Question: Required 1. What are Johnson's options regarding how he might respond to the issues raised by Relzo? 2. Items 1 and 3 deal specifically with

Required

1. What are Johnson's options regarding how he might respond to the issues raised by Relzo?

2. Items 1 and 3 deal specifically with revenue and expense recognition in the income statement. What principles and guidelines govern when and how each of these items should be recorded?

3. Relzo raises issues with the consistent application of accounting methods (item 4) and the consistent classification of certain line items (item 5). Do you think it is within the rights of a company to vary accounting methods and reclassify certain line items?

CASE STUDY: LONE STAR POWER

Ward Johnson stared out the window. In the three months since he had assumed the role of chief investment officer at Lone Star Power, Johnson thought the company's communications with the investing public had been superb, particularly with respect to its SEC filings. A single letter from an apparently upset analyst had changed that view.

Lone Star Power was a midsize power generation and power distribution company based in the Southwest. It provided electrical power to more than 750,000 homes, businesses, and government agencies. In addition to power generation and distribution, Lone Star sold and installed a wide-ranging array of products, from appliances to power-generation backup systems. It also offered service and repairs to customers throughout its territory. Total revenues for the quarter ended December 31, 2016, had topped $1 billion for the first time. With only one exception, the company had managed to grow both revenues and profits in each quarter since 2000. Put in place in early 2014, the company's formal investor-relations function was relatively new. Prior to that, Lone Star had a small support staff that would send annual reports and similar literature in response to phone requests and handle other routine investor inquiries. In addition to his other duties, Johnson was expected to develop the investor-relations department in a way that would enhance Lone Star's standing with the investing community.

Marianne Relzo was a senior, all-star equity analyst with Pitt Financial, a well-regarded U.S. investment bank. In a letter Johnson, Relzo detailed her discontent with the company's external financial communications. She complained about items as specific as Lone Star's financial-statement footnote disclosures and as general as the company's composite accounting policies. Johnson knew he would have to meet with Lone Star's senior financial staff and receive input as to whether these issues had merit and how he should respond. With a red pen in hand, he read the letter once again.

Relzo's letter raised a number of issues for Johnson to consider. In the margins of the letter, he jotted notes regarding each one. From his experience, Johnson knew it was an analyst's objective to gather as much information about a company as possible. Regulation FD, however, defined the landscape regarding how he and other Lone Star officer should release information, but he was unsure what was implied regarding how he should deal with financial-reporting questions.

Johnson was not an accountant, and was not at all confident that he could articulate Lone Star's position on what revenues and expenses were recorded. On the expense side, in particular, he was perplexed as to why it was even an issue if the company were to negotiate a discount that required promotional fees to be paid in advance, charging net income when paid. By recording in this fashion, he thought Lone Star was only being conservative by accelerating a loss.

The company was also being questioned on its overall financial-reporting "transparency." Lone Star followed Generally Accepted Accounting Principles (GAAP) to the letter and filed timely reports with the SEC. Its financial statements were audited, and each major topic required in the Management Discussion and Analysis (MD&A) was dutifully disclosed. It seemed unreasonable to Johnson that the company be expected to provide real-time details on such items as negotiations with specific customers and write-offs of assets.

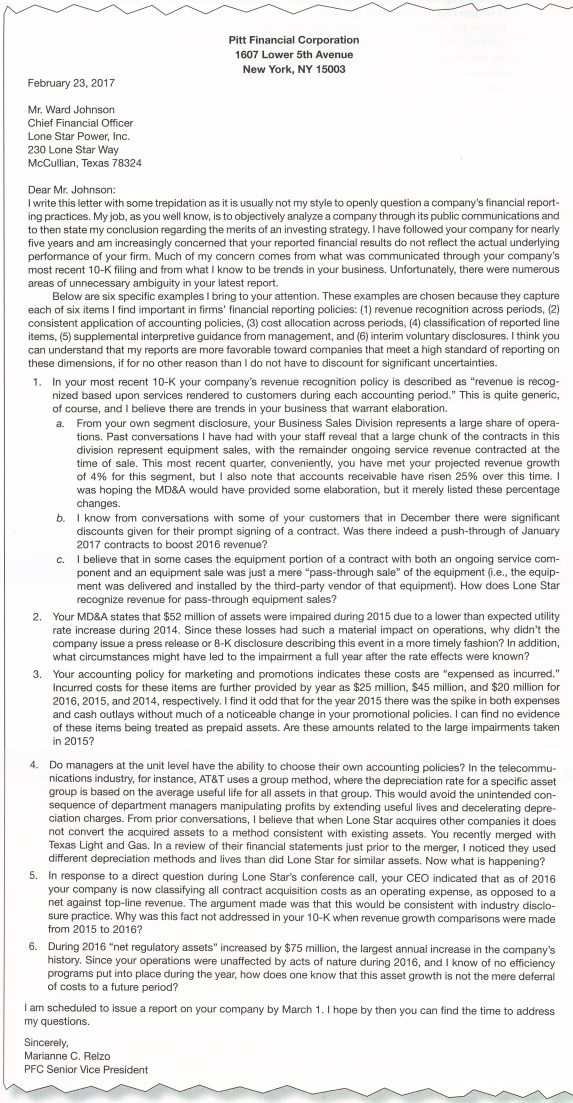

Pitt Financial Corporation rear Lower 5th Meme New York. NY 1500i! February 23. 201? Mr. Ward Johnem Chief Frnanciat Officer Lone Star Power. Inc. 230 Lone star Way tr'IcCull'ran. Texas T8324 Dear Mr. Johnson: 1 writethis letter with sornetrepidaiicn as itis Iusually not rnystyistoopenly qusslion a company's nancial repen- ing practices. Mylab. asyou well know. Isto objecihrely analyzeaccmpenythrough its public communications and to than state my conclusion regarding the merits oian Investing strategy. I have followed yochoerany forneariy ve years and am increasingly concocted that your reported nancial results do not reflect Hts acute] underlying performance of your flrrn. Much of my concent comes from what was communicated through your oornpany's most recent til-K ling and from what I know to be trends In your business. Uniormnately. there were mus areas of unnecessary airbiguity in your latest report. Below aresbt specific examples I bring to your attention. These examples. are chosen becausethsy capture each of six items | nd important in ilnrrs' financial reporting policies: [1] revenue recognition across periods. {21 oar'rsistent application ofacccunting policies. t3] cost allocation across periods. {4] classication of moaned Ilne Items, {5] supplemental interpretive guidance from management. and {t interim voluntary disclosures. lthinh you can understand that n'I1rr reports are more taverabie toward companies that meet a high standard of reporting on these dimensions. It for no other reason titan I do not have to discount for significant uncertainties. I. In your most recent til-K your company's raver-we recog'iition policy Is described as \"revenue is recog- nized based upon services rendered to mistomers during each accounting period." This is quite generic. of m. and I believe there are trends In your business that warrant elaboration. a. From your own segment disclosure. your Business Sales Division represents a large We of opera- time. Past conversations I have had with your staff reveal that a large chunlt oi the contracts in this division represent equipment sales with the Iernsindsr ongoing service reveme contracted at the time of sale. This most recent quarter. conveniently. you have met you" projected revenue groin-1h of 4% for this segment, but I also note that accou'rts receivable have risen 25% over this time. I was hoping the MDM would have provided some slab-oration. but it merely lisled these percentage changes. in. i Item from. conversations Iirrith some of your motomers that it December there were signlticant discounts given for their prompt signing of a contract. Was there indeed a push-through of January 2011:\" contracts to boost 2015 revenue? c. I believe that In some cases the equipment portion of a contract Iririth both an ongoing service com- ponent and an equipment sale was iust a mere \"pass-through eaie' of the eqripment ti.e.. the equip- ment was delivered and installed by the mireparty vendor of that sorripmenl'i. How does Lone Star recognize revenue for pass-through equipment sates? 2. Your Mitten. states that $52 million of assets were lrnpalred during 2015 due to a lower than expected utility rate increase during 2014. Since these losses had such a material impact on operations. why didn't the company issue a press release ore-K disclosure describing this event in a more timely fashion? In addition. what circumstances might have led to the impelnnent a full year alter the rate reects were known? 3. Your accounting policy for marketing and promotions indicates these costs are \"aspensed as incurred." Incurred costs for these items are further provided by year as $25 million. $45 mlllon. and $20 million for 2010. 2015. and 201s. respectively. I nd it odd thatiorths year 2015 there were the splits it both expanses and cash outlays without much of a noticeable change in your promotional policies. I can find no evidence of dress iterris being heated as prepaid assets. Ne these amounts relatedto the large Impairnents taken in 2015? it. Do managers at the unit level have the ability to choose their own accounting policies? In the telecommu- nications Industry. for instance. ATllT uses a group rnethcd. where thedaoreeiation rate for a specic asset group is based on the average useful life for all assets in that group. This would avoid the wtlntended con- sequence of department manager-e manipulating profits by astending useful lives and deceierating depre- ciation charges. From prior conversations. I believe that when Lone Star aoou'res other companies It does not convert the acquired assets to a method consistent with existing assets. 'rbu recently merged with Texas Light and Gas. In a review of their nancial statements iust prior to the merger. I noticed they used different depreciation methods and lives than did Lone Star forslmitar assets. Now what is happening? 5. In response to a direct question dufng Lona Star's conference call. you GED indicated that as at 2016 your company Is now classifying all contract acquisition costs as an operating expense. as opposed to a net against top-tine reverrua. The argument made was that this would be cer'ieistant with industry disclo- sure practice. Why was this fact not addressed in your 10~K when revenue growth comps-hone were made from 21115 to 2010'? e. During 2016 \"net regulatory assets" Iriereaeed try srs million. the largest annual increase In the corttpany's history. Since your operations were unaffetaed by acts ot nature during 2016. and I ltnow of no efciency programs out Into place during the year, now does one know that this asset grows-i is not the mere deferral of costs to a future partied? Iamecheduladto issueareponon youroompany byti-iar'oh 1. I hope bythen youcaniirrd thetimetc address my rarestlons. amnesty. Marianne C. Misc PFC Senior 1rI'Ics Pleeiderit II . \"3:. "h _ ___'-_ ' ' ..--'- _ :_-._-".E'=- _ .-l . _ _ -..:-.'--- ____.-:'--.-. ____.-.-.-r'r

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts