Question: Read the WRDS Financial Ratios PDF document and write a 2page summary of what you understood and learned from the information therein. The MAXIMUM number

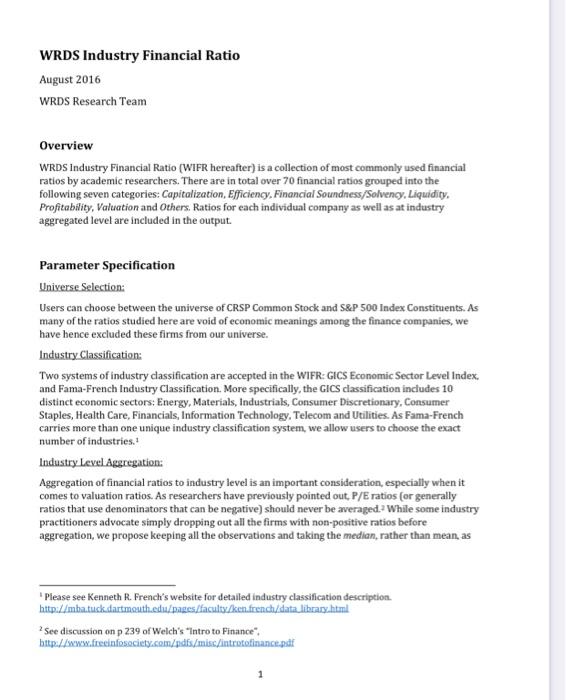

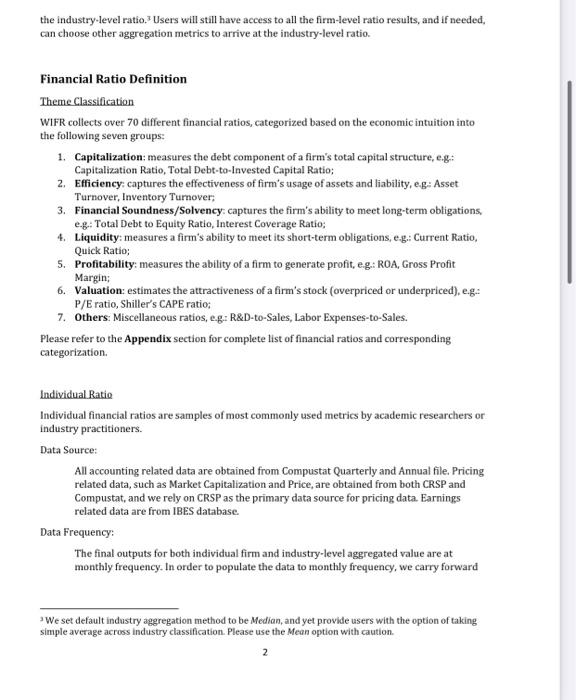

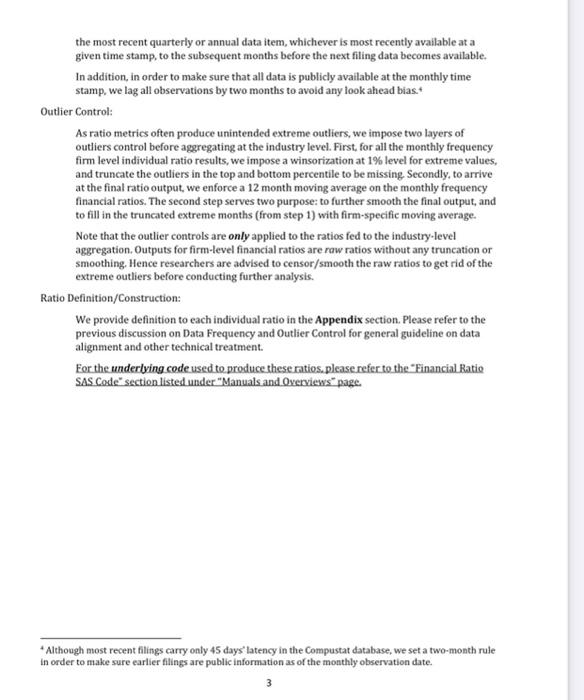

Read the WRDS Financial Ratios PDF document and write a 2page summary of what you understood and learned from the information therein. The MAXIMUM number of pages of the summary is THREE! This write MUST be in your own words. I will be checking for plagiarism. You will receive a COURSE grade of ' F ' if you plagiarize. This is an INDIVIDUAL assignment WRDS Industry Financial Ratio August 2016 WRDS Research Team Overview WRDS Industry Financial Ratio (WIFR hereafter) is a collection of most commonly used financial ratios by academic researchers. There are in total over 70 financial ratios grouped into the following seven categories: Capitalization, Efficiency, Financial Soundness/Solvency, Liquidity, Profitability, Valuation and Others. Ratios for each individual company as well as at industry aggregated level are included in the output. Parameter Specification Universe Selection: Users can choose between the universe of CRSP Common Stock and S\&P 500 Index Constituents. As many of the ratios studied here are void of economic meanings among the finance companies, we have hence excluded these firms from our universe. Industry Classification: Two systems of industry dassification are accepted in the WIFR: GICS Economic Sector Level Index. and Fama-French Industry Classification. More specifically, the GICS classification includes 10 distinct economic sectors: Energy, Materials, Industrials, Consumer Discretionary, Consumer Staples, Health Care, Financials, Information Technology, Telecom and Utilities. As Fama-French carries more than one unique industry classification system, we allow users to choose the exact number of industries. 1 Industry Level Aggregation: Aggregation of financial ratios to industry level is an important consideration, especially when it comes to valuation ratios. As researchers have previously pointed out, P/E ratios (or generally ratios that use denominators that can be negative) should never be averaged. 2 While some industry practitioners advocate simply dropping out all the firms with non-positive ratios before aggregation, we propose keeping all the observations and taking the median, rather than mean, as ' Please see Kenneth R. French's website for detailed industry classification description. http://mbatudkdartmouthedu/pages/faculty/ken french/data library html 2 See discussion on p 239 of Welch's "Intro to Finance". beted//www. freeinfosociety.com/pdfs/misc/introtofinancepadf the industry-level ratio. 3 Users will still have access to all the firm-level ratio results, and if needed, can choose other aggregation metrics to arrive at the industry-level ratio. Financial Ratio Definition Theme Classification WIFR collects over 70 different financial ratios, categorized based on the economic intuition into the following seven groups: 1. Capitalization: measures the debt component of a firm's total capital structure, e.g.: Capitalization Ratio, Total Debt-to-Invested Capital Ratio; 2. Efficiency: captures the effectiveness of firm's usage of assets and liability, e.g: Asset Turnover, Inventory Turnover; 3. Financial Soundness/Solvency: captures the firm's ability to meet long-term obligations, e.g.: Total Debt to Equity Ratio, Interest Coverage Ratio; 4. Liquidity: measures a firm's ability to meet its short-term obligations, e.g.: Current Ratio, Quick Ratio; 5. Profitability: measures the ability of a firm to generate profit, e.g.: R0A, Gross Profit Margin; 6. Valuation: estimates the attractiveness of a firm's stock (overpriced or underpriced), e.g.* P/E ratio, Shiller's CAPE ratio; 7. Others: Miscellaneous ratios, e.g. R\&D-to-Sales, Labor Expenses-to-Sales. Please refer to the Appendix section for complete list of financial ratios and corresponding categorization. Individual Ratio Individual financial ratios are samples of most commonly used metrics by academic researchers or industry practitioners. Data Source: All accounting related data are obtained from Compustat Quarterly and Annual file. Pricing related data, such as Market Capitalization and Price, are obtained from both CRSP and Compustat, and we rely on CRSP as the primary data source for pricing data. Earnings related data are from IBES database. Data Frequency: The final outputs for both individual firm and industry-level aggregated value are at monthly frequency. In order to populate the data to monthly frequency, we carry forward 3 We set default industry aggregation method to be Median, and yet provide users with the option of taking simple average across industry classification. Please use the Mean option with caution. 2 the most recent quarterly or annual data item, whichever is most recently available at a given time stamp, to the subsequent months before the next filing data becomes available. In addition, in order to make sure that all data is publicly available at the monthly time stamp, we lag all observations by two months to avoid any look ahead bias.. Outlier Control: As ratio metrics often produce unintended extreme outliers, we impose two layers of outliers control before aggregating at the industry level. First, for all the monthly frequency firm level individual ratio results, we impose a winsorization at 1% level for extreme values, and truncate the outliers in the top and bottom percentile to be missing Secondly, to arrive at the final ratio output, we enforce a 12 month moving average on the monthly frequency financial ratios. The second step serves two purpose: to further smooth the final output, and to fill in the truncated extreme months (from step 1) with firm-specific moving average. Note that the outlier controls are only applied to the ratios fed to the industry-level aggregation. Outputs for firm-level financial ratios are raw ratios without any truncation or smoothing. Hence researchers are advised to censor/smooth the raw ratios to get rid of the extreme outliers before conducting further analysis. Ratio Definition/Construction: We provide definition to each individual ratio in the Appendix section. Please refer to the previous discussion on Data Frequency and Outier Control for general guideline on data alignment and other technical treatment. For the underlying code used to produce these ratios. please refer to the "Financial Ratio SAS Code" section listed under "Manuals and Oyerviews" page. "Although most recent filings carry only 45 days' latency in the Compustat database, we set a two-month rule in order to make sure earlier filings are public information as of the monthly observation date. Read the WRDS Financial Ratios PDF document and write a 2page summary of what you understood and learned from the information therein. The MAXIMUM number of pages of the summary is THREE! This write MUST be in your own words. I will be checking for plagiarism. You will receive a COURSE grade of ' F ' if you plagiarize. This is an INDIVIDUAL assignment WRDS Industry Financial Ratio August 2016 WRDS Research Team Overview WRDS Industry Financial Ratio (WIFR hereafter) is a collection of most commonly used financial ratios by academic researchers. There are in total over 70 financial ratios grouped into the following seven categories: Capitalization, Efficiency, Financial Soundness/Solvency, Liquidity, Profitability, Valuation and Others. Ratios for each individual company as well as at industry aggregated level are included in the output. Parameter Specification Universe Selection: Users can choose between the universe of CRSP Common Stock and S\&P 500 Index Constituents. As many of the ratios studied here are void of economic meanings among the finance companies, we have hence excluded these firms from our universe. Industry Classification: Two systems of industry dassification are accepted in the WIFR: GICS Economic Sector Level Index. and Fama-French Industry Classification. More specifically, the GICS classification includes 10 distinct economic sectors: Energy, Materials, Industrials, Consumer Discretionary, Consumer Staples, Health Care, Financials, Information Technology, Telecom and Utilities. As Fama-French carries more than one unique industry classification system, we allow users to choose the exact number of industries. 1 Industry Level Aggregation: Aggregation of financial ratios to industry level is an important consideration, especially when it comes to valuation ratios. As researchers have previously pointed out, P/E ratios (or generally ratios that use denominators that can be negative) should never be averaged. 2 While some industry practitioners advocate simply dropping out all the firms with non-positive ratios before aggregation, we propose keeping all the observations and taking the median, rather than mean, as ' Please see Kenneth R. French's website for detailed industry classification description. http://mbatudkdartmouthedu/pages/faculty/ken french/data library html 2 See discussion on p 239 of Welch's "Intro to Finance". beted//www. freeinfosociety.com/pdfs/misc/introtofinancepadf the industry-level ratio. 3 Users will still have access to all the firm-level ratio results, and if needed, can choose other aggregation metrics to arrive at the industry-level ratio. Financial Ratio Definition Theme Classification WIFR collects over 70 different financial ratios, categorized based on the economic intuition into the following seven groups: 1. Capitalization: measures the debt component of a firm's total capital structure, e.g.: Capitalization Ratio, Total Debt-to-Invested Capital Ratio; 2. Efficiency: captures the effectiveness of firm's usage of assets and liability, e.g: Asset Turnover, Inventory Turnover; 3. Financial Soundness/Solvency: captures the firm's ability to meet long-term obligations, e.g.: Total Debt to Equity Ratio, Interest Coverage Ratio; 4. Liquidity: measures a firm's ability to meet its short-term obligations, e.g.: Current Ratio, Quick Ratio; 5. Profitability: measures the ability of a firm to generate profit, e.g.: R0A, Gross Profit Margin; 6. Valuation: estimates the attractiveness of a firm's stock (overpriced or underpriced), e.g.* P/E ratio, Shiller's CAPE ratio; 7. Others: Miscellaneous ratios, e.g. R\&D-to-Sales, Labor Expenses-to-Sales. Please refer to the Appendix section for complete list of financial ratios and corresponding categorization. Individual Ratio Individual financial ratios are samples of most commonly used metrics by academic researchers or industry practitioners. Data Source: All accounting related data are obtained from Compustat Quarterly and Annual file. Pricing related data, such as Market Capitalization and Price, are obtained from both CRSP and Compustat, and we rely on CRSP as the primary data source for pricing data. Earnings related data are from IBES database. Data Frequency: The final outputs for both individual firm and industry-level aggregated value are at monthly frequency. In order to populate the data to monthly frequency, we carry forward 3 We set default industry aggregation method to be Median, and yet provide users with the option of taking simple average across industry classification. Please use the Mean option with caution. 2 the most recent quarterly or annual data item, whichever is most recently available at a given time stamp, to the subsequent months before the next filing data becomes available. In addition, in order to make sure that all data is publicly available at the monthly time stamp, we lag all observations by two months to avoid any look ahead bias.. Outlier Control: As ratio metrics often produce unintended extreme outliers, we impose two layers of outliers control before aggregating at the industry level. First, for all the monthly frequency firm level individual ratio results, we impose a winsorization at 1% level for extreme values, and truncate the outliers in the top and bottom percentile to be missing Secondly, to arrive at the final ratio output, we enforce a 12 month moving average on the monthly frequency financial ratios. The second step serves two purpose: to further smooth the final output, and to fill in the truncated extreme months (from step 1) with firm-specific moving average. Note that the outlier controls are only applied to the ratios fed to the industry-level aggregation. Outputs for firm-level financial ratios are raw ratios without any truncation or smoothing. Hence researchers are advised to censor/smooth the raw ratios to get rid of the extreme outliers before conducting further analysis. Ratio Definition/Construction: We provide definition to each individual ratio in the Appendix section. Please refer to the previous discussion on Data Frequency and Outier Control for general guideline on data alignment and other technical treatment. For the underlying code used to produce these ratios. please refer to the "Financial Ratio SAS Code" section listed under "Manuals and Oyerviews" page. "Although most recent filings carry only 45 days' latency in the Compustat database, we set a two-month rule in order to make sure earlier filings are public information as of the monthly observation date

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts