Question: Rederive the expression for the Forward rate F(t,T1,T2). Starting from this expression: But, now assuming continuous compounding (e.g., of the form: exp(-rT) rather than of

Rederive the expression for the Forward rate F(t,T1,T2).

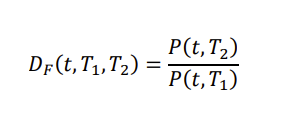

Starting from this expression:

But, now assuming continuous compounding (e.g., of the form: exp(-rT) rather than of the form: 1/(1+rT)) for the forward starting discounting DF using the constant forward rate F(t,T1,T2), between T1 and T2, restate the expression of the Forward Rate w.r.t. to the Bond Prices. Show that as = T2-T1, tends to zero (instantaneous forward), both expressions ( simple compounding vs continuous compounding you restated above) converge to the same result.

DF(t,T1,T2)=P(t,T1)P(t,T2)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock