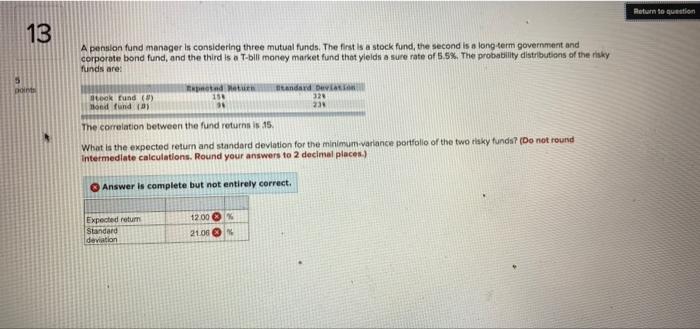

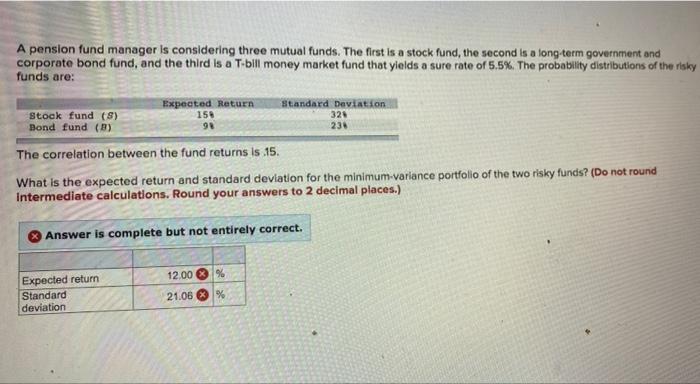

Question: Return to question 13 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government

Return to question 13 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Trond 150 tandard De 321 ook fund (3) Bond fundi The correlation between the fund returns is 15 What is the expected return and standard deviation for the minimum variance portfolio of the two risky funds? (Do not round Intermediate calculations. Round your answers to 2 decimal places) Answer is complete but not entirely correct. 1200 % Expected return andard deviation 2106 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Stock fund (8) Bond fund (3) Expected Return 159 98 Standard Deviation 325 234 The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum variance portfolio of the two risky funds? (Do not round Intermediate calculations. Round your answers to 2 decimal places.) Answer is complete but not entirely correct. 12.00 % Expected return Standard deviation 21.06

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts