Question: Required: Prepare Extraction Process account. Prepare Blending Process account by showing all relevant statements. Prepare Normal loss, Abnormal loss/gain account. (if any) Explain TWO (2)

Required:

- Prepare Extraction Process account.

- Prepare Blending Process account by showing all relevant statements.

- Prepare Normal loss, Abnormal loss/gain account. (if any)

- Explain TWO (2) methods of allocating joint cost other than physical unit value method.

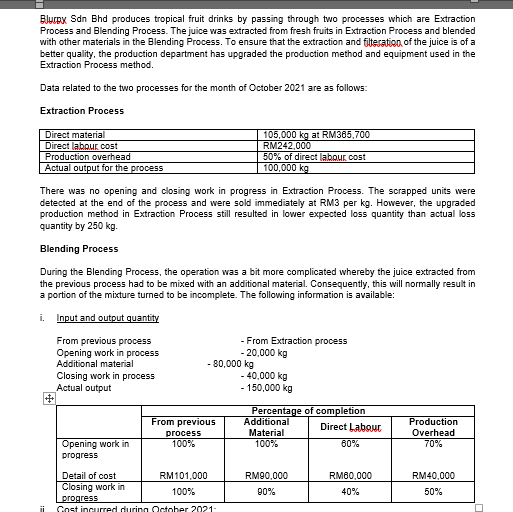

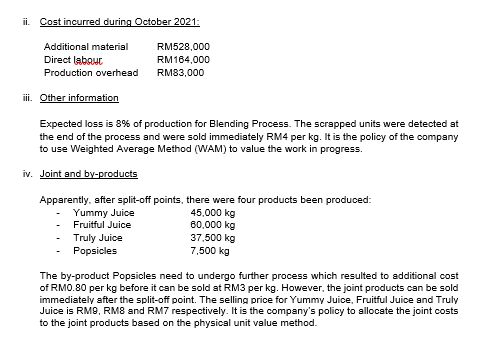

Bluspx Sdn Bhd produces tropical fruit drinks by passing through two processes which are Extraction Process and Blending Process. The juice was extracted from fresh fruits in Extraction Process and blended with other materials in the Blending Process. To ensure that the extraction and filteration of the juice is of a better quality, the production department has upgraded the production method and equipment used in the Extraction Process method. Data related to the two processes for the month of October 2021 are as follows: Extraction Process Direct material Direct labour cost Production overhead Actual output for the process 105,000 kg at RM365,700 RM242,000 50% of direct labour cost 100,000 kg There was no opening and closing work in progress in Extraction Process. The scrapped units were detected at the end of the process and were sold immediately at RM3 per kg. However, the upgraded production method in Extraction Process still resulted in lower expected loss quantity than actual loss quantity by 250 kg Blending Process During the Blending Process, the operation was a bit more complicated whereby the juice extracted from the previous process had to be mixed with an additional material. Consequently, this will normally result in a portion of the mixture turned to be incomplete. The following information is available: i. Input and output quantity From previous process - From Extraction process Opening work in process - 20.000 kg Additional material - 80,000 kg Closing work in process - 40,000 kg Actual output - 150,000 kg From previous process 100% Percentage of completion Additional Direct Labout Material 100% 80% Production Overhead 70% Opening work in progress Detail of cost RM 101,000 Closing work in 100% progress fost incurred durinn October 2021 RM90,000 90% RM60,000 40% RM40,000 50% . Cost incurred during October 2021: Additional material Direct labour Production overhead RM528,000 RM164,000 RM83,000 ii. Other information Expected loss is 3% of production for Blending Process. The scrapped units were detected at the end of the process and were sold immediately RM4 per kg. It is the policy of the company to use Weighted Average Method (WAM) to value the work in progress. iv. Joint and by-products Apparently, after split-off points, there were four products been produced: Yummy Juice 45,000 kg Fruitful Juice 60,000 kg Truly Juice 37.500 kg Popsicles 7.500 kg The by-product Popsicles need to undergo further process which resulted to additional cost of RM0.80 per kg before it can be sold at RM3 per kg. However, the joint products can be sold immediately after the split-off point. The selling price for Yummy Juice, Fruitful Juice and Truly Juice is RM9, RM8 and RM7 respectively. It is the company's policy to allocate the joint costs to the joint products based on the physical unit value method. Bluspx Sdn Bhd produces tropical fruit drinks by passing through two processes which are Extraction Process and Blending Process. The juice was extracted from fresh fruits in Extraction Process and blended with other materials in the Blending Process. To ensure that the extraction and filteration of the juice is of a better quality, the production department has upgraded the production method and equipment used in the Extraction Process method. Data related to the two processes for the month of October 2021 are as follows: Extraction Process Direct material Direct labour cost Production overhead Actual output for the process 105,000 kg at RM365,700 RM242,000 50% of direct labour cost 100,000 kg There was no opening and closing work in progress in Extraction Process. The scrapped units were detected at the end of the process and were sold immediately at RM3 per kg. However, the upgraded production method in Extraction Process still resulted in lower expected loss quantity than actual loss quantity by 250 kg Blending Process During the Blending Process, the operation was a bit more complicated whereby the juice extracted from the previous process had to be mixed with an additional material. Consequently, this will normally result in a portion of the mixture turned to be incomplete. The following information is available: i. Input and output quantity From previous process - From Extraction process Opening work in process - 20.000 kg Additional material - 80,000 kg Closing work in process - 40,000 kg Actual output - 150,000 kg From previous process 100% Percentage of completion Additional Direct Labout Material 100% 80% Production Overhead 70% Opening work in progress Detail of cost RM 101,000 Closing work in 100% progress fost incurred durinn October 2021 RM90,000 90% RM60,000 40% RM40,000 50% . Cost incurred during October 2021: Additional material Direct labour Production overhead RM528,000 RM164,000 RM83,000 ii. Other information Expected loss is 3% of production for Blending Process. The scrapped units were detected at the end of the process and were sold immediately RM4 per kg. It is the policy of the company to use Weighted Average Method (WAM) to value the work in progress. iv. Joint and by-products Apparently, after split-off points, there were four products been produced: Yummy Juice 45,000 kg Fruitful Juice 60,000 kg Truly Juice 37.500 kg Popsicles 7.500 kg The by-product Popsicles need to undergo further process which resulted to additional cost of RM0.80 per kg before it can be sold at RM3 per kg. However, the joint products can be sold immediately after the split-off point. The selling price for Yummy Juice, Fruitful Juice and Truly Juice is RM9, RM8 and RM7 respectively. It is the company's policy to allocate the joint costs to the joint products based on the physical unit value method

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts