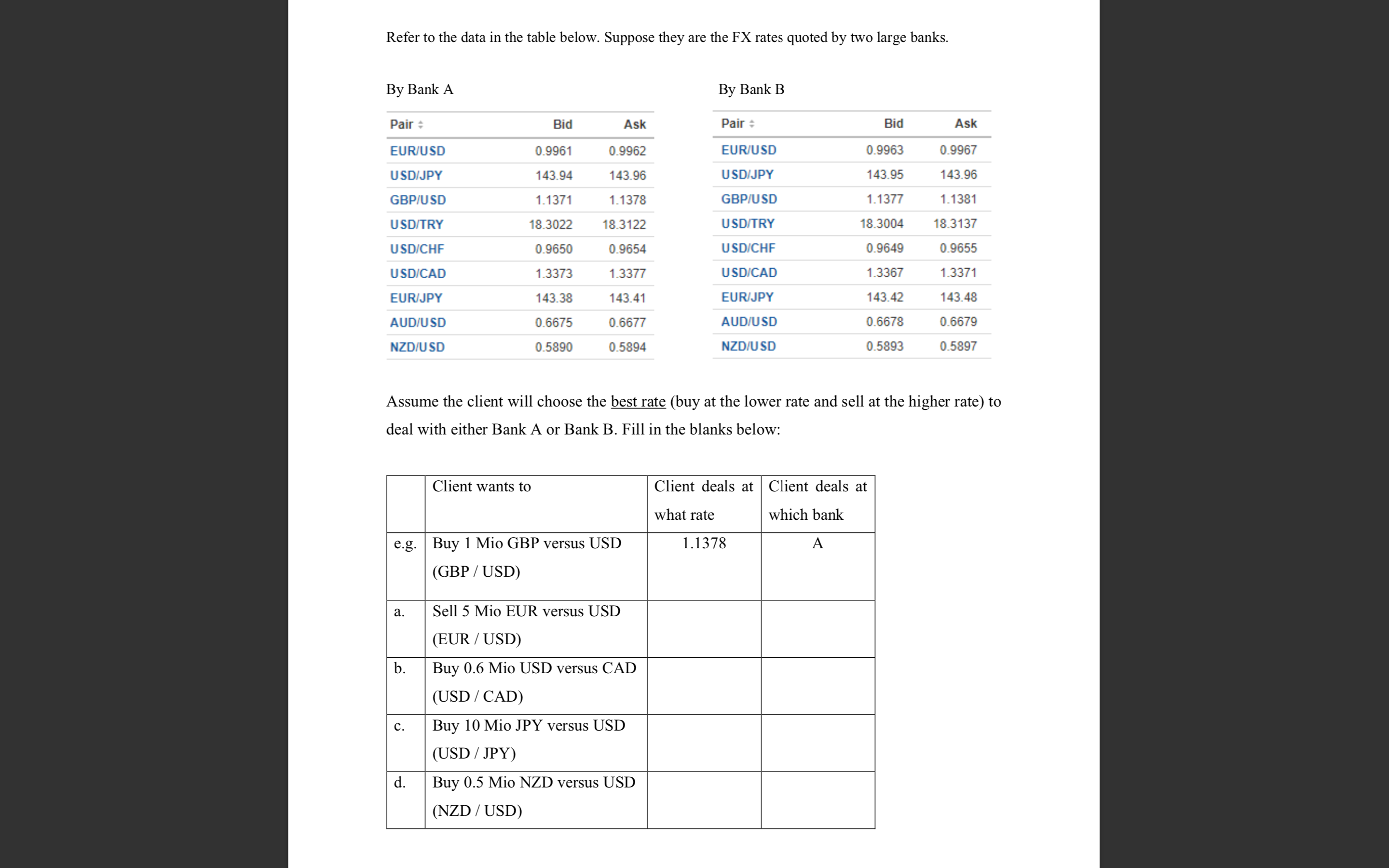

Question: Refer to the data in the table below. Suppose they are the FX rates quoted by two large banks. By Bank A By Bank B

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts