Question: returns and risks are annualized. Problem 1 (50 points). Suppose you are interested in forming a portfolio consisting of two risky securities, securities A and

returns and risks are annualized.

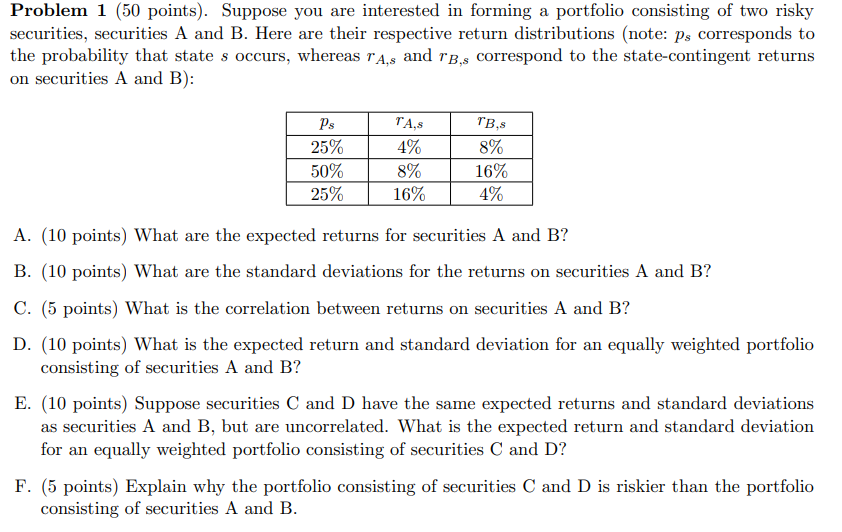

Problem 1 (50 points). Suppose you are interested in forming a portfolio consisting of two risky securities, securities A and B. Here are their respective return distributions (note: ps corresponds to the probability that state s occurs, whereas rA,s and rB,s correspond to the state-contingent returns on securities A and B): A. (10 points) What are the expected returns for securities A and B? B. (10 points) What are the standard deviations for the returns on securities A and B? C. (5 points) What is the correlation between returns on securities A and B? D. (10 points) What is the expected return and standard deviation for an equally weighted portfolio consisting of securities A and B ? E. (10 points) Suppose securities C and D have the same expected returns and standard deviations as securities A and B, but are uncorrelated. What is the expected return and standard deviation for an equally weighted portfolio consisting of securities C and D ? F. (5 points) Explain why the portfolio consisting of securities C and D is riskier than the portfolio consisting of securities A and B

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts