Requirements Calculate the net undiscounted and discount cash flows that you would use in the impairment tests.

Question:

Requirements

- Calculate the net undiscounted and discount cash flows that you would use in the impairment tests.

- Explain why the discount rate used to calculate discounted cash flows is appropriate for use in impairment testing.

All Information Given

ABSTRACT

This case introduces impairment of long-lived assets and intangible assets including goodwill. Students must analyze uncertainties in a fact situation including consideration of the impact of diversity in the application generally accepted accounting principles (GAAP) and financial statement outcomes. There is allowed diversity in accounting that can contribute to complexities in determining appropriate accounting treatment and financial statement presentation for an event, transaction, or item. As a result, different companies operating in the same industry sector will have results that differ not just on operational factors but based on the accounting methodologies applied. Students are provided with an opportunity to expand their understanding of GAAP and develop research skills related to accounting guidance and resources through the case requirements. Furthermore, the case provides students an opportunity to practice applying judgment and application of critical thinking as it relates to determining the impact of differences in allowed accounting treatments and financial statement presentation.

Keywords: accounting diversity, Accounting Standards Codification, ASC, depreciation,

financial statement presentation, generally accepted accounting principles, GAAP, impairment.

INTRODUCTION

Determining the appropriate accounting treatment for an event, transaction, or item requires an understanding of the authoritative guidance in the Financial Accounting Standards Board's (FASB) Accounting Standards Codification (ASC) and Securities and Exchange Commission (SEC) rules, regulations, and interpretations. The sources of authoritative accounting guidance may indicate (1) specific guidance directly applicable to the type of event, transaction, or item including the choice of applying optional methodologies; (2) alternative guidance related to a similar events, transactions, or item; or (3) a lack of specific or alternative guidance. In the absence of specific or alternative authoritative guidance, the FASB ASC allows for the use of analogy when determining an appropriate accounting treatment. If authoritative guidance is not available, the use of nonauthoritative guidance is appropriate. In addition, the SEC has allowed and recognizes diversity in accounting practice by public registrants.[1] This diversity not only results in differences in the financial statement of companies operating in the same industry sector but can also impact subsequent accounting results when (a) companies sell or dispose of inventory or assets held for productive use or (b) events lead to the impairment of inventory or assets held for productive use. Determining the appropriateness of an accounting treatment also requires understanding of the hierarchy of generally accepted accounting principles (GAAP) when considering the applicability of nonauthoritative guidance in superseded FASB, Accounting Principles Board (APB), and Accounting Research Bulletin (ARB) guidance and

other sources of identified accounting guidance.

THE CASE

It is late March 2020 and you are a first-year accounting analyst in the financial reporting area at All World Airways (AWA). You have just finished your first yearend close and reporting process. Other staff have told you the yearend activities were more hectic than usual due to concerns about the COVID-19 virus and how it may impact AWA's operations. While the annual report and Form 10-K were being finalized, you and other members of the financial reporting staff was also researching GAAP on impairment and preparing for potential disclosures to be released in a Form 8-K filing and the first quarter 10-Q filing. AWA's controller, Dirk Carre, has asked you to document the process that should be used to determine whether, or which, AWA assets are impaired, to calculate an impairment estimate including support for the discount rate used in your estimates, and draft a report for presentation to executive management and the BOD that supports the analyses and conclusions resulting from your research.

Background

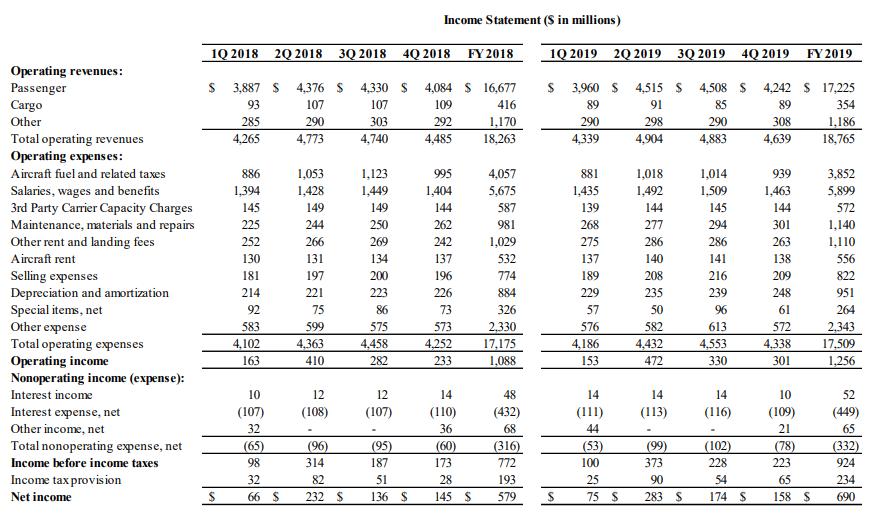

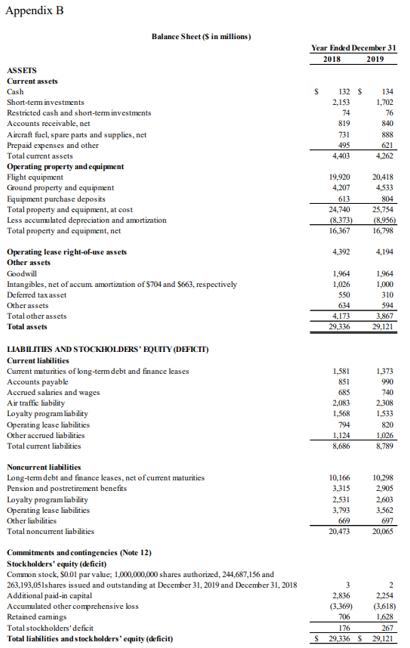

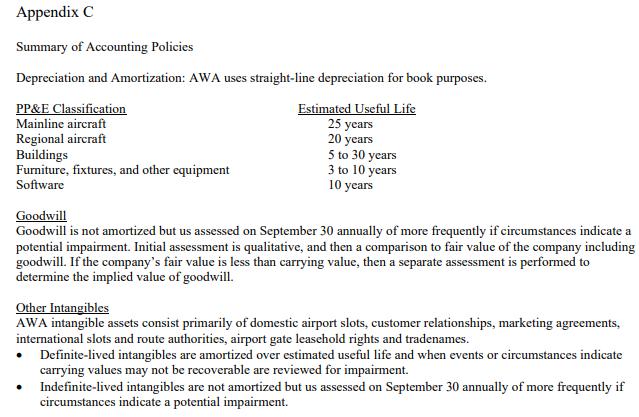

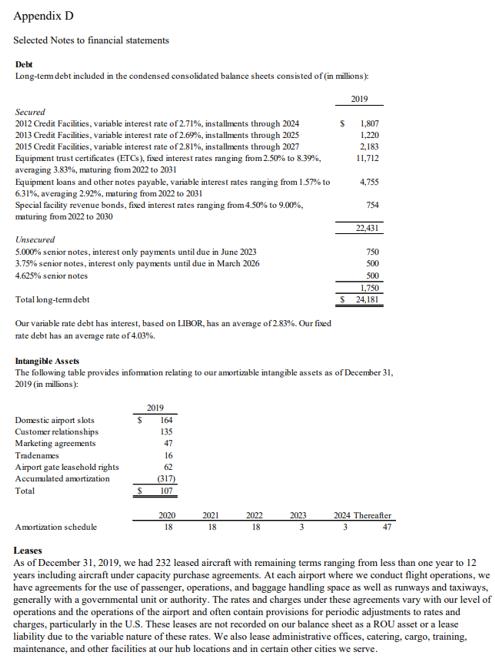

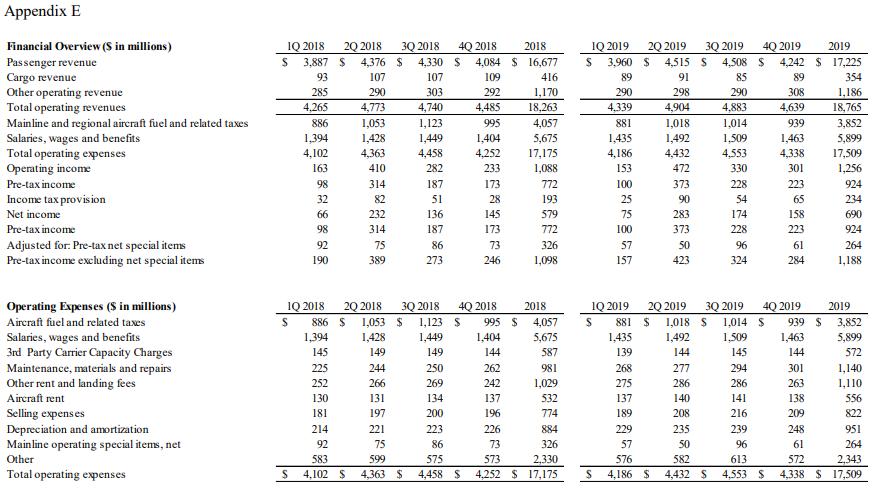

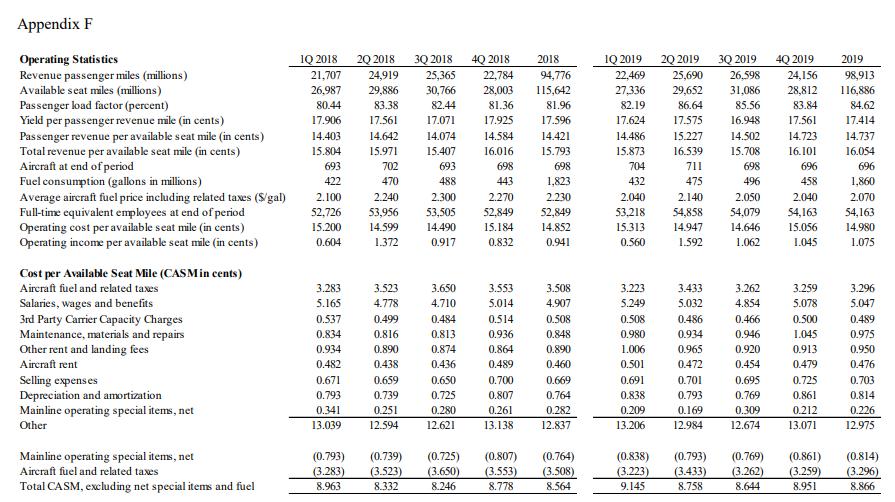

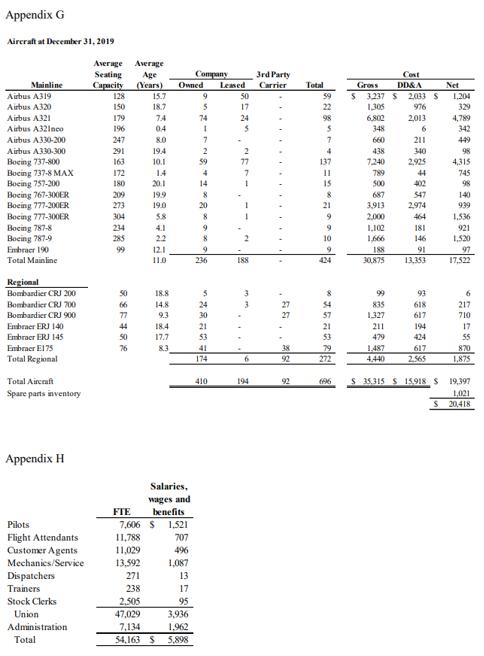

AWA is an U.S. based international air carrier. During 2019, AWA achieved profitable operations and significant improvements in its on-time departures and arrivals. AWA increased its passenger load factor approximately 3% and passenger revenue per available seat mile by approximately 2%. AWA's revenue and operating results are subject to seasonality. Historically, the 2 nd and 3 rd quarters of each year see the highest revenue and operating costs due to the vacation travel season with increased passenger flows in the May through August period. For 2019, AWA's operating income was $ 1.257 billion and net income of $ 691 million on $ 18.765 billion of revenue. AWA financial data and operating statistics are presented in Appendices A, B, C, D, E, and F. At the end of 2019, AWA's fleet consisted of 696 aircraft supported by 54,163 employees. For information on AWA's fleet and employees, see Appendices G and H

The Board of Directors (BOD) has set AWA's priorities as efficient and profitable growth to generate significant free cash flow through customer satisfaction and operational excellence. Based on various studies, the BOD believes becoming the customer's airline of choice is based on operational excellence achieved through reliability and scheduling. In addition, the BOD and AWA management believe operational excellence is dependent on having and maintaining a fuel-efficient fleet. Over the years, AWA fleet has replaced and upgraded through a significant capital investments program which is achieving desired results. With a future capital investment profile based on maintaining rather than growing a fuel-efficient fleet through replacement of older less efficient aircraft, AWA believes it is well positioned to strategically expand its operations and fleet in high growth and revenue markets. AWA's focus is generating returns to shareholders and de-levering its balance sheet (i.e., reducing debt) through profitable operations in existing markets and growth in new markets. In recent years, AWA has paid dividends that have averaged 1.7% annually. The AWA BOD would like to increase these payouts. Like its competitors, AWA has also been dealing with Boeing 737 MAX aircraft issues. AWA's fleet includes 11 Boeing 737 MAX aircraft with an additional 34 on order for future delivery. Due to safety concerns, on March 13, 2019, the U.S. Federal Aviation Administration (FAA) grounded all U.S. registered Boeing 737 MAX aircraft. AWA cancelled roughly 12,000 flights during the last three quarters of 2019 and removed all Boeing 737 MAX aircraft from its flight schedule through the first two quarters of 2020 while continuing to assess the FAA and Boeing timelines for resolution of the Boeing 737 MAX aircraft issues.

Issues and AWA's Planned Approaches

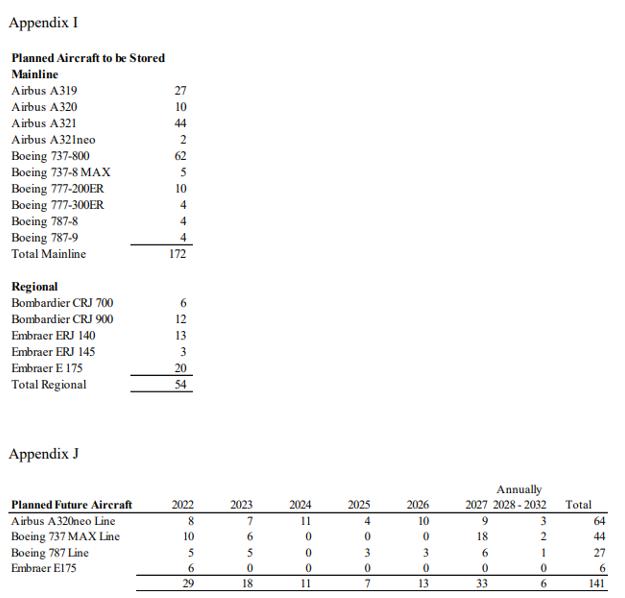

In early 2020, the World Health Organization declared COVID-19 which surfaced in nearly all regions of the world to be a global health pandemic. Government imposed and implemented significant measures in attempts to prevent or reduce spread of COVID-19. These measures include travel restrictions, border closings, "shelter in place" orders, and business closures led to an unprecedented decline in the demand for air travel. During the first two months of 2020, AWA's business performed largely as expected; however, a severe reduction in air travel during March 2020 led to AWA's total operating revenues decreasing nearly 25% in the first quarter of 2020 compared to the first quarter of 2019. As a result, AWA expects the deterioration to increase in the second quarter of 2020 with results of operations to be severely impacted for the balance of 2020 and possibly into early 2022. Based on the lack of COVID- 19 information, there is significant uncertainty on the potential length and severity of the pandemic. AWA expects significant business volatility during the pandemic period with future demand for aircraft travel difficult to forecast accurately in the near and long term. In response to COVID-19, AWA plans on taking forceful actions to reconfigure of fleet, reduce capacity significantly, reduce costs, and improve our liquidity, and preserve cash. Planned changes to capacity are based on expectation that AWA's demand will be 80%, 70, and 60% lower for the 2 nd , 3 rd , and 4 th quarters of 2020 compared to its 2019 results. For 2021, AWA expects the 1 st quarter to be consistent with the 4 th quarter of 2020 then a recovery beginning in the 2 nd quarter growing demand by 25 to 30% quarterly until full recovery occurs on the 1 st or 2 nd quarter of 2022. After full recovery, AWA expects to future growth of 1 to 2 percent annually (excluding inflation) from its existing fleet with additional growth from planned aircraft additions (see Appendix J). AWA's estimates and forecast are subject to the conditions and government mandates in the jurisdictions in which AWA operates. Based on the estimates and the forecast, AWA is accelerating the retirement of less efficient mainline aircraft as well as certain regional aircraft. This action reduces the complexity of AWA's fleet, creates maintenance costs reductions, and brings other savings from operating fewer aircraft types forward in time. Aircraft to be retired include the Airbus A330, Boeing 757 and 767, Embraer 140 and 190, and Bombardier CRJ 200 portions of AWA's fleet. AWA will also temporarily store some AWA owned aircraft including Boeing 737-800, Bombardier CRJ 700 and 900, and Embraer 145 and 175 aircraft. See Appendix I for planned aircraft storage information. While AWA is retiring some aircraft and storing others due to the forecasted changes in capacity, AWA has decided to maintain its relationships with 3rd party carriers and presence in the various airports serving its markets. In the interim periods, however, AWA plans to consolidate its airport facility space. AWA is also deferring marketing expenses, reducing and deferring maintenance expenses, and reducing contractor, event, and training expenses. To address personnel costs, AWA has implemented a hiring freeze for non-essential positions, paused non-contractual pay raises, implemented both voluntary partially paid leave and early retirement programs, and reduced executive and BOD compensation. These actions will reduce AWA's Administration staffing by 33% and operating staff by 20% for early retirement with a similar reduction for involuntary furloughs. Finally, AWA is deferring the timing and expenditure on future aircraft deliveries into 2022 and later periods.

Expert Answer:

It appears youve posted a scenario and accompanying appendices with detailed financial information about a hypothetical company named All World Airway... View the full answer

Financial Accounting A User Perspective

ISBN: 978-0470676608

6th Canadian Edition

Authors: Robert E Hoskin, Maureen R Fizzell, Donald C Cherry