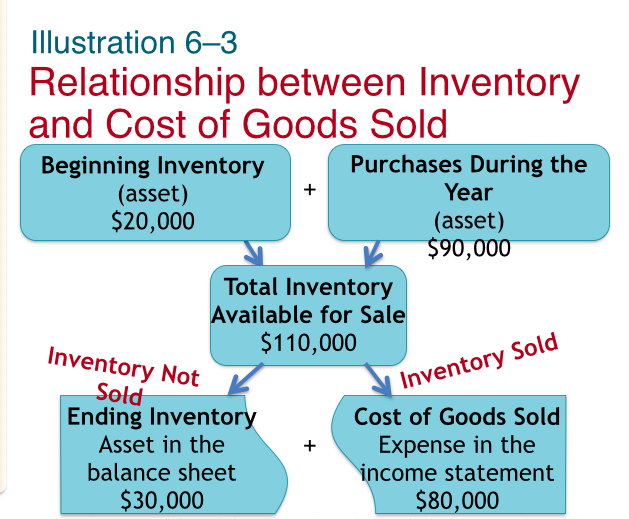

Question: Relationship between Inventory and COGS: Beginning Inventory + Purchases = Goods Available for Sale. Goods Available for Sale = COGS + Ending Inventory Inventory valuation

Relationship between Inventory and COGS:

Beginning Inventory + Purchases = Goods Available for Sale.

Goods Available for Sale = COGS + Ending Inventory

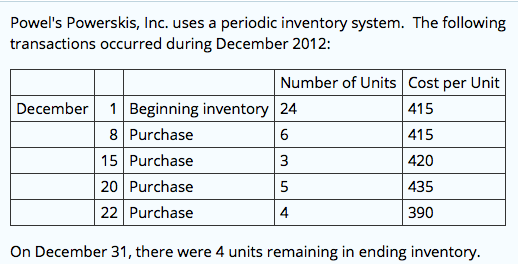

Inventory valuation methods are based on assumption of inventory flow. Complete the following exercise

Compute ending inventory and cost of goods sold using FIFO, LIFO and Weighted Average inventory costing.

DISCUSS:

1. Which method yields higher net income? (Hint: Higher Ending Inventory means lower COGS. Lower COGS (COGS is an expense account) = Higher Net Income)

2. Which method would a business choose under the income statement approach?

3. Which method would a business choose under the Balance Sheet approach?

Illustration 6-3 Relationship between Inventory and Cost of Goods Sold Purchases During the Year (asset) 90,000 Beginning Inventory (asset) $20,000 Total Inventory Available for Sale $110,000 Inventory Not Sold Inventory Sold Ending Inventor Asset in the balance sheet S30,000 Cost of Goods Sold Expense in the income statement $80,000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts