Question: Read the case study below and answer ALL the questions that follow. MANAGING RISK AND CAPITAL Banks have travelled a hard road since the global

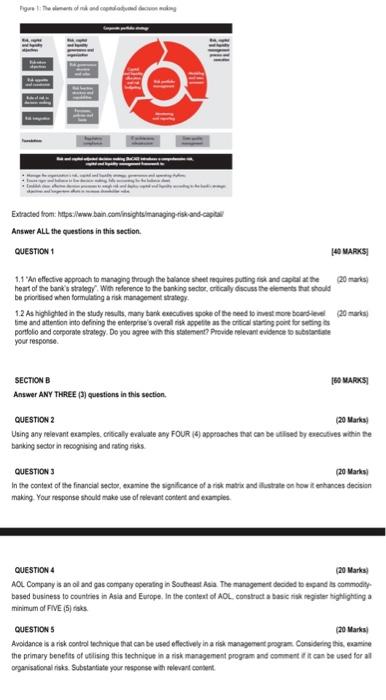

Read the case study below and answer ALL the questions that follow. MANAGING RISK AND CAPITAL Banks have travelled a hard road since the global financial crash of 2003 . They have had to weave their way through the wreckage of bad debt, volatile funding markets and an uncertain economic environment. Now, tough new nules under Basel III and a host of local regulations will require banks to significantly increase capital and adhere to stringent new liquidity and funding mandates. Meeting the new standards will put a big dent in banks' retum on equity and make it much harder for them to exceed their cost of capital. As banks begin to come to grips with these new realifes, many have been using an incomplete map to guide their business. The pursut of revenue and earnings growth with insufficient attention to the balance sheet ran them into a ditch. A comprohensive analysis by Bain \& Company of approximately 200 banks around the world and interviews with more than 50 senior executives at more than 30 global institutions reveal how banks are modifying a broad range of practices they relied on before the crisis in order to better compete in the new envircnment. During the pre-crisis years of benign credit conditions and readily available liquidity, the disciplines of managing the balance sheet atrophied, becoming the almost exclusive preserve at many institutions of a smal team of highly skilled technocrats working from corporate headquarters. Leading banis now recognize that the ablity to fully account for risk, capital and liquidity in line decisions will be a scurce of competive advantage. As they come to terms with how to strengthen balance sheet disciplines, bankers need to recognize the common set of challenges they face and the range of practices available to address them. In these executive surveys, t has been established that large differences in the understanding of risk, capital and liquidity and their implications on the balance sheet, both across business units and especially between the group-level functional specialists, on the one hand, and frontine commercial managers, on the other. This gulf reflects deeply ingrained habits and incentives that will be difficult to uproot. Distracted by the quarterly earnings drumbeat, senior group leaders and line executives often have had little motivation to think like balance sheet custodians. Because the organizabion's reward systarns are often aligned to the profitand- loss statement, critical qualibes of business judgment can be missing. Lacking incentives to focus on risk-and capitaladjusted results, commercial managers either pay token heed to captal deployment, or they rely on the metrics that "black box' models generate without fully understanding what they mean. To successfully navigate the difficult joumey ahead, industry leading banks are implanting better balance sheet management capabilities throughout the organization-and paricularly within their general management ranks. They recognize that there are no technical shortcuts. Whle strong, supporting technical expertise is necessary, in is not sufficient. If board members, senior executives and line managers do not anchor their business decisions in a risk-and capitaladjusted mindset, even the best technology does not count for much. An effective approach to managing through the balance sheet requires putting risk and capital at the heart of the bank's strategy, the objectives that management sets, how the organization is governed, and how the business is run and monitored on a daily basis. During the interviews, senior bank executives indicated that they were wrestling with how best to forge this joined-up view of the business, Many spoke of the need to invest more board-level time and attention into defining the enterprise's overall risk appetite as the critical starting point for setting its portlolio and corporate strategy. Others told us that they are redefining managerial roles and putting in place processes, policies and limits to give risk, capital and licuidity a central role in their bank's planning cycle. They described steps they were taking to shore up the structures, risk modeing and measurements, information technology and complance capabilities that are the underpinnings of the bank's core budgeting and management functions. Taken logether, the comments from bankers across the industry suggest that views are coalescing around new ways to think about running the bank with greater heed to the consequences of decisions on the balance sheet. They are best captured in common disciplines that form the connective tissue for a top-to-bottom system of risk and capilak-adjusted decision making (RaCADTM) (see Figure 1). This approach links the bank's overall stralegy into concrete cbjectives, governance and processes for managing risk, capital and liquidity at the level of each of its businesses, linked to the day-to- day decisions taken by operating managers. Extracted hom: hlps: lwww bain cominsights/managing-riskand-capla: Answer ALL the questions in this section. QUESTION 1 [4. MARxS] 1.1 'An effective approach to managing through the balance sheet requires puiting tsk and caplal at the 20 marks) heart of the bank's stradegy'. Wh reference to the banking sector, crtcally discuss the elenents fut should be priorised when formulating a risk management stratogy. 1.2As hyhlohted in fe study nesults, many bark entulives spoke of the need io mest mone board lenel: time and attention into defining the enberprise's overal rik appetie as he oritical surting point for seting is your fesponse. SECTION B Answer ANY TRREE (3) questions in this section, QUESTION 2 (20) Marks) Using any relevant examples. crically evaluate any FOUR (4) approsches that can be uclsed by treculives within Re barking sector in recogising and rating risis. QUESTION 3 (20) Marss) In the context of the financial sectse, examine the significance of a riek matrix and Ifustrate on bow it enhances decisian making. You response should rake use of relevant contert and examples. QUESTION 4 (20) Marks) ACC. Company is an ol and gas company operating in Southeast Asa. The managenert decided in tacand bs commotity" based business to countries in Asia and Eutope, In the contert of AOL. construct a basic risk negister highlighting a minimum of FNE (5) raks. QUESTION 5 (20) Marks) Avoidance is a risk, conterl technique that can be used eflectively in a risk management prograes. Considving this, enamiev the primary benefts of utlising this fechnique in a risk management program and comment it it can be used for all organisational risks. Substantiate your respotse with rolecant conbent

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts