Question: Refer to the data below. TesCorp's Beta is [Note: There was an error in the grading if you answered the question before 6:30 pm on

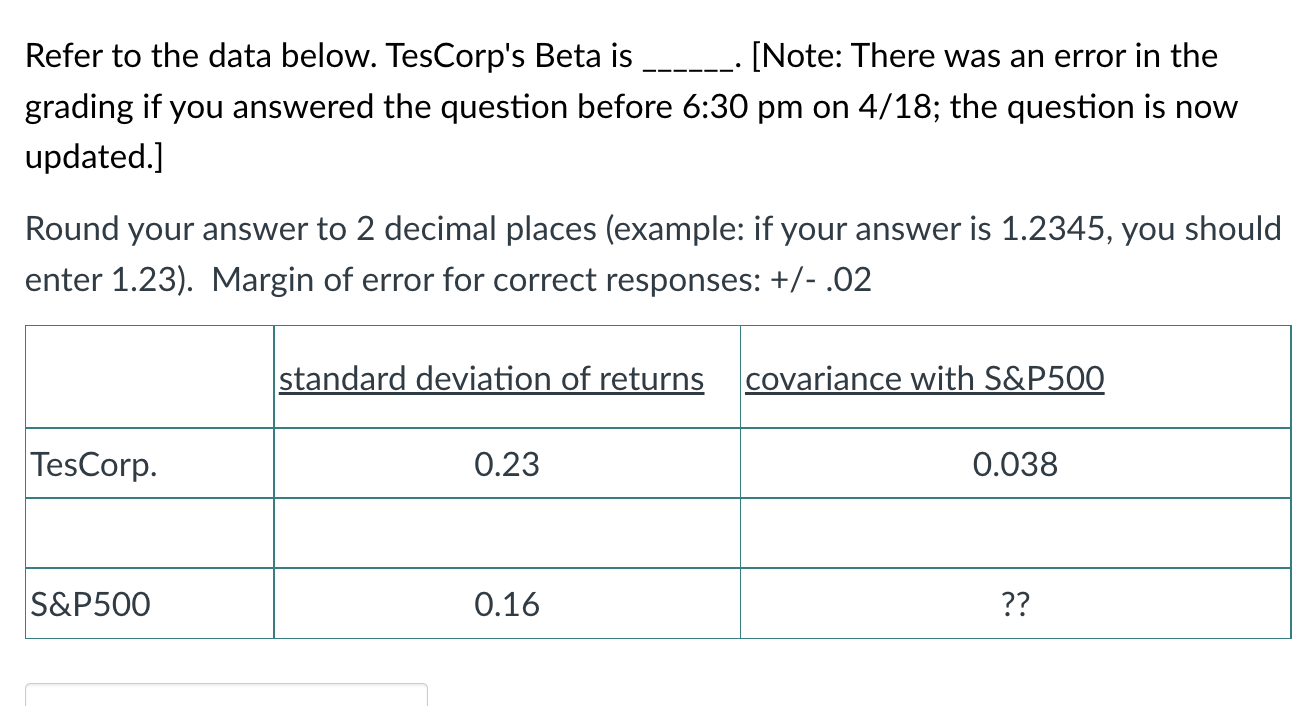

Refer to the data below. TesCorp's Beta is [Note: There was an error in the grading if you answered the question before 6:30 pm on 4/18; the question is now updated.] Round your answer to 2 decimal places (example: if your answer is 1.2345, you should enter 1.23). Margin of error for correct responses: +/-.02 standard deviation of returns covariance with S&P500 TesCorp. 0.23 0.038 S&P500 0.16

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock