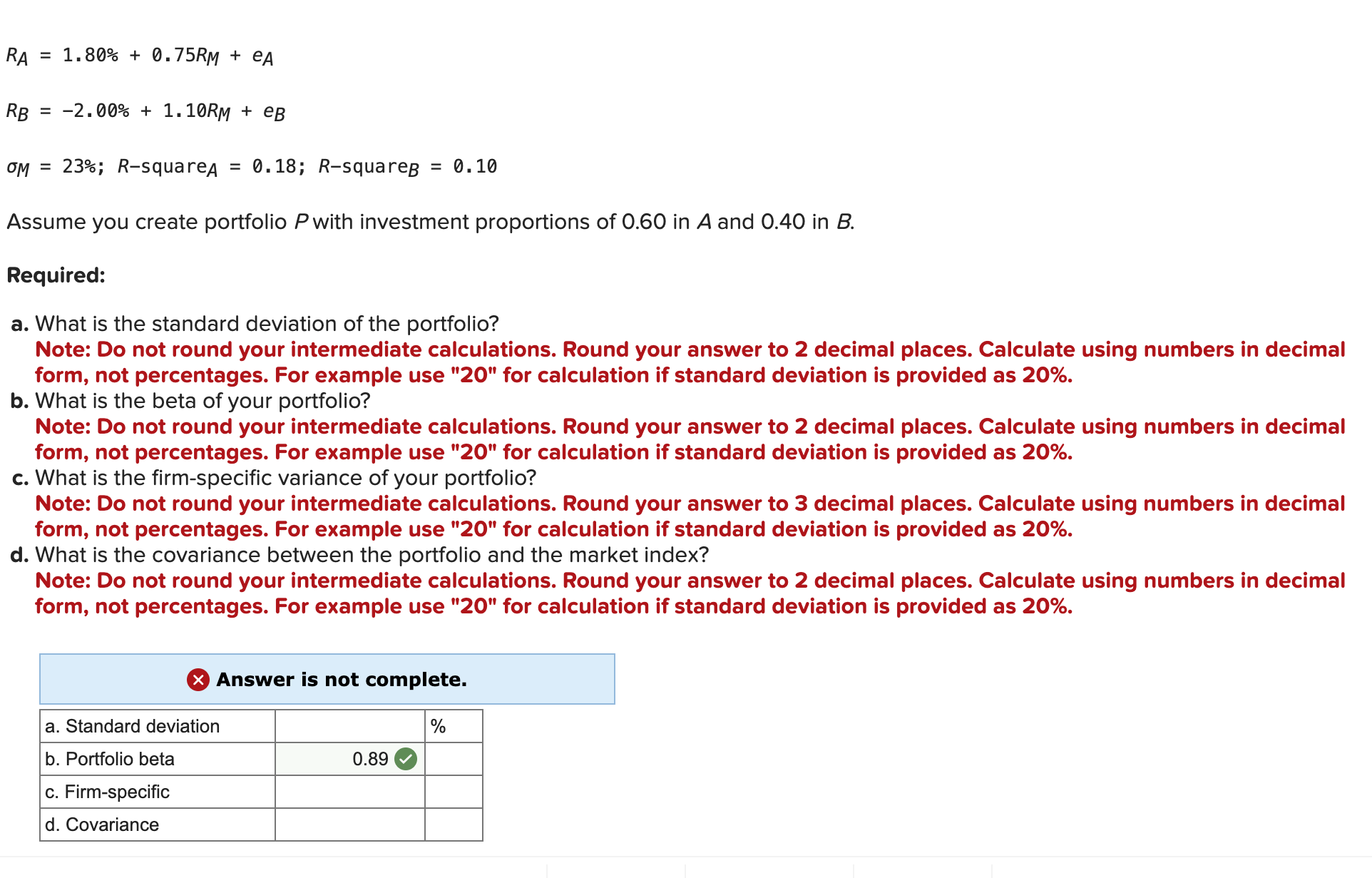

Question: RA = 1.80% + 0.75RM + A RB = -2.00% + 1.10RM + eB OM = 23%; R-square = 0.18; R-square = 0.10 Assume

RA = 1.80% + 0.75RM + A RB = -2.00% + 1.10RM + eB OM = 23%; R-square = 0.18; R-square = 0.10 Assume you create portfolio P with investment proportions of 0.60 in A and 0.40 in B. Required: a. What is the standard deviation of the portfolio? Note: Do not round your intermediate calculations. Round your answer to 2 decimal places. Calculate using numbers in decimal form, not percentages. For example use "20" for calculation if standard deviation is provided as 20%. b. What is the beta of your portfolio? Note: Do not round your intermediate calculations. Round your answer to 2 decimal places. Calculate using numbers in decimal form, not percentages. For example use "20" for calculation if standard deviation is provided as 20%. c. What is the firm-specific variance of your portfolio? Note: Do not round your intermediate calculations. Round your answer to 3 decimal places. Calculate using numbers in decimal form, not percentages. For example use "20" for calculation if standard deviation is provided as 20%. d. What is the covariance between the portfolio and the market index? Note: Do not round your intermediate calculations. Round your answer to 2 decimal places. Calculate using numbers in decimal form, not percentages. For example use "20" for calculation if standard deviation is provided as 20%. Answer is not complete. a. Standard deviation % b. Portfolio beta c. Firm-specific d. Covariance 0.89

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts