Question: Required information While James Craig and his former classmate Paul Dolittle both studied accounting at school, they ended up pursuing careers in professional cake decorating.

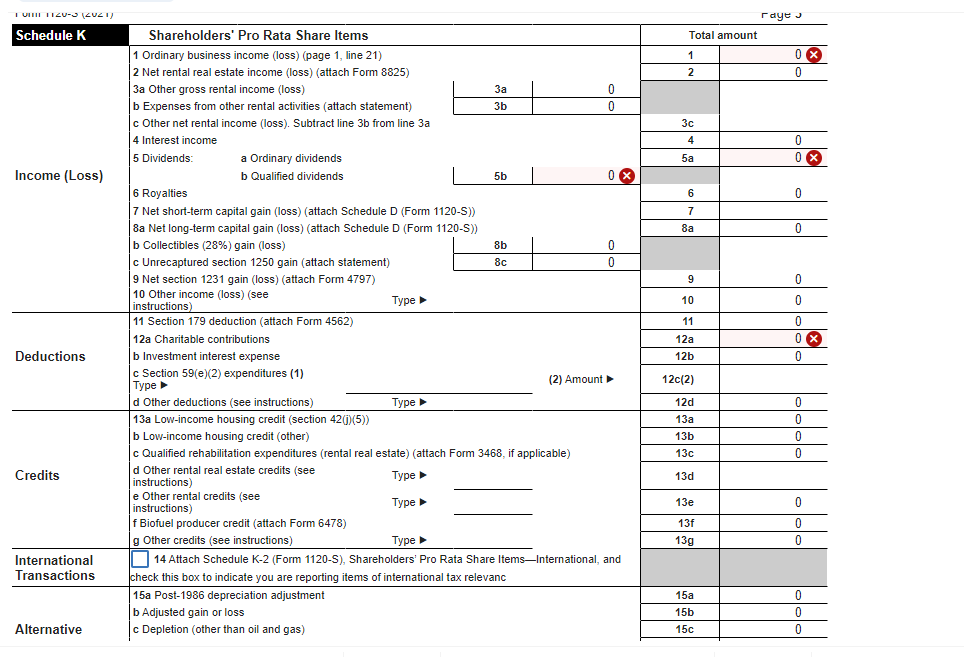

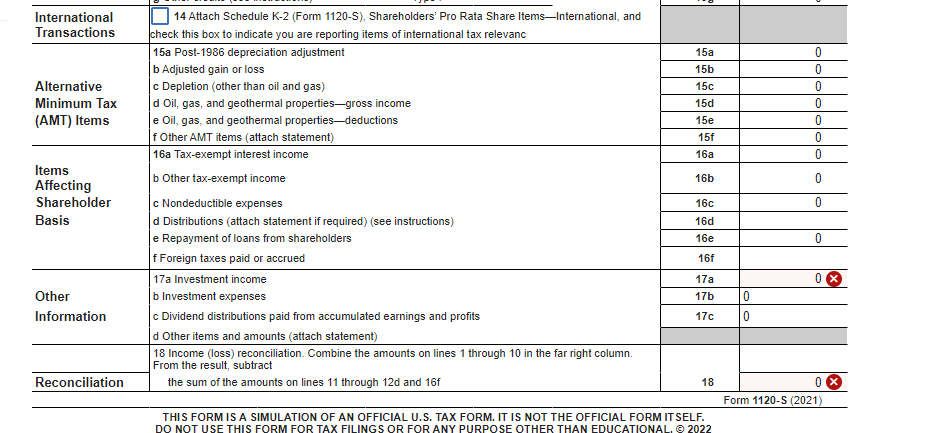

Required information While James Craig and his former classmate Paul Dolittle both studied accounting at school, they ended up pursuing careers in professional cake decorating. Their company, Good to Eat (GTE), specializes in custom-sculpted cakes for weddings, birthdays, and other celebrations. James and Paul formed the business at the beginning of 2022, and each contributed $100,000 in exchange for a 50 percent ownership interest. GTE also borrowed $400,000 from a local bank. Both James and Paul had to personally guarantee the loan. Both owners provide significant services for the business. The following information pertains to GTE's 2022 activities: . GTE uses the cash method of accounting (for both book and tax purposes) and reports income on a calendar-year basis. . GTE received $700,000 of sales revenue and reported $330,000 of cost of goods sold (it did not have any ending inventory). . GTE paid $55,000 compensation to James, $55,000 compensation to Paul, and $65,000 of compensation to other employees (assume these amounts include applicable payroll taxes, if any). . GTE paid $20,000 of rent for a building and equipment, $25,000 for advertising, $28,000 in interest expense, $4,500 for utilities, and $2,500 for supplies. . GTE contributed $7,500 to charity. . GTE received a $2,000 qualified dividend from a great stock investment (it owned 2 percent of the corporation distributing the dividend), and it recognized $2,000 in short-term capital gain when it sold some of the stock. . On December 1, 2022, GTE distributed $25,000 to James and $25,000 to Paul. . GTE has qualified property of $305,000 (unadjusted basis). Note: Leave no answers blank. Enter zero if applicable. Enter N/A if not applicable. a-1. Assume James and Paul formed GTE as an $ corporation.1 0III 120-3 (2021) Taye J Schedule K Shareholders' Pro Rata Share Items Total amount 1 Ordinary business income (loss) (page 1, line 21) 1 0 x 2 Net rental real estate income (loss) (attach Form 8825) 2 0 3a Other gross rental income (loss) b Expenses from other rental activities (attach statement) 3b c Other net rental income (loss). Subtract line 3b from line 3a 3c 4 Interest income A 0 5 Dividends: a Ordinary dividends 5a O X Income (Loss) b Qualified dividends 5b O X 6 Royalties 6 0 7 Net short-term capital gain (loss) (attach Schedule D (Form 1120-5)) 7 Ba Net long-term capital gain (loss) (attach Schedule D (Form 1120-S)) a 0 b Collectibles (28%) gain (loss) 8b c Unrecaptured section 1250 gain (attach statement) c 9 Net section 1231 gain (loss) (attach Form 4797) 9 10 Other income (loss) (see Type 10 instructions 11 Section 179 deduction (attach Form 4562) 11 0 12a Charitable contributions 12a O X Deductions b Investment interest expense 12b 0 c Section 59(e)(2) expenditures (1) Type (2) Amount 12c(2) d Other deductions (see instructions) Type D 12d 0 13a Low-income housing credit (section 420)(5)) 13a 0 b Low-income housing credit (other) 13b 0 c Qualified rehabilitation expenditures (rental real estate) (attach Form 3468, if applicable) 13c 0 Credits d Other rental real estate credits (see Type 13d instructions) e Other rental credits (see Type 13e instructions) 0 f Biofuel producer credit (attach Form 6478) 13f 0 g Other credits (see instructions) Type 13g 0 International 14 Attach Schedule K-2 (Form 1120-5), Shareholders' Pro Rata Share Items-International, and Transactions check this box to indicate you are reporting items of international tax relevanc 15a Post-1986 depreciation adjustment 152 0 b Adjusted gain or loss 15b 0 Alternative c Depletion (other than oil and gas) 15c 0International I:I 14 Attach Schedule K-2 (Form 1120-5), Shareholders' Pro Rata Share ltemsInternatienal. and Transactions heck this box to indicate you are reporfing items of international tax relevanc 156a Post-1956 depreciation adjustment 15a 0 b Adjusted gain or loss 15b 0 Alternative Deplation (other than oil and gas) 15 0 Minimum Tax d Oil, gas, and geothermal propertiesgross income 15d 0 (AMT]) ltems 0il, gas, and geothermal propertiesdeductions 15 0 f Other AMT items (attach statement) 15f 0 18a Tax-exempt interest income 16a 0 E?fr:sting b Other fax-exempt income 16b 0 Shareholder Mondeductible expenses 16c 0 Basis d Disfributions (attach statement if required) (see insiructions) 16d e Repayment of loans frem shareholders 16e 0 f Foreign taxes paid or accrued 16f 17a Invesiment income 17a 0 &3 Other b Investment expenses 17b 0 Information Dividend distributions paid from accumulated earnings and profits 17c ] d Other items and amounts (attach statement) 18 Income (loss) reconciliation. Combine the amounts on lines 1 through 10 in the far right column. From the result, subtract Reconciliation the sum of the amounts on lines 11 through 12d and 16f 18 0 a THIS FORM 15 A SIMULATION OF AN OFFICIAL U.5. TAX FORM. IT IS NOT THE OFFICIAL FORM IT SELF. DO NOT USE THIS FORM FOR TAX FILINGS OR FOR ANY PURPOSE OTHER THAN EDUCATIONAL, @ 2022 Form 1120-5 (2021)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!