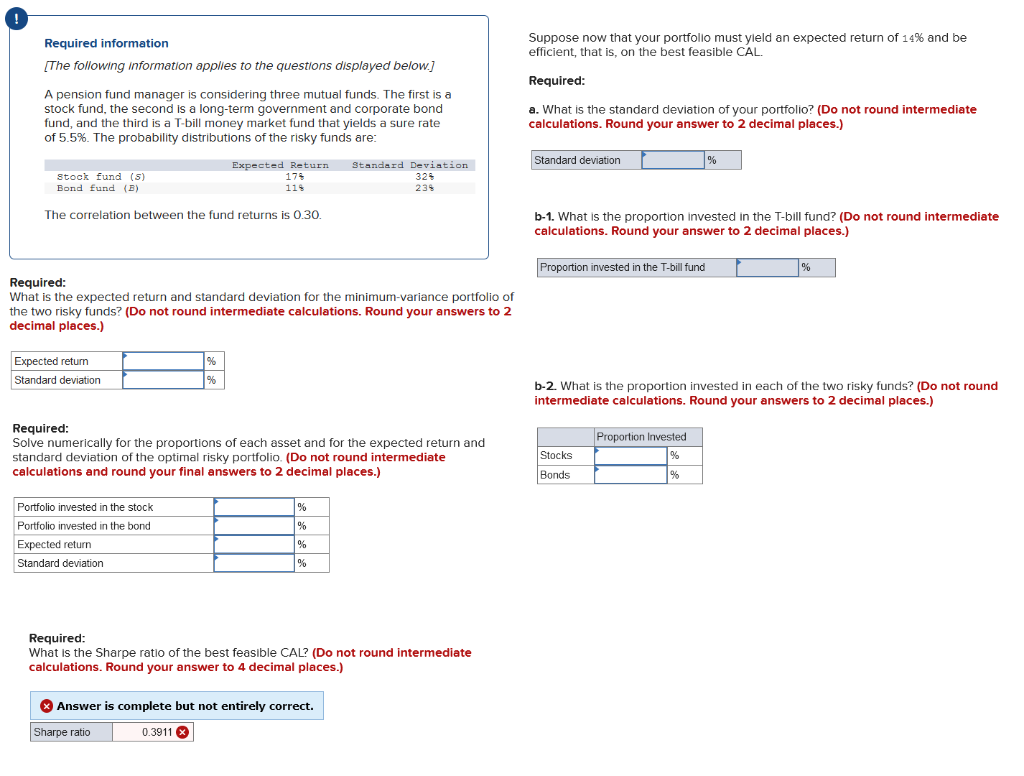

Question: Required: What is the expected return and standard deviation for the minimum-variance portfolio of the two risky funds? (Do not round intermediate calculations. Round your

Required: What is the expected return and standard deviation for the minimum-variance portfolio of the two risky funds? (Do not round intermediate calculations. Round your answers to 2 decimal places.) b-2. What is the proportion invested in each of the two risky funds? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Required: Solve numerically for the proportions of each asset and for the expected return and standard deviation of the optimal risky portfolio. (Do not round intermediate calculations and round your final answers to 2 decimal places.) Required: What is the Sharpe ratio of the best feasible CAL? (Do not round intermediate calculations. Round your answer to 4 decimal places.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts