Question: Return to question a. Acquired $30,000 cash from the issue of common stock. b. Purchased inventory for $18,000 cash. c. Sold inventory costing $15,000 for

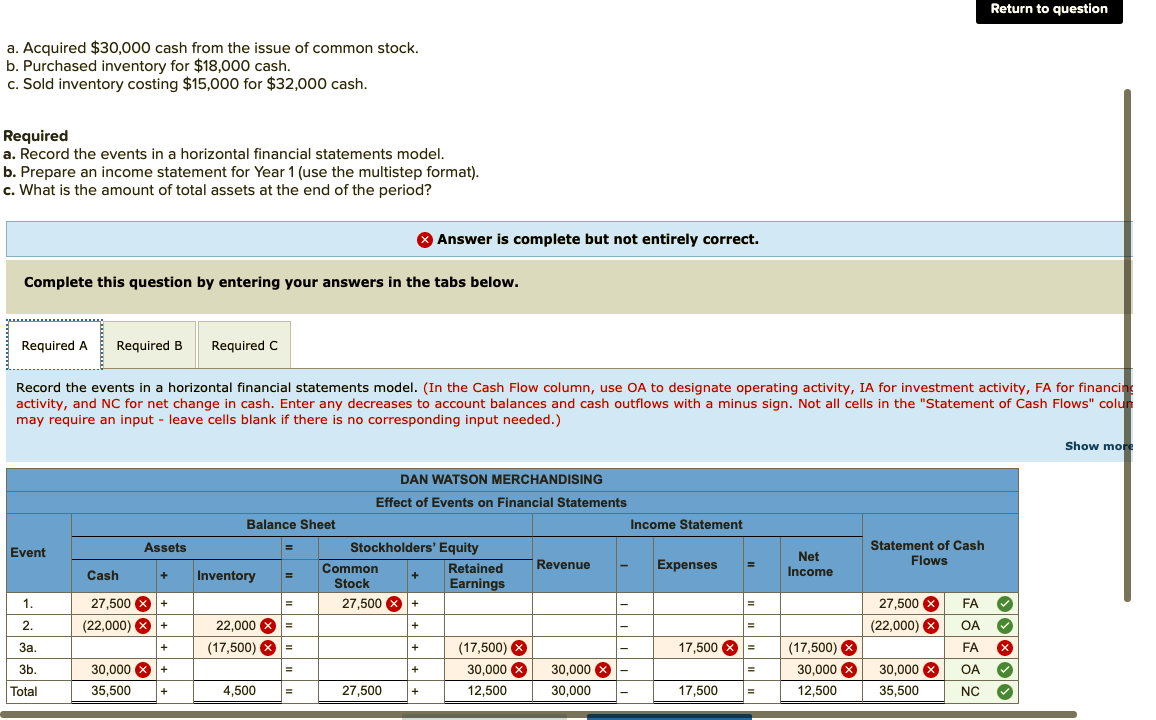

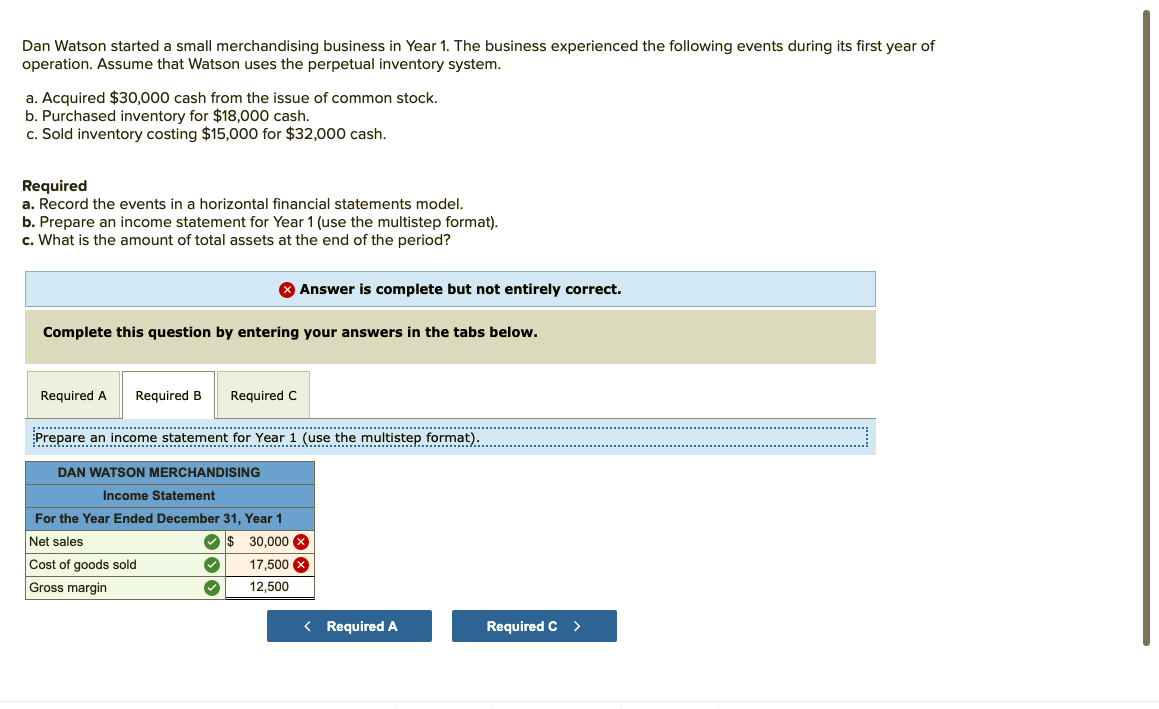

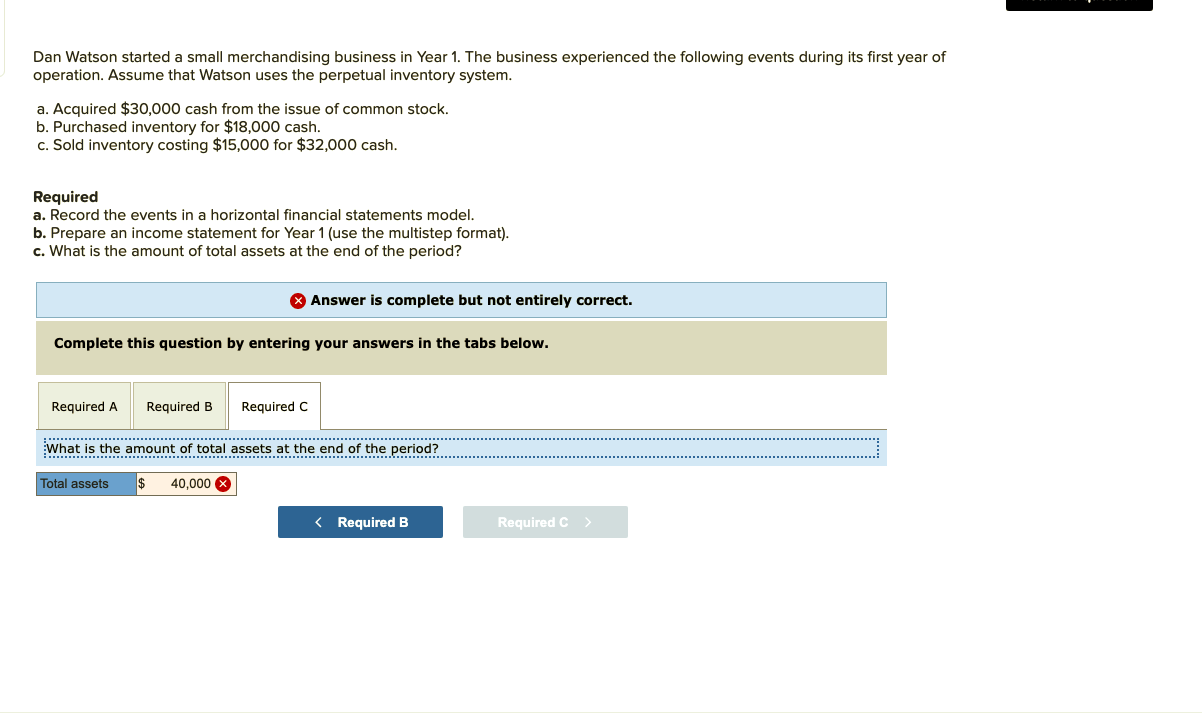

Return to question a. Acquired $30,000 cash from the issue of common stock. b. Purchased inventory for $18,000 cash. c. Sold inventory costing $15,000 for $32,000 cash. Required a. Record the events in a horizontal financial statements model. b. Prepare an income statement for Year 1 (use the multistep format). c. What is the amount of total assets at the end of the period? Answer is complete but not entirely correct. Complete this question by entering your answers in the tabs below. Required A Required B Required C Record the events in a horizontal financial statements model. (In the Cash Flow column, use OA to designate operating activity, IA for investment activity, FA for financing activity, and NC for net change in cash. Enter any decreases to account balances and cash outflows with a minus sign. Not all cells in the "Statement of Cash Flows" colur may require an input - leave cells blank if there is no corresponding input needed.) Show more Event Assets Net Income Statement of Cash Flows Cash + DAN WATSON MERCHANDISING Effect of Events on Financial Statements Balance Sheet Income Statement Stockholders' Equity Common Retained Revenue Expenses Inventory + Stock Earnings 27,500 22,000 X = (17,500) X (17,500) 17,500 X + 30,000 X 30,000 X 4,500 27,500 12,500 30,000 17,500 1. + + 27,500 X (22,000) X 27,500 FA (22,000) X OA 2. + + 3a. . + = + = FA x 3b. Total (17,500) X 30,000 X 12,500 30,000 X + 35,500 30,000 X 35,500 + + = NC Dan Watson started a small merchandising business in Year 1. The business experienced the following events during its first year of operation. Assume that Watson uses the perpetual inventory system. a. Acquired $30,000 cash from the issue of common stock. b. Purchased inventory for $18,000 cash. c. Sold inventory costing $15,000 for $32,000 cash. Required a. Record the events in a horizontal financial statements model. b. Prepare an income statement for Year 1 (use the multistep format). c. What is the amount of total assets at the end of the period? Answer is complete but not entirely correct. Complete this question by entering your answers in the tabs below. Required A Required B Required C Prepare an income statement for Year 1 (use the multistep format). DAN WATSON MERCHANDISING Income Statement For the Year Ended December 31, Year 1 Net sales $ 30,000 X Cost of goods sold 17,500 Gross margin 12,500 Dan Watson started a small merchandising business in Year 1. The business experienced the following events during its first year of operation. Assume that Watson uses the perpetual inventory system. a. Acquired $30,000 cash from the issue of common stock. b. Purchased inventory for $18,000 cash. c. Sold inventory costing $15,000 for $32,000 cash. Required a. Record the events in a horizontal financial statements model. b. Prepare an income statement for Year 1 (use the multistep format). c. What is the amount of total assets at the end of the period? Answer is complete but not entirely correct. Complete this question by entering your answers in the tabs below. Required A Required B Required C What is the amount of total assets at the end of the period? Total assets $ 40,000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts