Question: REQUIRED SOFTWARE: To enable solver in MS Excel, select File Options > Add-Ins Analysis tool pack, click Go check Solver. It will now appear in

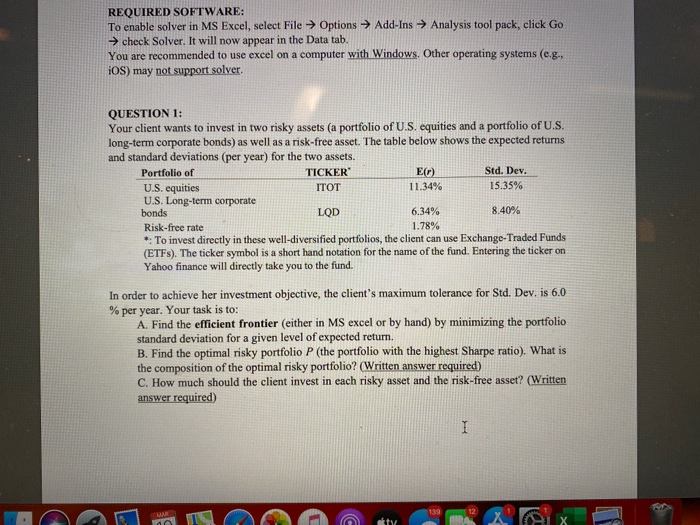

REQUIRED SOFTWARE: To enable solver in MS Excel, select File Options > Add-Ins Analysis tool pack, click Go check Solver. It will now appear in the Data tab. You are recommended to use excel on a computer with Windows. Other operating systems (e.g., iOS) may not support solver. QUESTION 1: Your client wants to invest in two risky assets (a portfolio of U.S. equities and a portfolio of U.S. long-term corporate bonds) as well as a risk-free asset. The table below shows the expected returns and standard deviations (per year) for the two assets. Portfolio of TICKER EO) Std. Dev. U.S. equities ITOT 11.34% 15.35% U.S. Long-term corporate bonds LOD 6.34% 8 409 Risk-free rate 1.78% *: To invest directly in these well-diversified portfolios, the client can use Exchange-Traded Funds (ETF). The ticker symbol is a short hand notation for the name of the fund. Entering the ticker on Yahoo finance will directly take you to the fund. In order to achieve her investment objective, the client's maximum tolerance for Std. Dev. is 6.0 % per year. Your task is to: A. Find the efficient frontier (either in MS excel or by hand) by minimizing the portfolio standard deviation for a given level of expected return. B. Find the optimal risky portfolio P (the portfolio with the highest Sharpe ratio). What is the composition of the optimal risky portfolio? (Written answer required) C. How much should the client invest in each risky asset and the risk-free asset? (Written answer required) AOOOX REQUIRED SOFTWARE: To enable solver in MS Excel, select File Options > Add-Ins Analysis tool pack, click Go check Solver. It will now appear in the Data tab. You are recommended to use excel on a computer with Windows. Other operating systems (e.g., iOS) may not support solver. QUESTION 1: Your client wants to invest in two risky assets (a portfolio of U.S. equities and a portfolio of U.S. long-term corporate bonds) as well as a risk-free asset. The table below shows the expected returns and standard deviations (per year) for the two assets. Portfolio of TICKER EO) Std. Dev. U.S. equities ITOT 11.34% 15.35% U.S. Long-term corporate bonds LOD 6.34% 8 409 Risk-free rate 1.78% *: To invest directly in these well-diversified portfolios, the client can use Exchange-Traded Funds (ETF). The ticker symbol is a short hand notation for the name of the fund. Entering the ticker on Yahoo finance will directly take you to the fund. In order to achieve her investment objective, the client's maximum tolerance for Std. Dev. is 6.0 % per year. Your task is to: A. Find the efficient frontier (either in MS excel or by hand) by minimizing the portfolio standard deviation for a given level of expected return. B. Find the optimal risky portfolio P (the portfolio with the highest Sharpe ratio). What is the composition of the optimal risky portfolio? (Written answer required) C. How much should the client invest in each risky asset and the risk-free asset? (Written answer required) AOOOX

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts