Question: Required: 1. Realized gain or loss for entity, Parent and Sub 2. Interest elimination and balance for entity, Parent and Sub 3. Interco interest revenue

Required: 1. Realized gain or loss for entity, Parent and Sub

Required: 1. Realized gain or loss for entity, Parent and Sub

2. Interest elimination and balance for entity, Parent and Sub

3. Interco interest revenue and expense

4. Calculation of consolidated net income

5. Consolidated Income Statement for year 7 using 40% tax rate

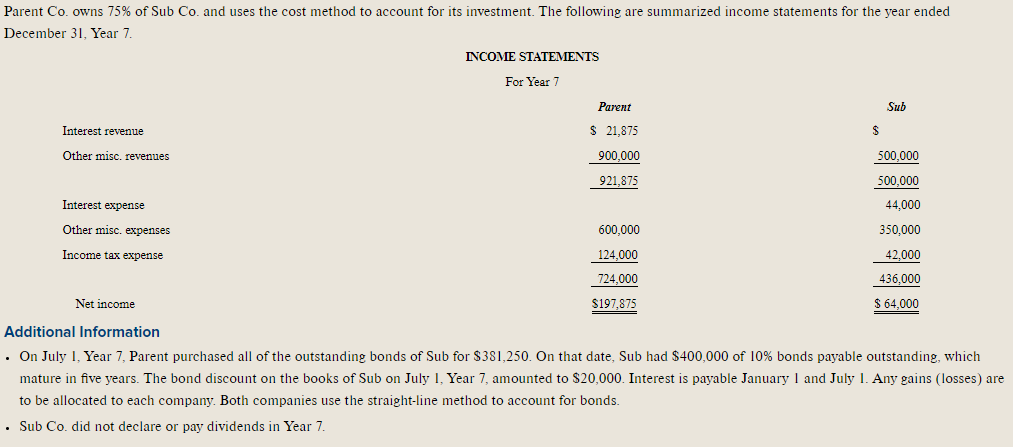

Parent Co. owns 75% of Sub Co. and uses the cost method to account for its investment. The following are summarized income statements for the year ended December 31 , Year 7 . Sub \begin{tabular}{r} $ \\ \begin{tabular}{r} 500,000 \\ \hline 500,000 \end{tabular} \\ 44,000 \\ 350,000 \\ 42,000 \\ \hline 436,000 \\ \hline$64,000 \\ \hline \end{tabular} Additional Information - On July 1, Year 7, Parent purchased all of the outstanding bonds of Sub for $381,250. On that date, Sub had $400,000 of 10% bonds payable outstanding, which mature in five years. The bond discount on the books of Sub on July 1, Year 7, amounted to $20,000. Interest is payable January 1 and July 1 . Any gains (losses) are to be allocated to each company. Both companies use the straight-line method to account for bonds. - Sub Co. did not declare or pay dividends in Year 7

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts