Question: Retirement Planning Case Study Fall 2024 Part 1 and Part 2 of the assignment should be submitted in excel. Part 3 of the assignment is

Retirement Planning Case Study Fall 2024

Part 1 and Part 2 of the assignment should be submitted in excel. Part 3 of the assignment is a report to the clients and needs to be submitted in a word file. Any tables needed for the report should also be included in the word file.

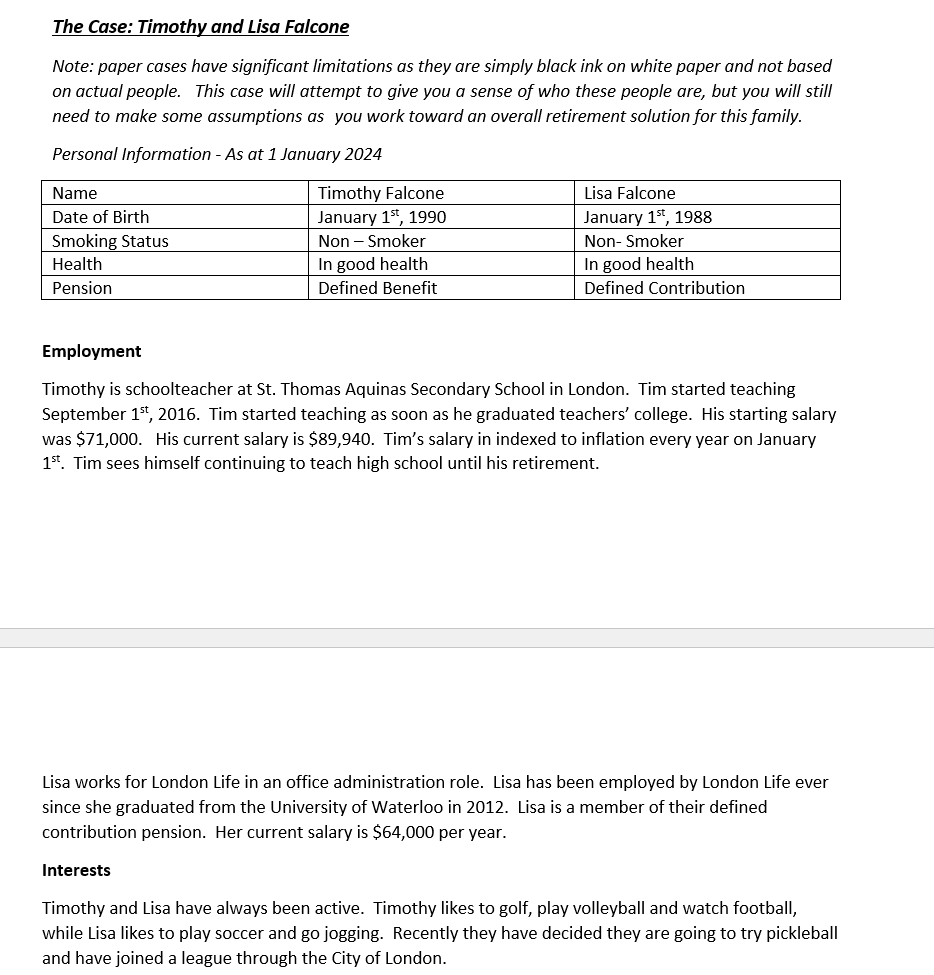

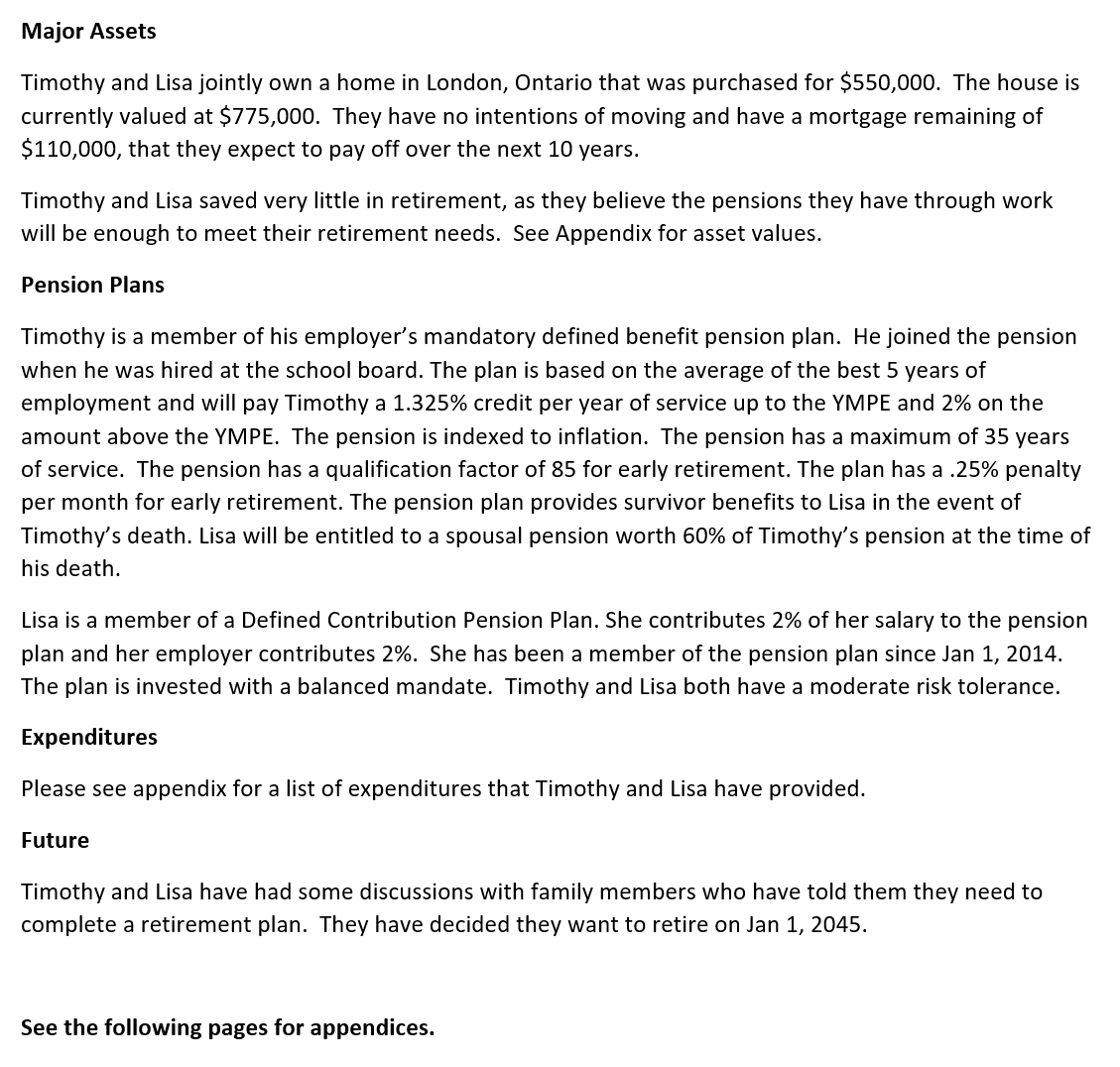

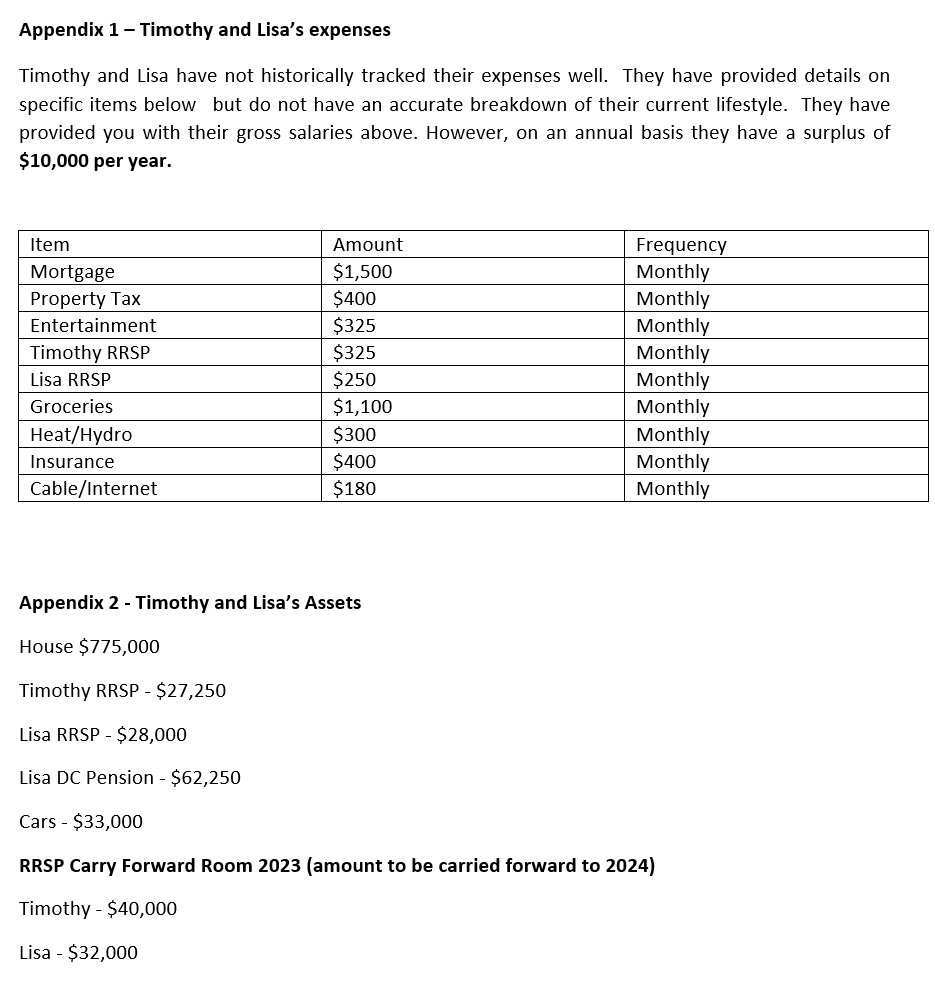

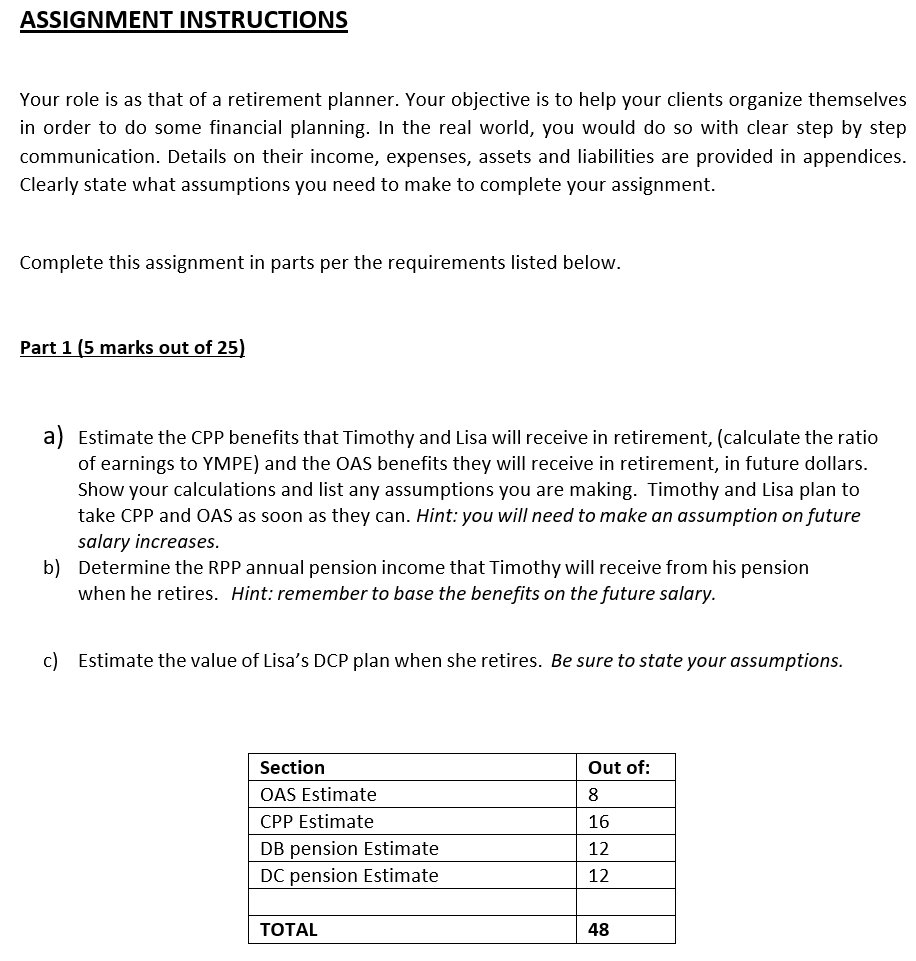

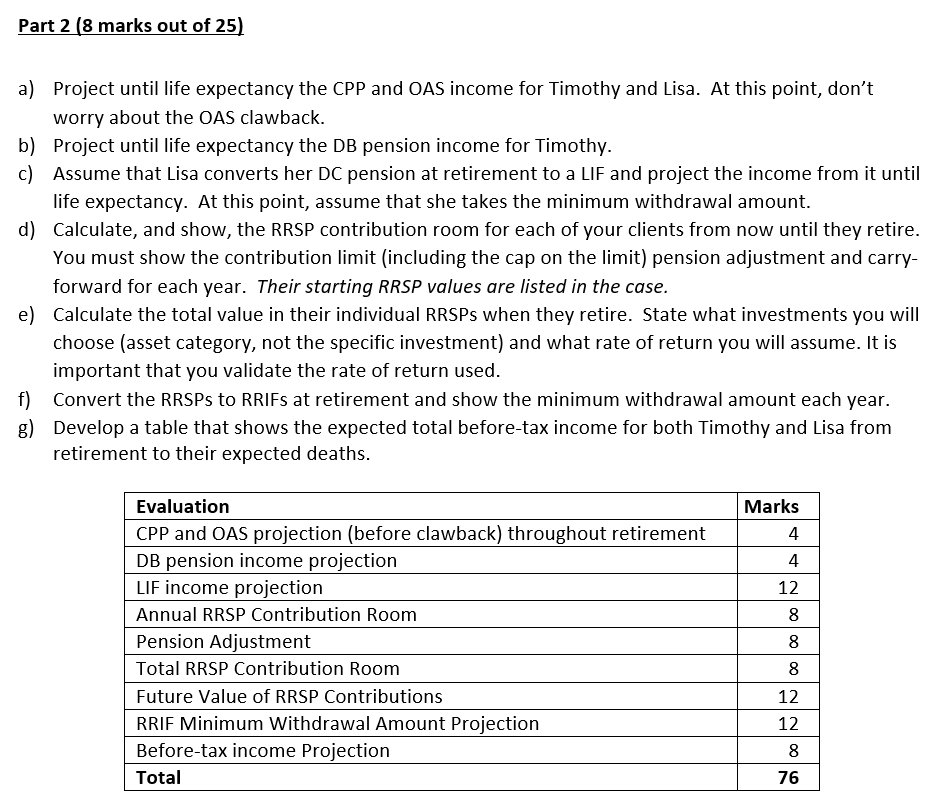

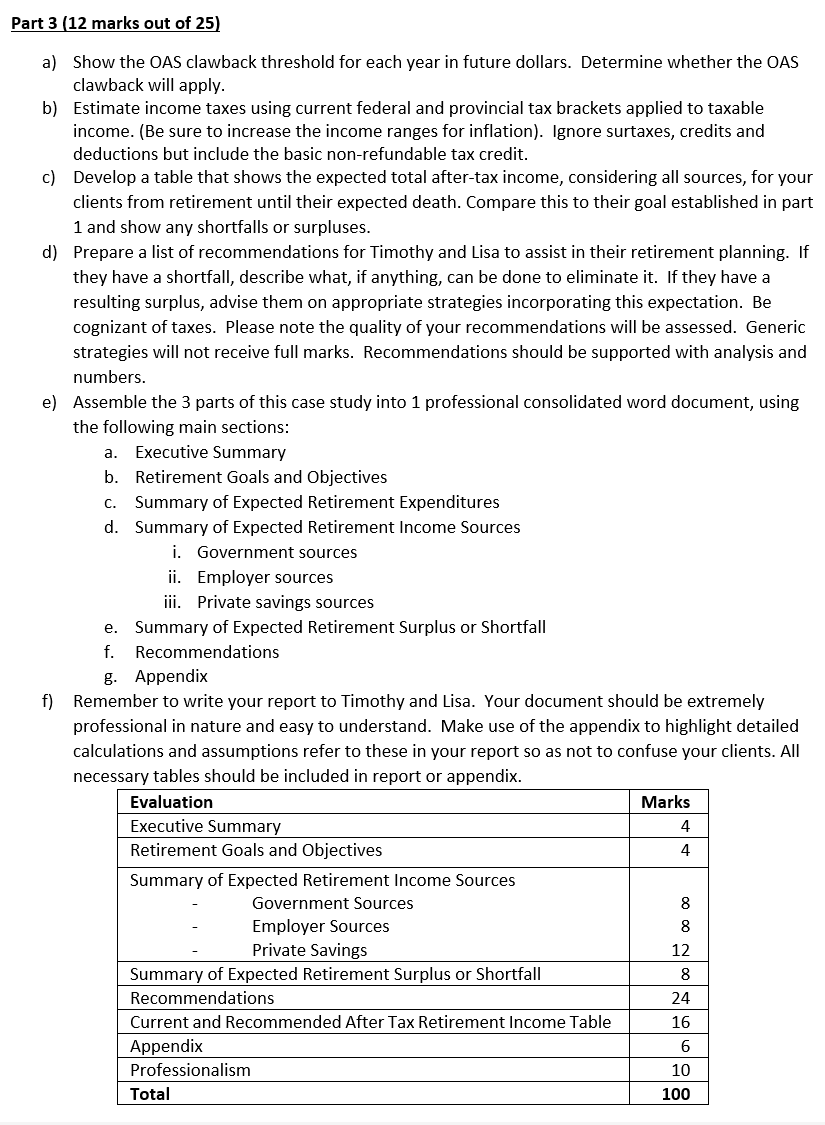

The Case: Timothy and Lisa Falcone Note: paper cases have significant limitations as they are simply black ink on white paper and not based on actual people. This case will attempt to give you a sense of who these people are, but you will still need to make some assumptions as you work toward an overall retirement solution for this family. Personal Information - As at 1 January 2024 Name Timothy Falcone Lisa Falcone Date of Birth January 1%, 1990 January 1%, 1988 Smoking Status Non Smoker Non- Smoker Health In good health In good health Pension Defined Benefit Defined Contribution Employment Timothy is schoolteacher at St. Thomas Aquinas Secondary School in London. Tim started teaching September 1%, 2016. Tim started teaching as soon as he graduated teachers' college. His starting salary was $71,000. His current salary is $89,940. Tim's salary in indexed to inflation every year on January 1%*. Tim sees himself continuing to teach high school until his retirement. Lisa works for London Life in an office administration role. Lisa has been employed by London Life ever since she graduated from the University of Waterloo in 2012. Lisa is a member of their defined contribution pension. Her current salary is $64,000 per year. Interests Timothy and Lisa have always been active. Timothy likes to golf, play volleyball and watch football, while Lisa likes to play soccer and go jogging. Recently they have decided they are going to try pickleball and have joined a league through the City of London. Major Assets Timothy and Lisa jointly own a home in London, Ontario that was purchased for $550,000. The house is currently valued at $775,000. They have no intentions of moving and have a mortgage remaining of $110,000, that they expect to pay off over the next 10 years. Timothy and Lisa saved very little in retirement, as they believe the pensions they have through work will be enough to meet their retirement needs. See Appendix for asset values. Pension Plans Timothy is a member of his employer's mandatory defined benefit pension plan. He joined the pension when he was hired at the school board. The plan is based on the average of the best 5 years of employment and will pay Timothy a 1.325% credit per year of service up to the YMPE and 2% on the amount above the YMPE. The pension is indexed to inflation. The pension has a maximum of 35 years of service. The pension has a qualification factor of 85 for early retirement. The plan has a .25% penalty per month for early retirement. The pension plan provides survivor benefits to Lisa in the event of Timothy's death. Lisa will be entitled to a spousal pension worth 60% of Timothy's pension at the time of his death. Lisa is a member of a Defined Contribution Pension Plan. She contributes 2% of her salary to the pension plan and her employer contributes 2%. She has been a member of the pension plan since Jan 1, 2014. The plan is invested with a balanced mandate. Timothy and Lisa both have a moderate risk tolerance. Expenditures Please see appendix for a list of expenditures that Timothy and Lisa have provided. Future Timothy and Lisa have had some discussions with family members who have told them they need to complete a retirement plan. They have decided they want to retire on Jan 1, 2045. See the following pages for appendices. Appendix 1 - Timothy and Lisa's expenses Timothy and Lisa have not historically tracked their expenses well. They have provided details on specific items below but do not have an accurate breakdown of their current lifestyle. They have provided you with their gross salaries above. However, on an annual basis they have a surplus of $10,000 per year. Item Amount Frequency Mortgage $1,500 Monthly Property Tax $400 Monthly Entertainment $325 Monthly Timothy RRSP $325 Monthly Lisa RRSP $250 Monthly Groceries $1,100 Monthly Heat/Hydro $300 Monthly Insurance $400 Monthly Cable/Internet $180 Monthly Appendix 2 - Timothy and Lisa's Assets House $775,000 Timothy RRSP - $27,250 Lisa RRSP - $28,000 Lisa DC Pension - $62,250 Cars - $33,000 RRSP Carry Forward Room 2023 (amount to be carried forward to 2024) Timothy - $40,000 Lisa - $32,000\fASSIGNMENT INSTRUCTIONS Your role is as that of a retirement planner. Your objective is to help your clients organize themselves in order to do some financial planning. In the real world, you would do so with clear step by step communication. Details on their income, expenses, assets and liabilities are provided in appendices. Clearly state what assumptions you need to make to complete your assignment. Complete this assignment in parts per the requirements listed below. Part 1 (5 marks out of 25) a) Estimate the CPP benefits that Timothy and Lisa will receive in retirement, (calculate the ratio of earnings to YMPE) and the OAS benefits they will receive in retirement, in future dollars. Show your calculations and list any assumptions you are making. Timothy and Lisa plan to take CPP and OAS as soon as they can. Hint: you will need to make an assumption on future salary increases. b) Determine the RPP annual pension income that Timothy will receive from his pension when he retires. Hint: remember to base the benefits on the future salary. c) Estimate the value of Lisa's DCP plan when she retires. Be sure to state your assumptions. Section OAS Estimate CPP Estimate DB pension Estimate DC pension Estimate TOTAL Part 2 (8 marks out of 25) a) Project until life expectancy the CPP and OAS income for Timothy and Lisa. At this point, don't worry about the OAS clawback. b) Project until life expectancy the DB pension income for Timothy. c) Assume that Lisa converts her DC pension at retirement to a LIF and project the income from it until life expectancy. At this point, assume that she takes the minimum withdrawal amount. d) Calculate, and show, the RRSP contribution room for each of your clients from now until they retire. You must show the contribution limit (including the cap on the limit) pension adjustment and carry- forward for each year. Their starting RRSP values are listed in the case. e) Calculate the total value in their individual RRSPs when they retire. State what investments you will choose (asset category, not the specific investment) and what rate of return you will assume. It is important that you validate the rate of return used. f) Convert the RRSPs to RRIFs at retirement and show the minimum withdrawal amount each year. g) Develop a table that shows the expected total before-tax income for both Timothy and Lisa from retirement to their expected deaths. Evaluation Marks CPP and OAS projection (before clawback) throughout retirement 4 DB pension income projection 4 LIF income projection 12 Annual RRSP Contribution Room 8 Pension Adjustment 8 Total RRSP Contribution Room 8 Future Value of RRSP Contributions 12 RRIF Minimum Withdrawal Amount Projection 12 Before-tax income Projection 8 Total 76 Part 3 (12 marks out of 25) a) b) c) d) e) f) Show the OAS clawback threshold for each year in future dollars. Determine whether the OAS clawback will apply. Estimate income taxes using current federal and provincial tax brackets applied to taxable income. (Be sure to increase the income ranges for inflation). lgnore surtaxes, credits and deductions but include the basic non-refundable tax credit. Develop a table that shows the expected total after-tax income, considering all sources, for your clients from retirement until their expected death. Compare this to their goal established in part 1 and show any shortfalls or surpluses. Prepare a list of recommendations for Timothy and Lisa to assist in their retirement planning. If they have a shortfall, describe what, if anything, can be done to eliminate it. If they have a resulting surplus, advise them on appropriate strategies incorporating this expectation. Be cognizant of taxes. Please note the quality of your recommendations will be assessed. Generic strategies will not receive full marks. Recommendations should be supported with analysis and numbers. Assemble the 3 parts of this case study into 1 professional consolidated word document, using the following main sections: a. Executive Summary b. Retirement Goals and Objectives c. Summary of Expected Retirement Expenditures d. Summary of Expected Retirement Income Sources i. Government sources ii. Employer sources iii. Private savings sources e. Summary of Expected Retirement Surplus or Shortfall f. Recommendations g. Appendix Remember to write your report to Timothy and Lisa. Your document should be extremely professional in nature and easy to understand. Make use of the appendix to highlight detailed calculations and assumptions refer to these in your report so as not to confuse your clients. All necessary tables should be included in report or appendix. Evaluation Marks Executive Summary 4 Retirement Goals and Objectives 4 Summary of Expected Retirement Income Sources - Government Sources 8 - Employer Sources 8 - Private Savings 12 8 Recommendations 24 Current and Recommended After Tax Retirement Income Table 16 Appendix 6 Professionalism 10 100

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!