Question: Required information Exercise 6-21B Complete the accounting cycle using inventory transactions (LO6-2, 6-3, 6-5, 6-6, 6-7) (The following information applies to the questions displayed below.)

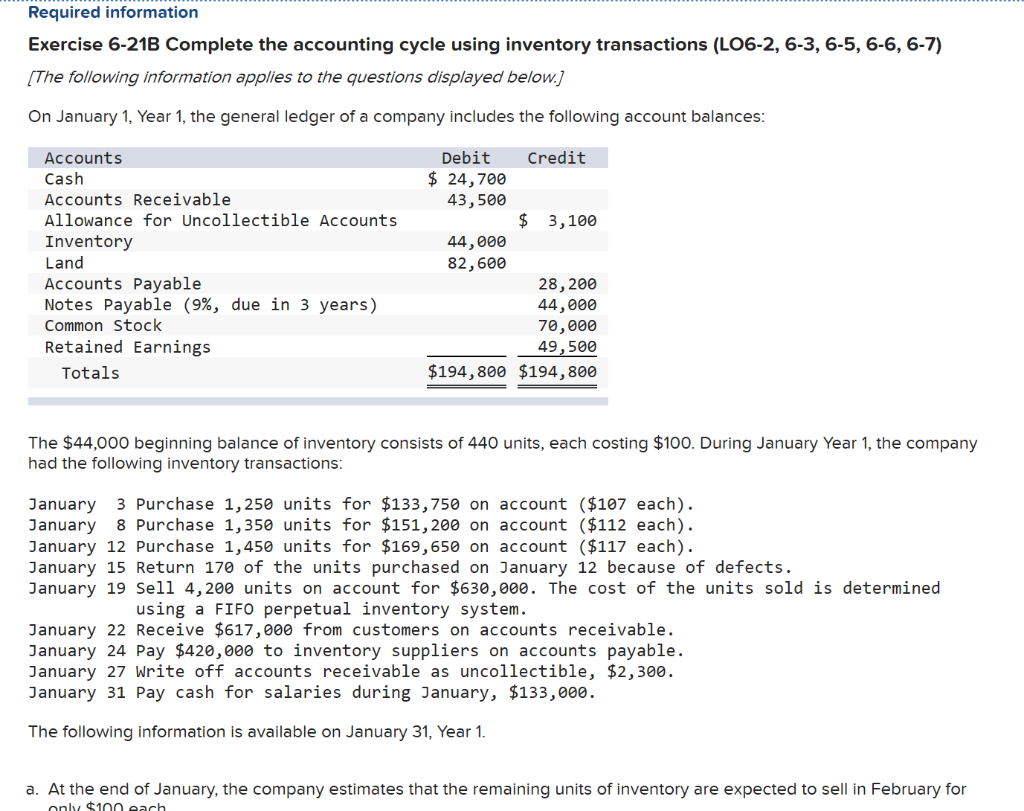

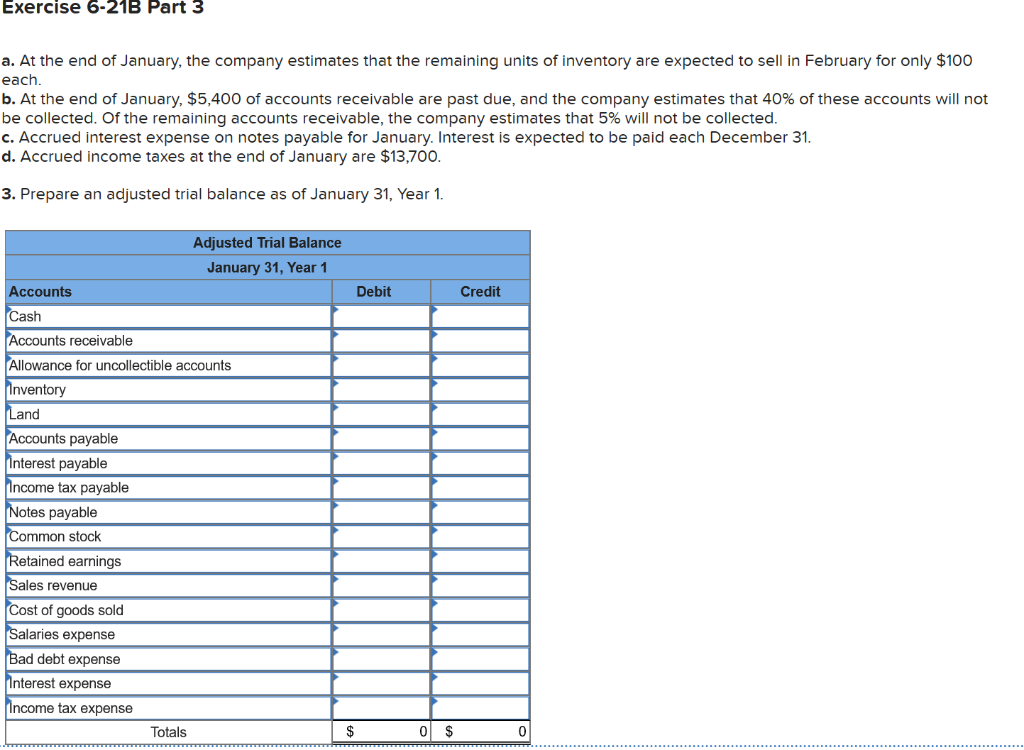

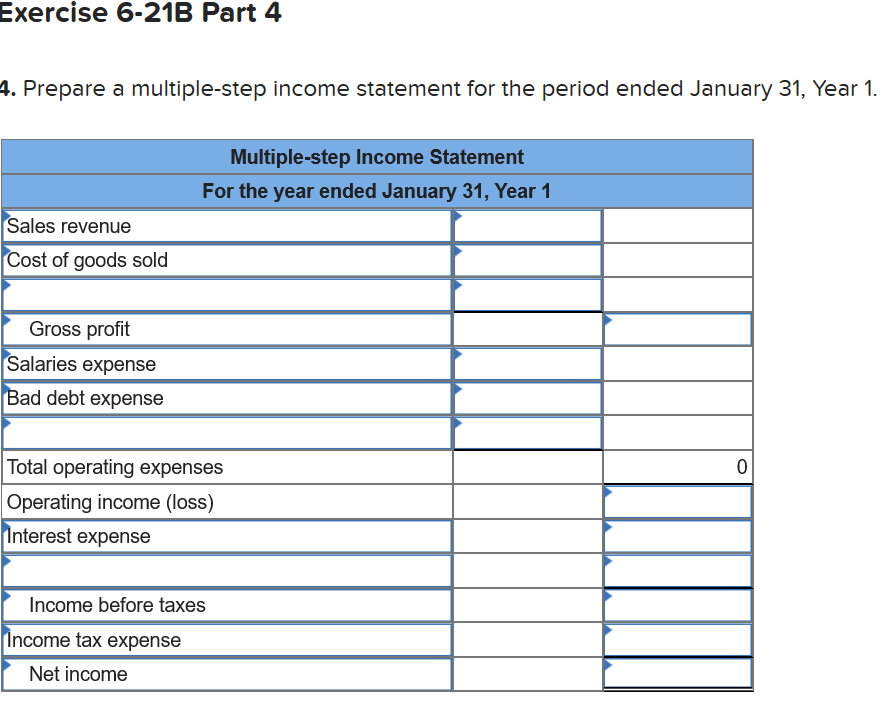

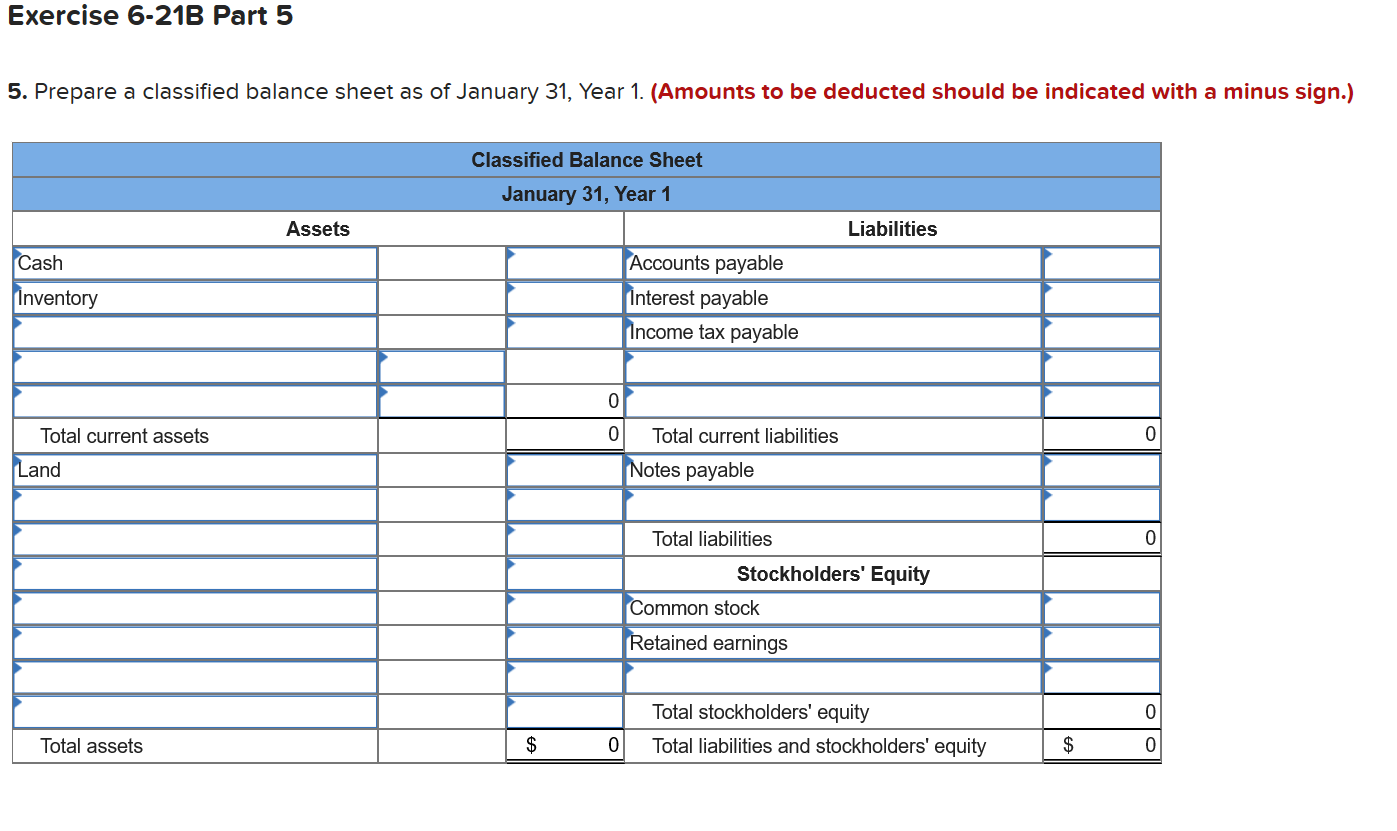

Required information Exercise 6-21B Complete the accounting cycle using inventory transactions (LO6-2, 6-3, 6-5, 6-6, 6-7) (The following information applies to the questions displayed below.) On January 1, Year 1, the general ledger of a company includes the following account balances: Accounts Cash Accounts Receivable Allowance for Uncollectible Accounts Inventory Land Accounts Payable Notes Payable (9%, due in 3 years) Common Stock Retained Earnings Totals Debit Credit $ 24,700 43,500 $ 3,100 44,000 82,600 28, 200 44,000 70,000 49,500 $194,800 $194,800 The $44,000 beginning balance of inventory consists of 440 units, each costing $100. During January Year 1, the company had the following inventory transactions: January 3 Purchase 1,250 units for $133,750 on account ($107 each). January 8 Purchase 1,350 units for $151,200 on account ($112 each). January 12 Purchase 1,450 units for $169,650 on account ($117 each). January 15 Return 170 of the units purchased on January 12 because of defects. January 19 Sell 4,200 units on account for $630,000. The cost of the units sold is determined using a FIFO perpetual inventory system. January 22 Receive $617,000 from customers on accounts receivable. January 24 Pay $420,000 to inventory suppliers on accounts payable. January 27 Write off accounts receivable as uncollectible, $2,300. January 31 Pay cash for salaries during January, $133,000. The following information is available on January 31, Year 1. a. At the end of January, the company estimates that the remaining units of inventory are expected to sell in February for only $100 each Exercise 6-21B Part 3 a. At the end of January, the company estimates that the remaining units of inventory are expected to sell in February for only $100 each. b. At the end of January, $5,400 of accounts receivable are past due, and the company estimates that 40% of these accounts will not be collected. Of the remaining accounts receivable, the company estimates that 5% will not be collected. c. Accrued interest expense on notes payable for January. Interest is expected to be paid each December 31. d. Accrued income taxes at the end of January are $13,700. 3. Prepare an adjusted trial balance as of January 31, Year 1. Debit Credit Adjusted Trial Balance January 31, Year 1 Accounts Cash Accounts receivable Allowance for uncollectible accounts Inventory Land Accounts payable Interest payable Income tax payable Notes payable i Common stock Retained earnings Sales revenue Cost of goods sold Salaries expense Bad debt expense Interest expense Income tax expense Totals 0 $ Exercise 6-21B Part 4 4. Prepare a multiple-step income statement for the period ended January 31, Year 1. Multiple-step Income Statement For the year ended January 31, Year 1 Sales revenue Cost of goods sold Gross profit Salaries expense Bad debt expense Total operating expenses Operating income (loss) Interest expense Income before taxes Income tax expense Net income Exercise 6-21B Part 5 5. Prepare a classified balance sheet as of January 31, Year 1. (Amounts to be deducted should be indicated with a minus sign.) Classified Balance Sheet January 31, Year 1 Assets Liabilities Cash Inventory Accounts payable Interest payable Income tax payable Total current assets 0 01 Total current liabilities Notes payable Land Total liabilities Stockholders' Equity Common stock Retained earnings Total stockholders' equity Total liabilities and stockholders' equity Total assets Required information Exercise 6-21B Complete the accounting cycle using inventory transactions (LO6-2, 6-3, 6-5, 6-6, 6-7) (The following information applies to the questions displayed below.) On January 1, Year 1, the general ledger of a company includes the following account balances: Accounts Cash Accounts Receivable Allowance for Uncollectible Accounts Inventory Land Accounts Payable Notes Payable (9%, due in 3 years) Common Stock Retained Earnings Totals Debit Credit $ 24,700 43,500 $ 3,100 44,000 82,600 28, 200 44,000 70,000 49,500 $194,800 $194,800 The $44,000 beginning balance of inventory consists of 440 units, each costing $100. During January Year 1, the company had the following inventory transactions: January 3 Purchase 1,250 units for $133,750 on account ($107 each). January 8 Purchase 1,350 units for $151,200 on account ($112 each). January 12 Purchase 1,450 units for $169,650 on account ($117 each). January 15 Return 170 of the units purchased on January 12 because of defects. January 19 Sell 4,200 units on account for $630,000. The cost of the units sold is determined using a FIFO perpetual inventory system. January 22 Receive $617,000 from customers on accounts receivable. January 24 Pay $420,000 to inventory suppliers on accounts payable. January 27 Write off accounts receivable as uncollectible, $2,300. January 31 Pay cash for salaries during January, $133,000. The following information is available on January 31, Year 1. a. At the end of January, the company estimates that the remaining units of inventory are expected to sell in February for only $100 each Exercise 6-21B Part 3 a. At the end of January, the company estimates that the remaining units of inventory are expected to sell in February for only $100 each. b. At the end of January, $5,400 of accounts receivable are past due, and the company estimates that 40% of these accounts will not be collected. Of the remaining accounts receivable, the company estimates that 5% will not be collected. c. Accrued interest expense on notes payable for January. Interest is expected to be paid each December 31. d. Accrued income taxes at the end of January are $13,700. 3. Prepare an adjusted trial balance as of January 31, Year 1. Debit Credit Adjusted Trial Balance January 31, Year 1 Accounts Cash Accounts receivable Allowance for uncollectible accounts Inventory Land Accounts payable Interest payable Income tax payable Notes payable i Common stock Retained earnings Sales revenue Cost of goods sold Salaries expense Bad debt expense Interest expense Income tax expense Totals 0 $ Exercise 6-21B Part 4 4. Prepare a multiple-step income statement for the period ended January 31, Year 1. Multiple-step Income Statement For the year ended January 31, Year 1 Sales revenue Cost of goods sold Gross profit Salaries expense Bad debt expense Total operating expenses Operating income (loss) Interest expense Income before taxes Income tax expense Net income Exercise 6-21B Part 5 5. Prepare a classified balance sheet as of January 31, Year 1. (Amounts to be deducted should be indicated with a minus sign.) Classified Balance Sheet January 31, Year 1 Assets Liabilities Cash Inventory Accounts payable Interest payable Income tax payable Total current assets 0 01 Total current liabilities Notes payable Land Total liabilities Stockholders' Equity Common stock Retained earnings Total stockholders' equity Total liabilities and stockholders' equity Total assets

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts