Question: Require clarification to work out part A and D for this question please. 2. [21 marks] In Simpleland, there are only two risky assets in

![question please. 2. [21 marks] In Simpleland, there are only two risky](https://s3.amazonaws.com/si.experts.images/answers/2024/06/66623398f3c76_76866623398e61e1.jpg)

Require clarification to work out part A and D for this question please.

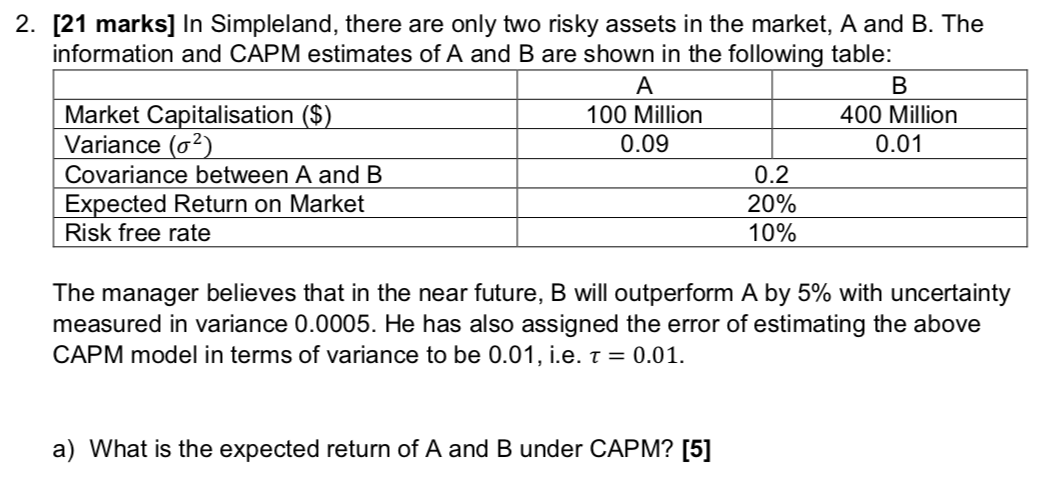

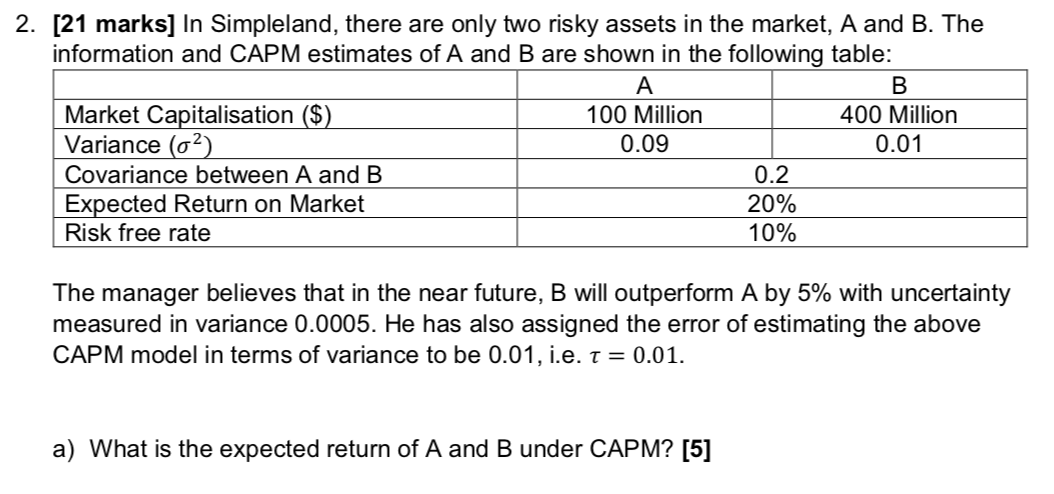

2. [21 marks] In Simpleland, there are only two risky assets in the market, A and B. The information and CAPM estimates ofA and B are shown in the following table: : Market Caitalisation s m 400 Million Variance (02) 0.09 0.01 Covariance between A and B 0.2 Risk free rate 10% The manager believes that in the near future, B will outperform A by 5% with uncertainty measured in variance 0.0005. He has also assigned the error of estimating the above CAPM model in terms of variance to be 0.01, i.e. r = 0.01. a) What is the expected retum of A and B under CAP M? [5] e) What is the BIack-Litterman adjusted values of expected return of the market? [9]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts