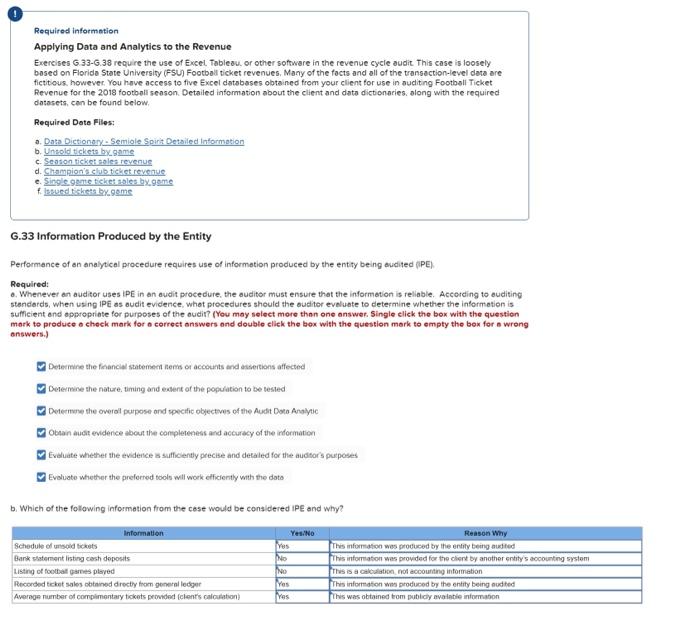

Question: Required information Applying Data and Analytics to the Revenue Exereises G.33-G.38 require the use of Excel. Tableou. or other software in the revenue cycle audit

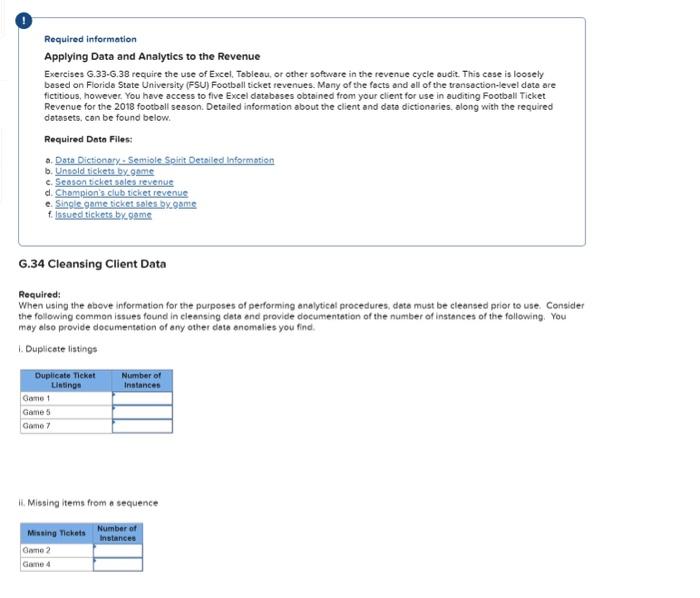

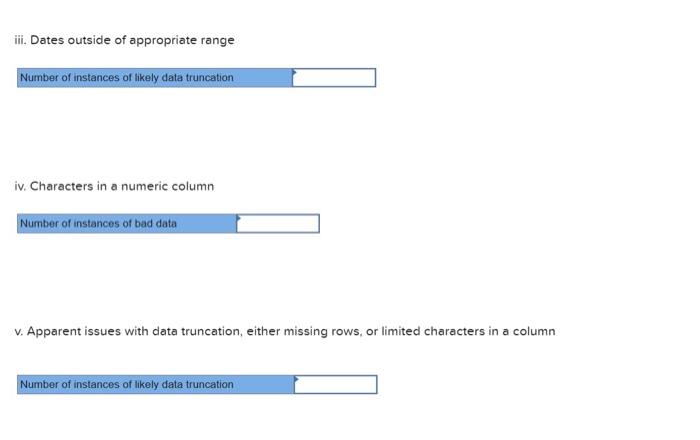

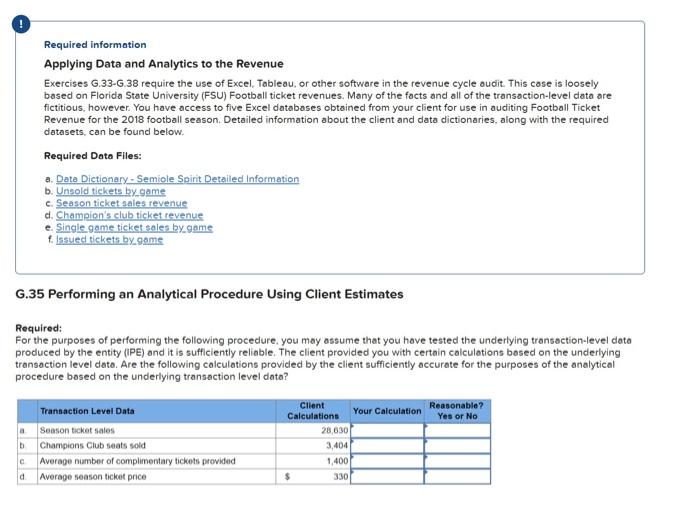

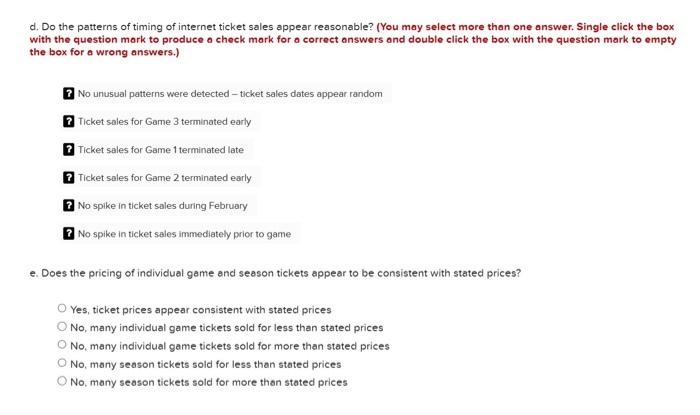

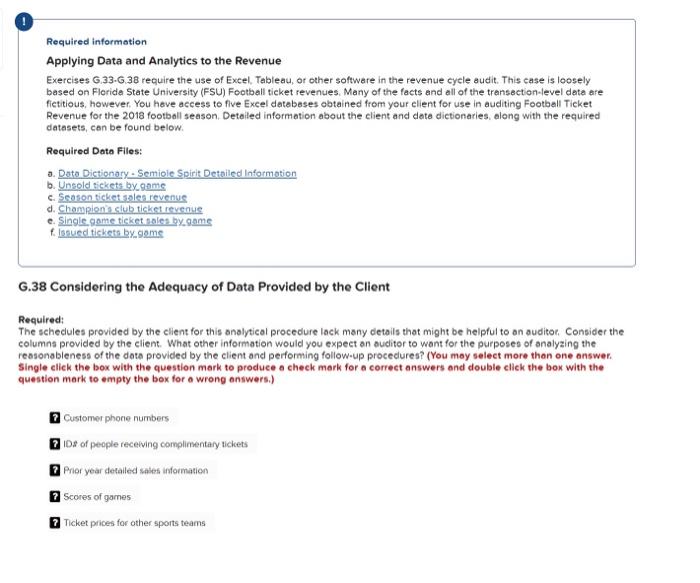

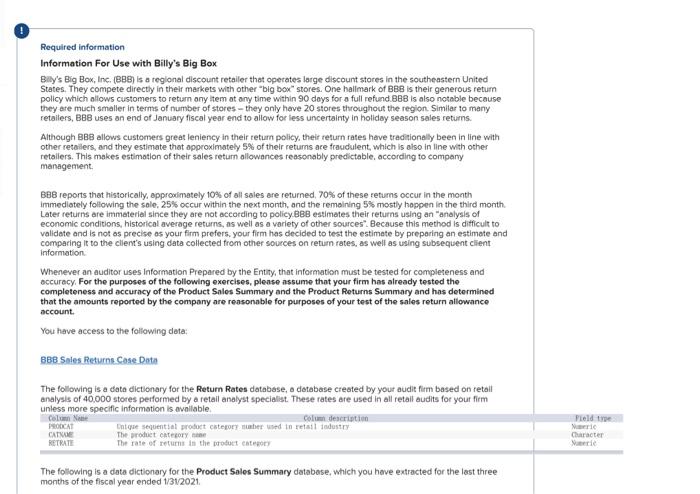

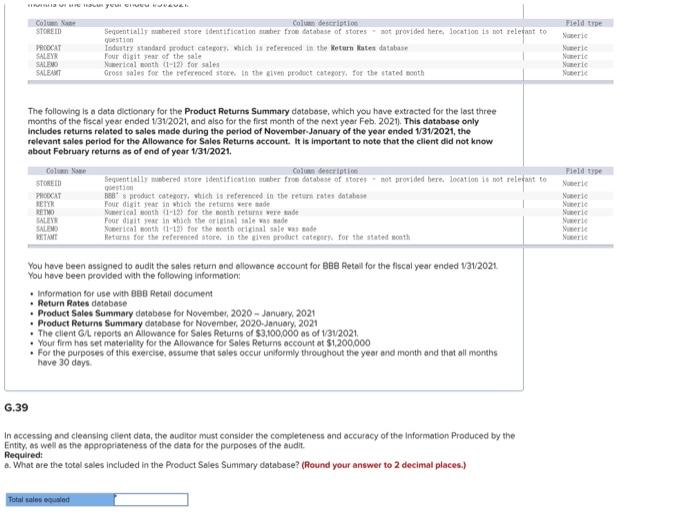

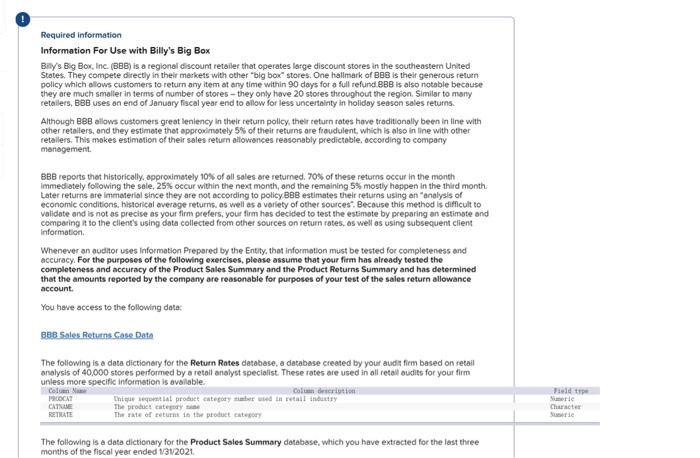

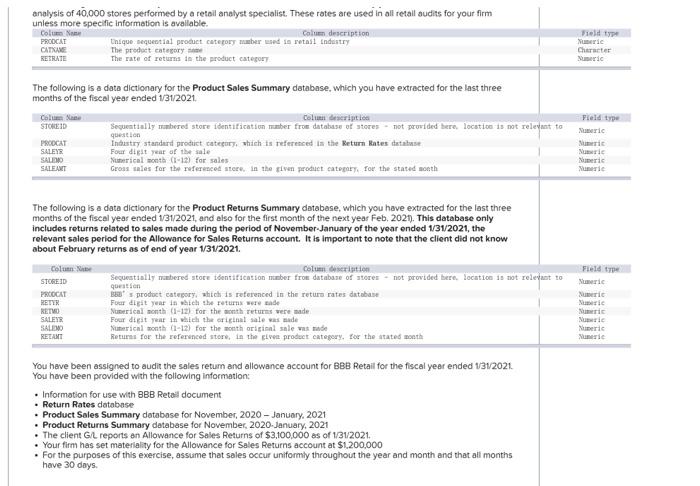

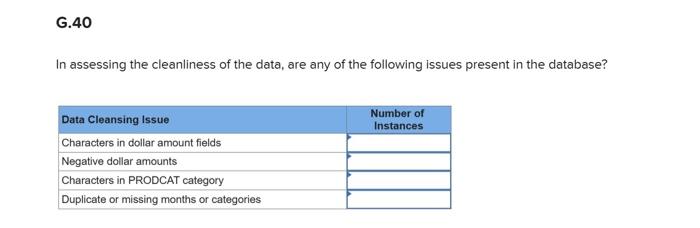

Required information Applying Data and Analytics to the Revenue Exereises G.33-G.38 require the use of Excel. Tableou. or other software in the revenue cycle audit This case is loosely bosed on Florido State University (FSU) Footboll ticket revenues, Many of the facts and all of the trangaction-ievel data are fictitous. however. You hnve access to five Excel dstobsses obtained from your client tor use in suditing Foothsill Ticket Revenue for the 2018 footboll seoson. Detailed information about the elient and dota dictionaries, along with the required datasets, can be found below. Required Date Filles: a. Data Dietionary-Semiole Spirit Detailed intormation b. Untold tickets bxgame c. Season tieket moles revenue d. Champion's elub tieket revenue e. Single gate tichet asles by 90 ese f. lstued tiskets bygome G.33 Information Produced by the Entity Performence of an analytical procedure requires use of informetion produced by the entity being oudited (PPE) Required: a. Whenever an auditor uses IPE in an audit procedure, the auditor must ensure that the information is reliable. According to auditing stenderds, when using IPE as oudit evidence, whet procedures should the ouditor evaluote to determine whether the informetion is sumficient and oppropriate for purposes of the oudit? (You may select more thnn one answer. Single elick the box with the question mork to produce o check mark for o correct onswers ond double eliek the box with the question mork to empty the box for a wreng answers.) Determine the fiancial statomeert heris of accocants and assertions affected Dermere the nature. timing and eatent of the population to be tested Determene the overal parpose ond specitic obyectives of the Audit Dola Analytic Obtain audit eviderice thout the conpleteness and accuracy of the information Evoluate whether the eviderice is sufficertyy precise and defaled for the audsor's pueposes Evaluate whether the preferred fools will work efficiently with the data b. Which of the following information from the cese would be consldered IPE and why? Required information Applying Data and Analytics to the Revenue Exereises 6.33-G.38 require the use of Excel. Tobleou, or other software in the revenue cycle oudit. This cose is loosely bosed on Florida State University (FSU) Footboll ticket revenues. Many of the focts and all of the transaetion-level date are fictitious, however. You have access to five Excel databases obtained from your client for use in auditing Football Ticket Revenue for the 2018 football season. Detalled information about the client and dato dictionaries, along with the required dotosets, con be found below. Required Date Files: a. Dota Dictionory - Semiole Spitit Detoiled Informotion b. Uneold tiekets bxgnme c. Seasen tiehet soles tevenue d. Chompion's club ticket revenue e. Singlegonne ticket roles gygome f. Issued tieketa bycgome G.34 Cleansing Client Data Required: When using the above information for the purposes of performing analytical procedures, date must be cleansed prior to use. Consider the following common issues found in cleansing doth end provide documentation of the number of instances of the following. You may also provide documentation of any other doto anomalies you find. 1. Duplicate listings 1i. Missing items from a sequence iii. Dates outside of appropriate range iv. Characters in a numeric column v. Apparent issues with data truncation, either missing rows, or limited characters in a column Required information Applying Data and Analytics to the Revenue Exercises G.33-G.38 require the use of Excel, Tableau, or other software in the revenue cycle oudit. This cose is loosely bosed on Florida State University (FSU) Football ticket revenues. Many of the facts and all of the transaction-level data are fictitious, however. You have access to five Excel databases obtained from your client for use in auditing Football Ticket Revenue for the 2018 football season. Detailed information about the client and data dictionaries, along with the required datasets, can be found below. Required Dato Files: a. Data Dictionary - Semiole Spirit Detailed Information b. Unsold tickets by game c. Season ticket sales revenue d. Champion's club ticket revenue e. Single game ticket soles bygame f. lssued tickets by gome G.35 Performing an Analytical Procedure Using Client Estimates Required: For the purposes of performing the following procedure. you may assume that you hove tested the underlying transaction-level data produced by the entity (IPE) ond it is sufficiently reliable. The client provided you with certain calculations bosed on the underlying transaction level dato. Are the following calculations provided by the client sufficiently accurate for the purposes of the analytical procedure bosed on the underlying transaction level data? Required informetion Applying Data and Analytics to the Revenue Exercises G.33.G.38 require the use of Excel. Tobleou, or other software in the revenue cyele audit. This case is loosely bosed on Florids Stote University (FSU) Footboll ticket revenues. Many of the facts and all of the transoction-level data are fictitious. however. You have accens to five Excel dstaboses obteined from your client for use in suditing Football Ticket Revenue for the 2018 football season. Detailed information about the client and data dictionaries, along with the required datasets, can be found below. Required Dato Files: . Dots Distionary - Semiole Spinit Detsiled informution b. Unsold tickets by o9me c. Season ticket ables revenve d. Chempion's club ticket revenue c. Singlegame tieket noles bygome t. issued tickets bygame G.36 Testing the Client's Estimates with Underlying Data Assume thet performance materislity hes been set at $130,000 for the purpose of this analyticel procedure, Prepere and appropriately document on andlytical procedure testing the reported soles revenue of $26,726,664 and answer the following questions: Assume thet performence meteridity has been set ot 5130.000 for the purpese of this onelytical procedure. Prepare ond appropriately document an analyticel procedure testing the reported sales revenue of 52.6726,864 and answer the following questions: Required: a. Vihat is your best estimate of 2010 football ticket revenue wising the client's average ticket sales and prices provided in the case? Do not use the actual dete for this calculation. b. Bosed on the performance maserielity set, does 2018 Football Ticket Revenue appear to be foirly stated? Yes No c. At what level would you assess the nisk of meterial misstatement related to 20 bi footbell ticket revenve after the performence of your analytical procedure (low, moderate, high)? Low Moderete High c. At what level would you ossess the risk of meterial misstatement related to 2018 football ticket revenue after the performance of your analytical procedure (low, moderate, high)? Low Moderate High d. What additional procedures would you recommend performing related to your audit of Football Ticket Revenue? (You may select more then one answer. Single cliek the box with the question merk to produce a check mark for a correct answers and double eliek the box with the question mork to empty the box for a wrong answers.) ? Test completeness and accuracy of client's calculations Contirmotion of Cash Confirmation of Accounts Recetvable Confirmation of Accounts Payable Vouch o sample of soles to cosh recelpts Observe so count of ncket imventory Required information Applying Data and Analytics to the Revenue Exercises 9.33 .9 .38 require the use of Excel, Tobleau, or other software in the revenue cycle audit. This case is loosely based on Floride Stote University (FSU) Footboll ticket revenues. Many of the facts and all of the tronsaction-level data are fictitious, however. You have occess to five Excel detobeses obtained from your client for use in auditing Football Ticket Revenue for the 2018 footboll seoson. Detoiled information obout the client and doto dietionories, along with the required datasets, can be found below. Required Doto Files: a. Pata Pictionory - Semiple Spirit Petniled Information b. Uneold bickets by gnime c. Seasen ticket soles reverue d. Champion's club ticket rovenue e. Singlegome tieket soles bycgome f. Issued tickets by pome G.37 Conducting Additional Risk Assessment Procedures Regerdless of your conclusions reoched in the questions above. perform some exploratory risk analysis on the dete provided. ldentify ony areas where you believe there moy be elevbted risk ofter performing your procedures ond identify ony specific occounts ond assertions that may be affected. You may classify and break down the date in any way you deem appropriate for the purposes of risk assessment. Be sure to provide proper documentetion of your work. Consicler the following: Required: a. Does the listing of unissued tickets oppeor to be complete ond accurote? Yes No b. Do you notice any unusual veriotions in the ratio of online va. window ticket seles? Yes No c. Do you identify ony unususl varistions in the number of complimentary tickets issued? [You may select more than one answer, Single click the box with the question mork to produce a check mork for a correct answers and double click the box with the question mark to empty the box for o wrong answers.) Tickets issued by on undentified ogent 7 Duplicile ucket numbers issued by multiple agents. Usualy high number of complimentary uckets in Game 3 Unusual potherns of tichets ssued by Agent 2 ? Unusual pattems of tickets lasued by Agent 3 Unusual patsens of tichets assued by Agent 4 Required information Applying Data and Analytics to the Revenue Exercises 9.33 .9 .38 require the use of Excel, Tobleau, or other software in the revenue cycle audit. This case is loosely based on Floride Stote University (FSU) Footboll ticket revenues. Many of the facts and all of the tronsaction-level data are fictitious, however. You have occess to five Excel detobeses obtained from your client for use in auditing Football Ticket Revenue for the 2018 footboll seoson. Detoiled information obout the client and doto dietionories, along with the required datasets, can be found below. Required Doto Files: a. Pata Pictionory - Semiple Spirit Petniled Information b. Uneold bickets by gnime c. Seasen ticket soles reverue d. Champion's club ticket rovenue e. Singlegome tieket soles bycgome f. Issued tickets by pome G.37 Conducting Additional Risk Assessment Procedures Regerdless of your conclusions reoched in the questions above. perform some exploratory risk analysis on the dete provided. ldentify ony areas where you believe there moy be elevbted risk ofter performing your procedures ond identify ony specific occounts ond assertions that may be affected. You may classify and break down the date in any way you deem appropriate for the purposes of risk assessment. Be sure to provide proper documentetion of your work. Consicler the following: Required: a. Does the listing of unissued tickets oppeor to be complete ond accurote? Yes No b. Do you notice any unusual veriotions in the ratio of online va. window ticket seles? Yes No c. Do you identify ony unususl varistions in the number of complimentary tickets issued? [You may select more than one answer, Single click the box with the question mork to produce a check mork for a correct answers and double click the box with the question mark to empty the box for o wrong answers.) Tickets issued by on undentified ogent 7 Duplicile ucket numbers issued by multiple agents. Usualy high number of complimentary uckets in Game 3 Unusual potherns of tichets ssued by Agent 2 ? Unusual pattems of tickets lasued by Agent 3 Unusual patsens of tichets assued by Agent 4 d. Do the patterns of timing of internet ticket sales appear reasonable? (You may select more than one answer. Single click the box with the question mork to produce a check mark for a correct answers and double click the box with the question mark to empty the box for a wrong answers.) No unusual patterns were detected - ticket sales dates appear random Ticket sales for Game 3 terminated early Ticket sales for Game 1 terminated late ? Ticket sales for Game 2 terminated early No spike in ticket sales during February No spike in ticket sales immediately prior to game e. Does the pricing of individual game and season tickets appear to be consistent with stated prices? Yes, ticket prices appear consistent with stated prices No, many individual game tickets sold for less than stated prices No, many individual game tickets sold for more than stated prices No, many season tickets sold for less than stated prices No, many season tickets sold for more than stated prices Required information Applying Data and Analytics to the Revenue Exercises G.33.G.38 require the use of Excel. Tableau, or other software in the revenue cycle audit. This case is loosely based on Floride State University (FSU) Footbell ticket revenues. Many of the facts and all of the transection-level date are fictitious, however. You have access to five Excel databsses obtained from your elient for use in auditing Football Ticket Revenue for the 2018 footboll season. Detailed information about the client and date dictionaries, olong with the required datasets, can be found below. Required Date Files: a. Dote Dietionary - Semiole Spirit Detailed lnformation b. Unsold tiekets by grme c. Season ticket soles revenue d. Champion's club ticket revenue e. Single gome tieket noles byosme f. 1sfued tickets by gome G.38 Considering the Adequacy of Data Provided by the Client Required: The schedules provided by the client for this analytical procedure lack many details that might be helpful to an auditor. Consider the columns provided by the client. What other information would you expect an ouditor to want for the purposes of analyzing the ressonableness of the data provided by the client and performing follow-up procedures? (You moy select more than one answer. single elick the box with the question mark to produce a check mark for a correct answers and double click the bok with the question mark to empty the box for a wrong onswers.) Qustomer phone numbers IDs of people receiving complimentary tickets Pnor year detailed soles information Scores of games Ticket prices for other sports teams Required information Information For Use with Billy's Big Box Bily's Big Box, Inc, (BBB) is a regional discount retailer that operates large discount stores in the southeastern United States. They compete directly in thelf markets with other "big box" stores. One hallmark of BBB is their generous return policy which ollows customers to retum ony item ot ony time within 90 doys for a full refund. B8B is also notable because they are much smaller in terms of number of stores - they only hove 20 stores throughout the region. Similar to many retailers, Be8 uses an end of January fiscal year end to allow for less uncertainty in holiday season sales returns. Although BBB allows customers great leniency in their return policy, their return rates hovve traditionally been in line with other retallers, and they estimate that opproximately 5% of their returns are fraudulent which is olso in line with other retaliers. This makes estimation of their sales retum allowances reasonably predictable, according to company management: BEB reports thet historically, epprodimately 10% of all sales are returned, 70% of these returns occur in the month immedlotely following the sole, 25\% occur within the next month, and the remoining 5% mostly hoppen in the third month. Later returns are immaterial since they are not according to policy.BBB estimates their returns using an "anolysis of economic conditions, historical average returns, as well as a variety of other sources". Because this method is ditficult to validate and is not os precise as your firm prefers. your firm has decided to test the estimate by preparing an estimate and comparing it to the client's using data collected from other sources on return rates, as well as using subsequent client information. Whenever an auditor uses Information Prepared by the Entity, that information must be tested for completeness and occuracy. For the purposes of the following exercises, please assume that your firm has already tested the completeness and accuracy of the Product Sales Summary and the Product Returns Summary and has determined that the amounts reported by the company are reasonable for purposes of your test of the sales return allowance account. You have access to the following data: BB8 Sales Returns Case Data The following is a data dictionary for the Retum Rates database, a dotabase created by your audit firm based on retail analysis of 40,000 stores performed by a retail analyst speciallst. These rates are used in all retall audits for yout firm The following is a data dictionary for the Product Sales Summary databose, which you have extracted for the last three months of the fiscel year ended 1/31/2021. The following is a data dictionary for the Product Returns Summary database, which you have extracted for the last three months of the fiscal year ended 1/312021, and aiso for the first month of the next year Feb. 2021). This database only includes returns related to sales made during the period of November-January of the year ended 1/31/2021, the relevant sales period for the Allowance for Sales Returns account. It is important to note that the client did not know about February returns as of end of year 1/31/2021. You hove been assigned to oudit the sales return and ollowance account for BBe Retall for the flscal year ended 1av2021. You hove been provided with the following information: - Information for use with 88 Retail documen - Return Rates dotabase - Product Sales Summary databese for November, 2020 - January, 2021 - Product Returns Summary dotobase for November, 2020-January. 2021 - The client G/L reports an Allowance for Sales Returns of \$3,100,000 as of 1/31/2021. - Your firm has set materiality for the Allowance for Soles Returns occount at $1,200,000 - For the purposes of this exercise, assume that seles occur uniformly throughout the year and month and that all months heve 30 doys. 6.39 In accessing and cleansing cilent deta, the auditor must consider the completeness and accuracy of the Information Produced by the Entity, as well as the appropriateness of the data for the purposes of the audit. Requiled: a. What are the total soles included in the Product Sales Summary database? (Round your answer to 2 decimal places.) Information For Use with Billy's Big Box Biy/s Big Box, lnc. (BBB) is a regional discoum retaller that operates large discount stores in the southeastern United States. They compete directly in their merkets with other "big box" stores. One hallmark of BBB is their generous retum policy which allows customers to return any item at any time within 90 doys for a full refund BBB is also notable because they ore much smaller in terms of number of stores - they only hove 20 stores throughout the region. Similer to many retallers, BBB uses an end of January fiscal year end to allow for less uncertainty in holidoy season sales returns. Although BBB allows customers great leniency in their retum policy, their return rates have traditionally been in line with other retallers, and they estimate that approwimstely 5% of their retums are froudulent, which is also in line with other retallers. This mokes estimotion of their sales return ollovances reasonobly predietable, occording to company martogement. BBB reports thet historically, opproximately 10% of all sales are returned. 70% of these retums occur in the month immedlotely folowing the sole, 25\% occur within the next month, and the remaining 5% mostly happen in the third month. Later retums are immaterial since they are not according to policyBBB estimates their returns using an "analysis of economic conditions. historical overage returmb. as well as a varlety of other sources". Becouse this method is difficult to volidate and is not as precise as your firm prefers, your firm has declded to test the estimote by preporing an estimote and comporing it to the client's using dota collected from other sources on return rates. as well as using subsequent client informatsen. Whenever an auditor uses information Prepered by the Entity, that information must be tested for completeness and accuracy. For the purposes of the following exercises, please assume that your firm has already tested the completeness and accuracy of the Product Sales Summary and the Product Returns Summary and has determined that the amounts reported by the company are reasonable for purposes of your test of the sales return allowance account. You have access to the following data: The following is a data dictionary for the Return Rates database, a database created by your auda firm based on retail analysis of 40,000 stores performed by a retail analyst specialist. These rates are used in oll retall audits for your flirm unless more soecific informetion is avsilable. analysis of 40,000 stores performed by a retoil analyst specialist. These rates are used in all retall audits for your firm unless more specific information is avallable. Colin Nerm PRODCEI KETRMIE Lhsque nequential psobuct caterory maber aned is retast andastry The prodact eategory that The rate of returna da the product categoet Coluen description Wislin type Nunerde Charartef Wimeate The following is a data dictionary for the Product Sales Summary database, which you have extracted for the last three months of the fiscal year ended 1/31/2021. months of the fiscal year ended 1/31/2021, and also for the first month of the next year Feb. 2021). This database only includes returns related to sales made during the period of November-January of the year ended 1/31/2021, the relevant sales period for the Allowance for Soles Retums account. It is important to note that the client did not know about February returns as of end of year 1/31/2021. In assessing the cleanliness of the data, are any of the following issues present in the database? Required information Applying Data and Analytics to the Revenue Exereises G.33-G.38 require the use of Excel. Tableou. or other software in the revenue cycle audit This case is loosely bosed on Florido State University (FSU) Footboll ticket revenues, Many of the facts and all of the trangaction-ievel data are fictitous. however. You hnve access to five Excel dstobsses obtained from your client tor use in suditing Foothsill Ticket Revenue for the 2018 footboll seoson. Detailed information about the elient and dota dictionaries, along with the required datasets, can be found below. Required Date Filles: a. Data Dietionary-Semiole Spirit Detailed intormation b. Untold tickets bxgame c. Season tieket moles revenue d. Champion's elub tieket revenue e. Single gate tichet asles by 90 ese f. lstued tiskets bygome G.33 Information Produced by the Entity Performence of an analytical procedure requires use of informetion produced by the entity being oudited (PPE) Required: a. Whenever an auditor uses IPE in an audit procedure, the auditor must ensure that the information is reliable. According to auditing stenderds, when using IPE as oudit evidence, whet procedures should the ouditor evaluote to determine whether the informetion is sumficient and oppropriate for purposes of the oudit? (You may select more thnn one answer. Single elick the box with the question mork to produce o check mark for o correct onswers ond double eliek the box with the question mork to empty the box for a wreng answers.) Determine the fiancial statomeert heris of accocants and assertions affected Dermere the nature. timing and eatent of the population to be tested Determene the overal parpose ond specitic obyectives of the Audit Dola Analytic Obtain audit eviderice thout the conpleteness and accuracy of the information Evoluate whether the eviderice is sufficertyy precise and defaled for the audsor's pueposes Evaluate whether the preferred fools will work efficiently with the data b. Which of the following information from the cese would be consldered IPE and why? Required information Applying Data and Analytics to the Revenue Exereises 6.33-G.38 require the use of Excel. Tobleou, or other software in the revenue cycle oudit. This cose is loosely bosed on Florida State University (FSU) Footboll ticket revenues. Many of the focts and all of the transaetion-level date are fictitious, however. You have access to five Excel databases obtained from your client for use in auditing Football Ticket Revenue for the 2018 football season. Detalled information about the client and dato dictionaries, along with the required dotosets, con be found below. Required Date Files: a. Dota Dictionory - Semiole Spitit Detoiled Informotion b. Uneold tiekets bxgnme c. Seasen tiehet soles tevenue d. Chompion's club ticket revenue e. Singlegonne ticket roles gygome f. Issued tieketa bycgome G.34 Cleansing Client Data Required: When using the above information for the purposes of performing analytical procedures, date must be cleansed prior to use. Consider the following common issues found in cleansing doth end provide documentation of the number of instances of the following. You may also provide documentation of any other doto anomalies you find. 1. Duplicate listings 1i. Missing items from a sequence iii. Dates outside of appropriate range iv. Characters in a numeric column v. Apparent issues with data truncation, either missing rows, or limited characters in a column Required information Applying Data and Analytics to the Revenue Exercises G.33-G.38 require the use of Excel, Tableau, or other software in the revenue cycle oudit. This cose is loosely bosed on Florida State University (FSU) Football ticket revenues. Many of the facts and all of the transaction-level data are fictitious, however. You have access to five Excel databases obtained from your client for use in auditing Football Ticket Revenue for the 2018 football season. Detailed information about the client and data dictionaries, along with the required datasets, can be found below. Required Dato Files: a. Data Dictionary - Semiole Spirit Detailed Information b. Unsold tickets by game c. Season ticket sales revenue d. Champion's club ticket revenue e. Single game ticket soles bygame f. lssued tickets by gome G.35 Performing an Analytical Procedure Using Client Estimates Required: For the purposes of performing the following procedure. you may assume that you hove tested the underlying transaction-level data produced by the entity (IPE) ond it is sufficiently reliable. The client provided you with certain calculations bosed on the underlying transaction level dato. Are the following calculations provided by the client sufficiently accurate for the purposes of the analytical procedure bosed on the underlying transaction level data? Required informetion Applying Data and Analytics to the Revenue Exercises G.33.G.38 require the use of Excel. Tobleou, or other software in the revenue cyele audit. This case is loosely bosed on Florids Stote University (FSU) Footboll ticket revenues. Many of the facts and all of the transoction-level data are fictitious. however. You have accens to five Excel dstaboses obteined from your client for use in suditing Football Ticket Revenue for the 2018 football season. Detailed information about the client and data dictionaries, along with the required datasets, can be found below. Required Dato Files: . Dots Distionary - Semiole Spinit Detsiled informution b. Unsold tickets by o9me c. Season ticket ables revenve d. Chempion's club ticket revenue c. Singlegame tieket noles bygome t. issued tickets bygame G.36 Testing the Client's Estimates with Underlying Data Assume thet performance materislity hes been set at $130,000 for the purpose of this analyticel procedure, Prepere and appropriately document on andlytical procedure testing the reported soles revenue of $26,726,664 and answer the following questions: Assume thet performence meteridity has been set ot 5130.000 for the purpese of this onelytical procedure. Prepare ond appropriately document an analyticel procedure testing the reported sales revenue of 52.6726,864 and answer the following questions: Required: a. Vihat is your best estimate of 2010 football ticket revenue wising the client's average ticket sales and prices provided in the case? Do not use the actual dete for this calculation. b. Bosed on the performance maserielity set, does 2018 Football Ticket Revenue appear to be foirly stated? Yes No c. At what level would you assess the nisk of meterial misstatement related to 20 bi footbell ticket revenve after the performence of your analytical procedure (low, moderate, high)? Low Moderete High c. At what level would you ossess the risk of meterial misstatement related to 2018 football ticket revenue after the performance of your analytical procedure (low, moderate, high)? Low Moderate High d. What additional procedures would you recommend performing related to your audit of Football Ticket Revenue? (You may select more then one answer. Single cliek the box with the question merk to produce a check mark for a correct answers and double eliek the box with the question mork to empty the box for a wrong answers.) ? Test completeness and accuracy of client's calculations Contirmotion of Cash Confirmation of Accounts Recetvable Confirmation of Accounts Payable Vouch o sample of soles to cosh recelpts Observe so count of ncket imventory Required information Applying Data and Analytics to the Revenue Exercises 9.33 .9 .38 require the use of Excel, Tobleau, or other software in the revenue cycle audit. This case is loosely based on Floride Stote University (FSU) Footboll ticket revenues. Many of the facts and all of the tronsaction-level data are fictitious, however. You have occess to five Excel detobeses obtained from your client for use in auditing Football Ticket Revenue for the 2018 footboll seoson. Detoiled information obout the client and doto dietionories, along with the required datasets, can be found below. Required Doto Files: a. Pata Pictionory - Semiple Spirit Petniled Information b. Uneold bickets by gnime c. Seasen ticket soles reverue d. Champion's club ticket rovenue e. Singlegome tieket soles bycgome f. Issued tickets by pome G.37 Conducting Additional Risk Assessment Procedures Regerdless of your conclusions reoched in the questions above. perform some exploratory risk analysis on the dete provided. ldentify ony areas where you believe there moy be elevbted risk ofter performing your procedures ond identify ony specific occounts ond assertions that may be affected. You may classify and break down the date in any way you deem appropriate for the purposes of risk assessment. Be sure to provide proper documentetion of your work. Consicler the following: Required: a. Does the listing of unissued tickets oppeor to be complete ond accurote? Yes No b. Do you notice any unusual veriotions in the ratio of online va. window ticket seles? Yes No c. Do you identify ony unususl varistions in the number of complimentary tickets issued? [You may select more than one answer, Single click the box with the question mork to produce a check mork for a correct answers and double click the box with the question mark to empty the box for o wrong answers.) Tickets issued by on undentified ogent 7 Duplicile ucket numbers issued by multiple agents. Usualy high number of complimentary uckets in Game 3 Unusual potherns of tichets ssued by Agent 2 ? Unusual pattems of tickets lasued by Agent 3 Unusual patsens of tichets assued by Agent 4 Required information Applying Data and Analytics to the Revenue Exercises 9.33 .9 .38 require the use of Excel, Tobleau, or other software in the revenue cycle audit. This case is loosely based on Floride Stote University (FSU) Footboll ticket revenues. Many of the facts and all of the tronsaction-level data are fictitious, however. You have occess to five Excel detobeses obtained from your client for use in auditing Football Ticket Revenue for the 2018 footboll seoson. Detoiled information obout the client and doto dietionories, along with the required datasets, can be found below. Required Doto Files: a. Pata Pictionory - Semiple Spirit Petniled Information b. Uneold bickets by gnime c. Seasen ticket soles reverue d. Champion's club ticket rovenue e. Singlegome tieket soles bycgome f. Issued tickets by pome G.37 Conducting Additional Risk Assessment Procedures Regerdless of your conclusions reoched in the questions above. perform some exploratory risk analysis on the dete provided. ldentify ony areas where you believe there moy be elevbted risk ofter performing your procedures ond identify ony specific occounts ond assertions that may be affected. You may classify and break down the date in any way you deem appropriate for the purposes of risk assessment. Be sure to provide proper documentetion of your work. Consicler the following: Required: a. Does the listing of unissued tickets oppeor to be complete ond accurote? Yes No b. Do you notice any unusual veriotions in the ratio of online va. window ticket seles? Yes No c. Do you identify ony unususl varistions in the number of complimentary tickets issued? [You may select more than one answer, Single click the box with the question mork to produce a check mork for a correct answers and double click the box with the question mark to empty the box for o wrong answers.) Tickets issued by on undentified ogent 7 Duplicile ucket numbers issued by multiple agents. Usualy high number of complimentary uckets in Game 3 Unusual potherns of tichets ssued by Agent 2 ? Unusual pattems of tickets lasued by Agent 3 Unusual patsens of tichets assued by Agent 4 d. Do the patterns of timing of internet ticket sales appear reasonable? (You may select more than one answer. Single click the box with the question mork to produce a check mark for a correct answers and double click the box with the question mark to empty the box for a wrong answers.) No unusual patterns were detected - ticket sales dates appear random Ticket sales for Game 3 terminated early Ticket sales for Game 1 terminated late ? Ticket sales for Game 2 terminated early No spike in ticket sales during February No spike in ticket sales immediately prior to game e. Does the pricing of individual game and season tickets appear to be consistent with stated prices? Yes, ticket prices appear consistent with stated prices No, many individual game tickets sold for less than stated prices No, many individual game tickets sold for more than stated prices No, many season tickets sold for less than stated prices No, many season tickets sold for more than stated prices Required information Applying Data and Analytics to the Revenue Exercises G.33.G.38 require the use of Excel. Tableau, or other software in the revenue cycle audit. This case is loosely based on Floride State University (FSU) Footbell ticket revenues. Many of the facts and all of the transection-level date are fictitious, however. You have access to five Excel databsses obtained from your elient for use in auditing Football Ticket Revenue for the 2018 footboll season. Detailed information about the client and date dictionaries, olong with the required datasets, can be found below. Required Date Files: a. Dote Dietionary - Semiole Spirit Detailed lnformation b. Unsold tiekets by grme c. Season ticket soles revenue d. Champion's club ticket revenue e. Single gome tieket noles byosme f. 1sfued tickets by gome G.38 Considering the Adequacy of Data Provided by the Client Required: The schedules provided by the client for this analytical procedure lack many details that might be helpful to an auditor. Consider the columns provided by the client. What other information would you expect an ouditor to want for the purposes of analyzing the ressonableness of the data provided by the client and performing follow-up procedures? (You moy select more than one answer. single elick the box with the question mark to produce a check mark for a correct answers and double click the bok with the question mark to empty the box for a wrong onswers.) Qustomer phone numbers IDs of people receiving complimentary tickets Pnor year detailed soles information Scores of games Ticket prices for other sports teams Required information Information For Use with Billy's Big Box Bily's Big Box, Inc, (BBB) is a regional discount retailer that operates large discount stores in the southeastern United States. They compete directly in thelf markets with other "big box" stores. One hallmark of BBB is their generous return policy which ollows customers to retum ony item ot ony time within 90 doys for a full refund. B8B is also notable because they are much smaller in terms of number of stores - they only hove 20 stores throughout the region. Similar to many retailers, Be8 uses an end of January fiscal year end to allow for less uncertainty in holiday season sales returns. Although BBB allows customers great leniency in their return policy, their return rates hovve traditionally been in line with other retallers, and they estimate that opproximately 5% of their returns are fraudulent which is olso in line with other retaliers. This makes estimation of their sales retum allowances reasonably predictable, according to company management: BEB reports thet historically, epprodimately 10% of all sales are returned, 70% of these returns occur in the month immedlotely following the sole, 25\% occur within the next month, and the remoining 5% mostly hoppen in the third month. Later returns are immaterial since they are not according to policy.BBB estimates their returns using an "anolysis of economic conditions, historical average returns, as well as a variety of other sources". Because this method is ditficult to validate and is not os precise as your firm prefers. your firm has decided to test the estimate by preparing an estimate and comparing it to the client's using data collected from other sources on return rates, as well as using subsequent client information. Whenever an auditor uses Information Prepared by the Entity, that information must be tested for completeness and occuracy. For the purposes of the following exercises, please assume that your firm has already tested the completeness and accuracy of the Product Sales Summary and the Product Returns Summary and has determined that the amounts reported by the company are reasonable for purposes of your test of the sales return allowance account. You have access to the following data: BB8 Sales Returns Case Data The following is a data dictionary for the Retum Rates database, a dotabase created by your audit firm based on retail analysis of 40,000 stores performed by a retail analyst speciallst. These rates are used in all retall audits for yout firm The following is a data dictionary for the Product Sales Summary databose, which you have extracted for the last three months of the fiscel year ended 1/31/2021. The following is a data dictionary for the Product Returns Summary database, which you have extracted for the last three months of the fiscal year ended 1/312021, and aiso for the first month of the next year Feb. 2021). This database only includes returns related to sales made during the period of November-January of the year ended 1/31/2021, the relevant sales period for the Allowance for Sales Returns account. It is important to note that the client did not know about February returns as of end of year 1/31/2021. You hove been assigned to oudit the sales return and ollowance account for BBe Retall for the flscal year ended 1av2021. You hove been provided with the following information: - Information for use with 88 Retail documen - Return Rates dotabase - Product Sales Summary databese for November, 2020 - January, 2021 - Product Returns Summary dotobase for November, 2020-January. 2021 - The client G/L reports an Allowance for Sales Returns of \$3,100,000 as of 1/31/2021. - Your firm has set materiality for the Allowance for Soles Returns occount at $1,200,000 - For the purposes of this exercise, assume that seles occur uniformly throughout the year and month and that all months heve 30 doys. 6.39 In accessing and cleansing cilent deta, the auditor must consider the completeness and accuracy of the Information Produced by the Entity, as well as the appropriateness of the data for the purposes of the audit. Requiled: a. What are the total soles included in the Product Sales Summary database? (Round your answer to 2 decimal places.) Information For Use with Billy's Big Box Biy/s Big Box, lnc. (BBB) is a regional discoum retaller that operates large discount stores in the southeastern United States. They compete directly in their merkets with other "big box" stores. One hallmark of BBB is their generous retum policy which allows customers to return any item at any time within 90 doys for a full refund BBB is also notable because they ore much smaller in terms of number of stores - they only hove 20 stores throughout the region. Similer to many retallers, BBB uses an end of January fiscal year end to allow for less uncertainty in holidoy season sales returns. Although BBB allows customers great leniency in their retum policy, their return rates have traditionally been in line with other retallers, and they estimate that approwimstely 5% of their retums are froudulent, which is also in line with other retallers. This mokes estimotion of their sales return ollovances reasonobly predietable, occording to company martogement. BBB reports thet historically, opproximately 10% of all sales are returned. 70% of these retums occur in the month immedlotely folowing the sole, 25\% occur within the next month, and the remaining 5% mostly happen in the third month. Later retums are immaterial since they are not according to policyBBB estimates their returns using an "analysis of economic conditions. historical overage returmb. as well as a varlety of other sources". Becouse this method is difficult to volidate and is not as precise as your firm prefers, your firm has declded to test the estimote by preporing an estimote and comporing it to the client's using dota collected from other sources on return rates. as well as using subsequent client informatsen. Whenever an auditor uses information Prepered by the Entity, that information must be tested for completeness and accuracy. For the purposes of the following exercises, please assume that your firm has already tested the completeness and accuracy of the Product Sales Summary and the Product Returns Summary and has determined that the amounts reported by the company are reasonable for purposes of your test of the sales return allowance account. You have access to the following data: The following is a data dictionary for the Return Rates database, a database created by your auda firm based on retail analysis of 40,000 stores performed by a retail analyst specialist. These rates are used in oll retall audits for your flirm unless more soecific informetion is avsilable. analysis of 40,000 stores performed by a retoil analyst specialist. These rates are used in all retall audits for your firm unless more specific information is avallable. Colin Nerm PRODCEI KETRMIE Lhsque nequential psobuct caterory maber aned is retast andastry The prodact eategory that The rate of returna da the product categoet Coluen description Wislin type Nunerde Charartef Wimeate The following is a data dictionary for the Product Sales Summary database, which you have extracted for the last three months of the fiscal year ended 1/31/2021. months of the fiscal year ended 1/31/2021, and also for the first month of the next year Feb. 2021). This database only includes returns related to sales made during the period of November-January of the year ended 1/31/2021, the relevant sales period for the Allowance for Soles Retums account. It is important to note that the client did not know about February returns as of end of year 1/31/2021. In assessing the cleanliness of the data, are any of the following issues present in the database

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts