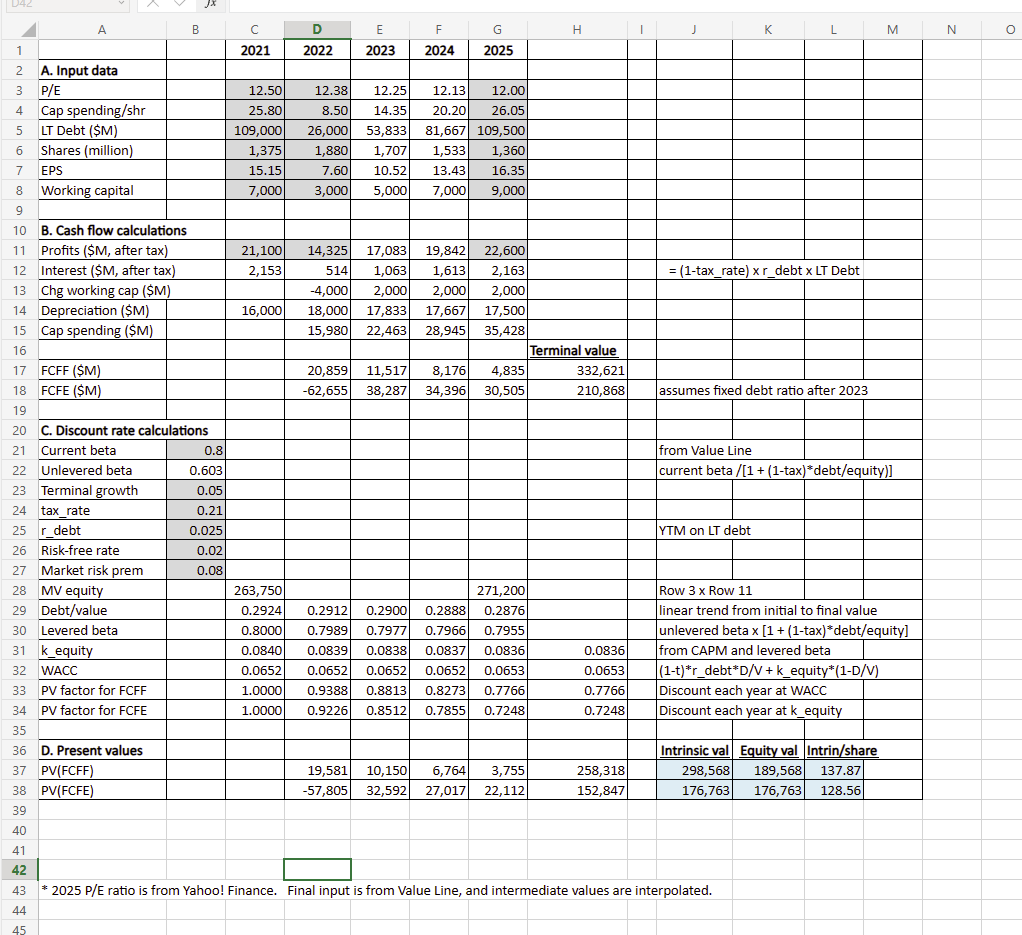

Recalculate the intrinsic value of Toyota shares using the free cash flow model of Spreadsheet(above) under each

Fantastic news! We've Found the answer you've been seeking!

Question:

Recalculate the intrinsic value of Toyota shares using the free cash flow model of Spreadsheet(above) under each of the following assumptions. Treat each scenario independently.

a. Toyota's P/E ratio starting in 2025 (cell G3) will be 11.5.

b. Toyota's unlevered beta (cell B22) is .65.

c. The market risk premium (cell B27) is 7.5%

Expert Answer:

To recalculate the intrinsic value of Toyota shares using the free cash flow model under each of ... View the full answer

Related Book For

Posted Date: