Question: Require help working out two questions from a sample past paper from 2019 Macquarie for Applied Finance Management 1. [5 marks] Consider stocks A and

Require help working out two questions from a sample past paper from 2019 Macquarie for Applied Finance Management

![from 2019 Macquarie for Applied Finance Management 1. [5 marks] Consider stocks](https://s3.amazonaws.com/si.experts.images/answers/2024/06/666235516cf7b_20966623551521f1.jpg)

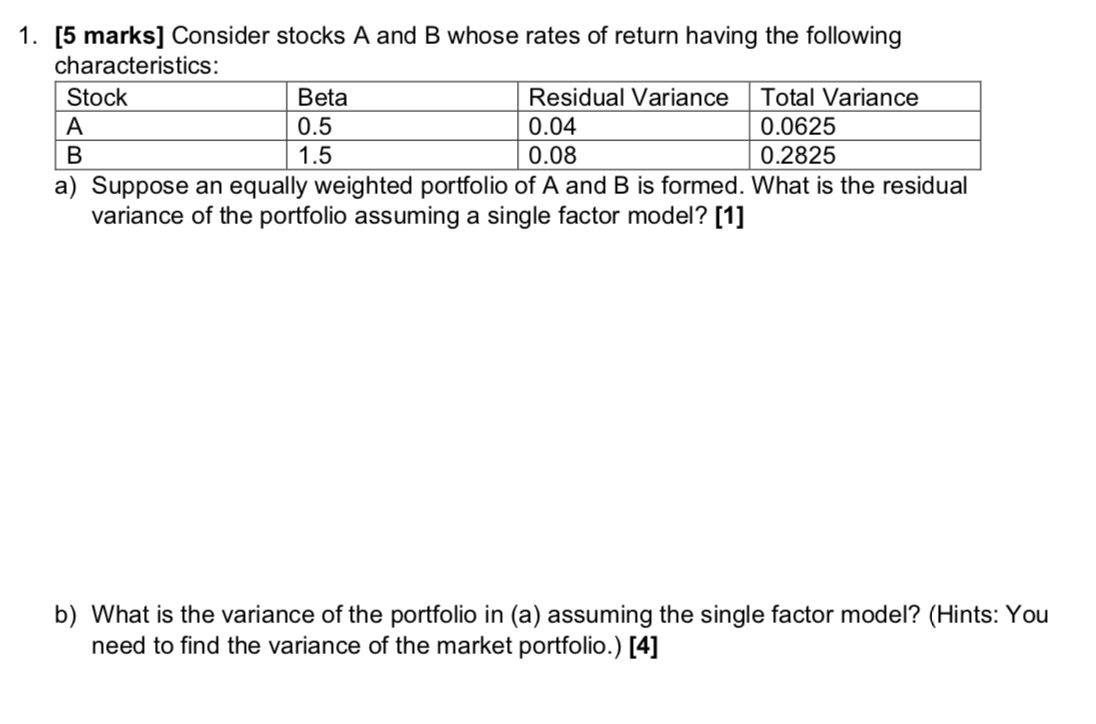

1. [5 marks] Consider stocks A and B whose rates of return having the following characteristics: Stock Beta Residual Variance Total Variance A 0.5 0.04 0.0625 B 1.5 0.08 0.2825 a) Suppose an equally weighted portfolio of A and B is formed. What is the residual variance of the portfolio assuming a single factor model? [1] b) What is the variance of the portfolio in (a) assuming the single factor model? (Hints: You need to find the variance of the market portfolio.) [4]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock