Q4. Review the accounts receivable lead sheet memo and related workpapers (AR.3.1 to AR.3.4). Evaluate the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

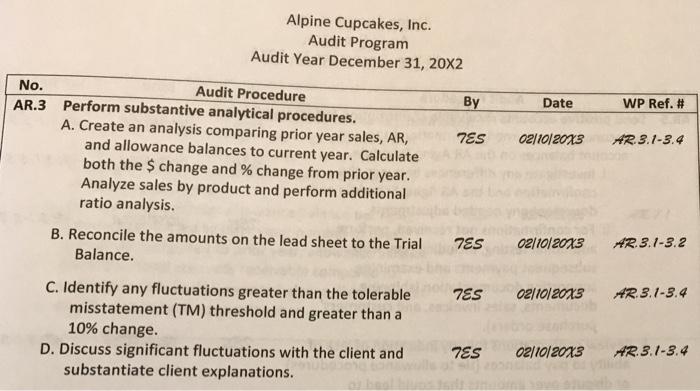

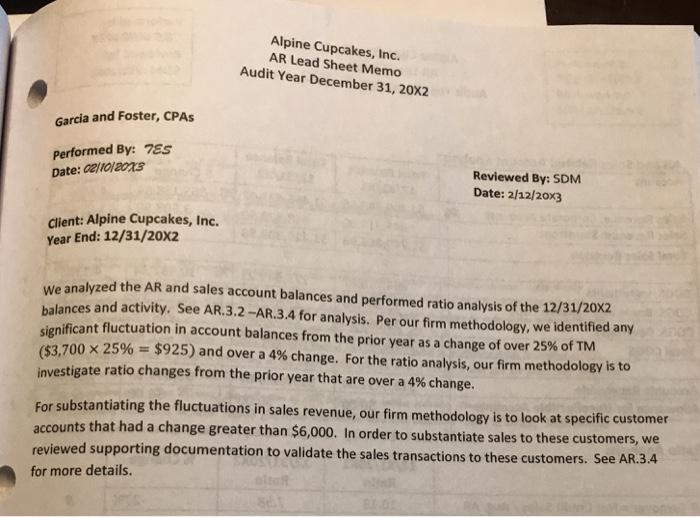

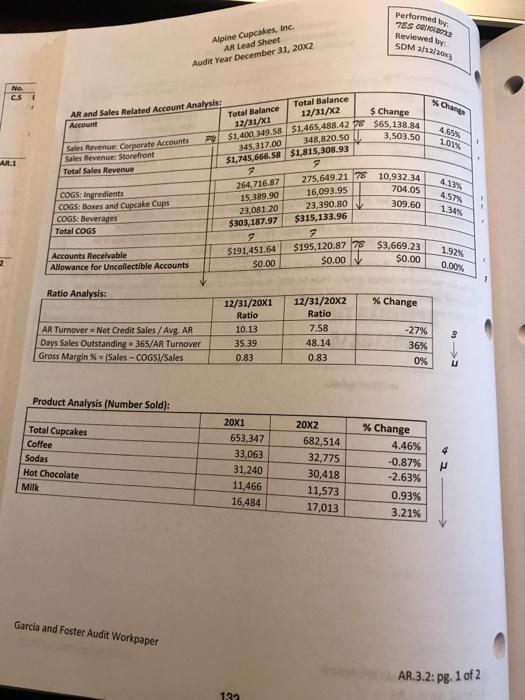

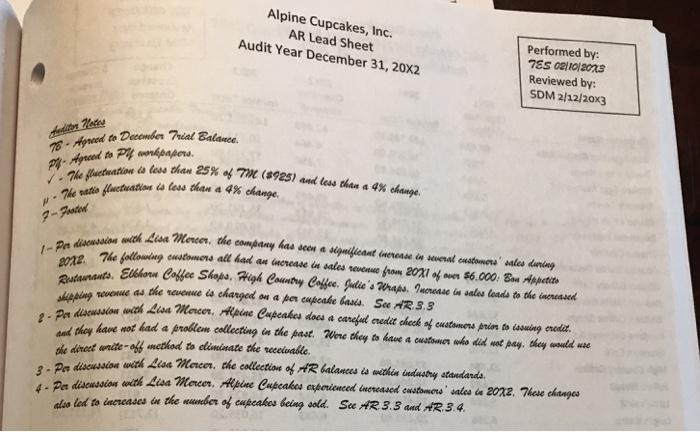

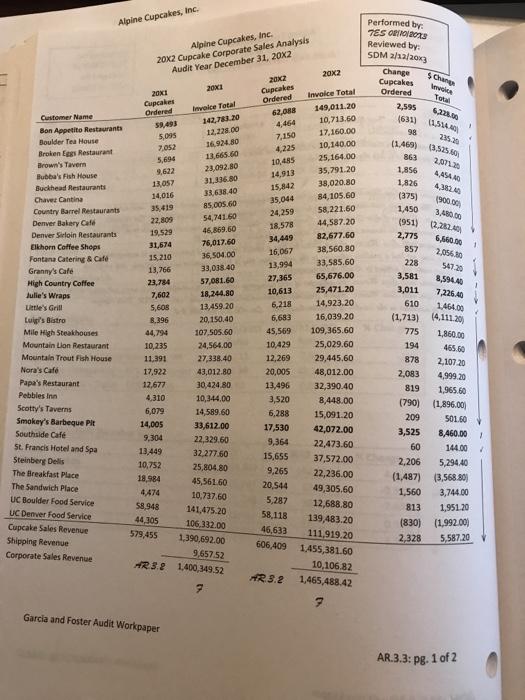

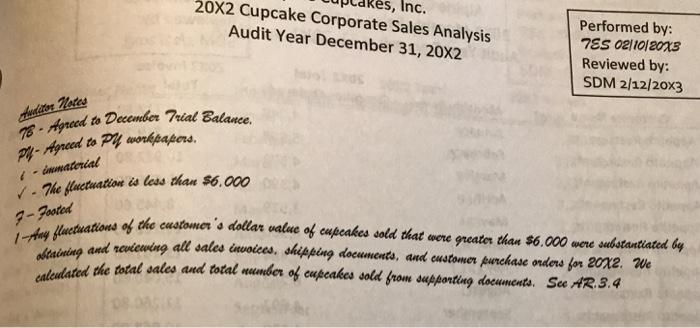

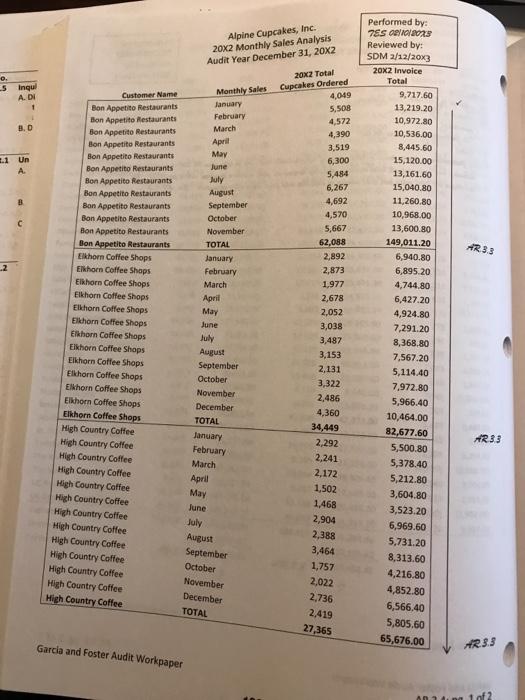

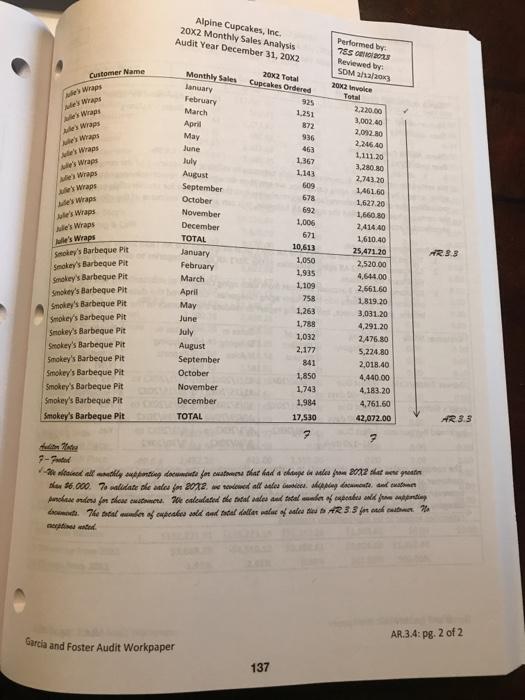

Q4. Review the accounts receivable lead sheet memo and related workpapers (AR.3.1 to AR.3.4). Evaluate the auditors' tickmarks, comments, and explanations in the memo and on the lead sheet. Identify any of the following issues: a. Did they perform all of the steps associated with the AR.3 audit procedure? b. Did they perform the steps accurately? If not, specifically state the nature of the problem and follow up on it to the extent possible with the information given. c. Do you see any other issues or problems with the auditors' work or client documentation? This question relates to Step 4 of the Garcia and Foster Audit Plan. Alpine Cupcakes, Inc. Audit Program Audit Year December 31, 20X2 No. Audit Procedure AR.3 Perform substantive analytical procedures. A. Create an analysis comparing prior year sales, AR, and allowance balances to current year. Calculate both the $ change and % change from prior year. Analyze sales by product and perform additional ratio analysis. B. Reconcile the amounts on the lead sheet to the Trial Balance. C. Identify any fluctuations greater than the tolerable misstatement (TM) threshold and greater than a 10% change. D. Discuss significant fluctuations with the client and substantiate client explanations. By 7ES TES Date TES 02/10/20x3 02/10/20x3 7ES 02/10/2013 02/10/20x3 WP Ref. # AR.3.1-3.4 AR.3.1-3.2 AR.3.1-3.4 AR.3.1-3.4 Garcia and Foster, CPAS Performed By: 7Es Date: 02/10/2013 Client: Alpine Cupcakes, Inc. Year End: 12/31/20X2 Alpine Cupcakes, Inc. AR Lead Sheet Memo Audit Year December 31, 20X2 Reviewed By: SDM Date: 2/12/20x3 We analyzed the AR and sales account balances and performed ratio analysis of the 12/31/20X2 balances and activity. See AR.3.2-AR.3.4 for analysis. Per our firm methodology, we identified any significant fluctuation in account balances from the prior year as a change of over 25% of TM ($3,700 x 25% = $925) and over a 4% change. For the ratio analysis, our firm methodology is to investigate ratio changes from the prior year that are over a 4% change. For substantiating the fluctuations in sales revenue, our firm methodology is to look at specific customer accounts that had a change greater than $6,000. In order to substantiate sales to these customers, we reviewed supporting documentation to validate the sales transactions to these customers. See AR.3.4 for more details. No. C.5 AR.1 AR and Sales Related Account Analysis: Account Sales Revenue: Corporate Accounts Sales Revenue: Storefront Total Sales Revenue COGS: Ingredients COGS: Boxes and Cupcake Cups COGS: Beverages Total COGS Accounts Receivable Allowance for Uncollectible Accounts Ratio Analysis: Alpine Cupcakes, Inc. AR Lead Sheet Audit Year December 31, 20X2 AR Turnover Net Credit Sales/Avg. AR Days Sales Outstanding 365/AR Turnover Gross Margin %-(Sales-COGS)/Sales Product Analysis (Number Sold): Total Cupcakes Coffee Sodas Hot Chocolate Milk Garcia and Foster Audit Workpaper $ Change Total Balance 12/31/X1 P $1,400,349.58 $1,465,488.42 8 $65,138.84 3,503.50 345,317.00 348,820.50 $1,745,666.58 $1,815,308.93 7 7 264,716.87 15,389.90 23,081.20 $303,187.97 9 $191,451.64 $0.00 12/31/20X1 Ratio 10.13 35.39 0.83 20X1 Total Balance 12/31/X2 653,347 33,063 31,240 11,466 16,484 132 275,649.21 76 10,932.34 16,093.95 704.05 23,390.80 309.60 $315,133.96 7 $195,120.87 78 $3,669.23 $0.00 V $0.00 12/31/20X2 Ratio 7.58 Performed by: 755 02/10/2013 Reviewed by: SDM 2/12/20x3 48.14 0.83 20X2 682,514 32,775 30,418 11,573 17,013 % Change % Change 4.46% -0.87% -2.63% % Change 0.93% 3.21% 4.65% 1.01% 4.13% 4.57% -27% 3 36% 0% 1.34% 1.92% 0.00% C16 AR.3.2: pg. 1 of 2 Alpine Cupcakes, Inc. AR Lead Sheet Audit Year December 31, 20X2 Auditor Notes 76-Agreed to December Trial Balance. P-Agreed to P workpapers. -The fluctuation is less than 25% of 7M ($925) and less than a 4% change. The ratio fluctuation is less than a 4% change. #- 7-Fosted Performed by: 785 02/10/2013 Reviewed by: SDM 2/12/20x3 1-Per discussion with Lisa Mercer, the company has seen a significant increase in several customers' sales during 2022. The following customers all had an increase in sales revenue from 2001 of over $6.000: Bon Appetito Restaurants. Elkhorn Coffee Shops. High Country Coffee. Julie's Wraps. Increase in sales leads to the increased shipping revenue as the revenue is charged on a per cupcake basis. See AR. 3.3 2- Por discussion with Lisa Morcer. Alpine Cupcakes does a careful credit check of customers prior to issuing credit. and they have not had a problem collecting in the past. Were they to have a customer who did not pay, they would use the direct write-off method to eliminate the receivable. 3- Per discussion with Lisa Morcer, the collection of AR balances is within industry standards. 4- Per discussion with Lisa Morcer. Alpine Cupcakes experienced increased customers' sales in 2012. These changes also led to increases in the number of cupcakes being sold. See AR.3.3 and AR.3.4. Customer Name Bon Appetito Restaurants Boulder Tea House Broken Eggs Restaurant Brown's Tavern Bubba's Fish House Buckhead Restaurants Chavez Cantina Country Barrel Restaurants Denver Bakery Café Denver Sirloin Restaurants Elkhorn Coffee Shops Fontana Catering & Café Granny's Café High Country Coffee Julie's Wraps Little's Grill Luigi's Bistro Mile High Steakhouses Mountain Lion Restaurant Mountain Trout Fish House Nora's Café Papa's Restaurant Pebbles Inn Scotty's Taverns Smokey's Barbeque Pit Southside Café St. Francis Hotel and Spa Steinberg Delis Alpine Cupcakes, Inc. The Breakfast Place The Sandwich Place UC Boulder Food Service UC Denver Food Service Cupcake Sales Revenue Shipping Revenue Corporate Sales Revenue Alpine Cupcakes, Inc. 20x2 Cupcake Corporate Sales Analysis Audit Year December 31, 20x2 2001 Cupcakes Ordered 59,493 5,095 7,052 5,694 9,622 13,057 14.016 35,419 22,809 19,529 31,674 15,210 13,766 23,784 7,602 5,608 8.396 44,794 10,235 11,391 17,922 12,677 4,310 6,079 14,005 9,304 13,449 10,752 18,984 4,474 58,948 44,305 579,455 2001 Invoice Total 142,783.20 12,228.00 16.924.80 13,665.60 Garcia and Foster Audit Workpaper 23,092.80 31,336.80 33,638.40 85,005.60 54,741.60 46,869.60 76,017.60 36,504.00 33,038.40 57,081.60 18,244.80 13,459.20 14,589.60 33,612.00 22,329.60 32,277.60 25,804.80 45,561.60 10,737.60 141,475.20 106,332.00 1,390,692.00 9,657.52 AR3.2 1,400,349.52 7 20,150.40 107,505.60 24,564.00 27,338.40 43,012.80 30,424.80 10,344.00 2012 Cupcakes Ordered 62,088 4,464 7,150 4,225 10,485 14,913 15,842 35,044 24,259 18,578 34,449 12,269 20,005 13,496 3,520 6,288 20x2 Invoice Total 149,011.20 10,713.60 17,160.00 10,140.00 25,164.00 16,067 13,994 27,365 10,613 6,218 6,683 45,569 109,365.60 10,429 25,029.60 29,445.60 48,012.00 32,390.40 8,448.00 AR. 3.2 35,791.20 38,020.80 84,105.60 58,221.60 44,587.20 82,677.60 38,560.80 33,585.60 65,676.00 25,471.20 14,923.20 16,039.20 15,091.20 42,072.00 22,473.60 37,572.00 22,236.00 49,305.60 12,688.80 17,530 9,364 15,655 9,265 20,544 5,287 58,118 139,483.20 46.633 111,919.20 606,409 1,455,381.60 10,106.82 1,465,488.42 7 Performed by: TES 08/10/2013 Reviewed by: SDM 2/12/20x3 Change Cupcakes Ordered $ Change Invoice Total 2,595 (631) 98 235.20 (1,469) (3.525.60) 863 2,071.20 4,454.40 6,228.00 (1,514.40) 1,856 1,826 (375) (900.00) 1,450 3,480.00 (951) (2,282.40) 2,775 6,660.00 857 2,056.80 228 3,581 3,011 610 4,382,40 547.20 8,594.40 7,226.40 1,464.00 (1,713) (4,111.20) 775 194 878 2,083 819 1,860.00 465.60 2,107.20 4,999.20 1,965.60 (790) (1,896.00) 209 501.60 3,525 8,460.00 60 V 1 144.00 7 5,294.40 2,206 (1,487) (3,568.80) 1,560 3,744.00 813 1,951.20 (830) (1,992.00) 2,328 5,587.20 1 AR.3.3: pg. 1 of 2 Inc. 20X2 Cupcake Corporate Sales Analysis Audit Year December 31, 20X2 Performed by: 7ES 02/10/20x3 Reviewed by: SDM 2/12/20x3 Auditor Notes 76-Agreed to December Trial Balance. P-Agreed to Py workpapers. immaterial ✓ The fluctuation is less than $6.000 7-Footed 1-Any fluctuations of the customer's dollar value of cupcakes sold that were greater than $6.000 were substantiated by obtaining and reviewing all sales invoices, shipping documents, and customer purchase orders for 20X2. We calculated the total sales and total number of cupcakes sold from supporting documents. See AR.3.4 08 0. 5 Inqui A. DI 2 B.D 1 Un A. Customer Name Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee Alpine Cupcakes, Inc. 20x2 Monthly Sales Analysis Audit Year December 31, 20X2 Garcia and Foster Audit Workpaper Monthly Sales January February March April May June July August September October November TOTAL January February March April May June July August September October November December TOTAL January February March April May June July August September October November December TOTAL 20x2 Total Cupcakes Ordered 4,049 5,508 4,572 4,390 3,519 6,300 5,484 6,267 4,692 4,570 5,667 62,088 2,892 2,873 1,977 2,678 2,052 3,038 3,487 3,153 2,131 3,322 2,486 4,360 34,449 2,292 2,241 2,172 1,502 1,468 2,904 2,388 3,464 1,757 2,022 2,736 2,419 27,365 Performed by: 7ES 02/10/202 Reviewed by: SDM 2/12/20x3 20X2 Invoice Total 9,717.60 13,219.20 10,972.80 10,536.00 8,445.60 15,120.00 13,161.60 15,040.80 11,260.80 10,968.00 13,600.80 149,011.20 6,940.80 6,895.20 4,744.80 6,427.20 4,924.80 7,291.20 8,368.80 7,567.20 5,114.40 7,972.80 5,966.40 10,464.00 82,677.60 5,500.80 5,378.40 5,212.80 3,604.80 3,523.20 6,969.60 5,731.20 8,313.60 4,216.80 4,852.80 6,566.40 5,805.60 65,676.00 AR 3.3 AR33 AR3.3 1of2 Customer Name le's Wraps Ale's Wraps le's Wraps Ale's Wraps le's Wraps Wraps Julie's e's Wraps le's Wraps Julle's Wraps le's Wraps Jule's Wraps le's Wraps Alle's Wraps Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Alpine Cupcakes, Inc. 20x2 Monthly Sales Analysis Audit Year December 31, 20X2 Garcia and Foster Audit Workpaper Monthly Sales January February March April May June July August September October November December TOTAL January February March April May June July August September October November December TOTAL 2002 Total Cupcakes Ordered 925 1,251 137 872 936 463 1,367 1,143 609 678 692 1,006 671 10,613 1,050 1,935 1,109 758 1,263 1,788 1,032 2,177 841 1,850 1,743 1,984 17,530 7 Performed by: 785 233 Reviewed by: SDM 2/12/2003 2012 Invoice Total 2,220.00 3,002,40 2,092.80 2,246.40 1,111.20 3,280.80 2,743.20 1,461.60 1,627.20 1,660.80 2,414.40 1,610.40 25,471.20 2,520.00 4,644.00 2,661.60 1,819.20 3,031.20 4,291.20 2,476.80 5,224.80 2,018.40 4,440.00 4,183.20 4,761.60 42,072.00 Audition Notes 7-Frated We desired all monthly supporting documents for customers that had a change in sales from 20X2 that were greater than $6.000. To validate the sales for 20X2, we reviewed all sales invoices, shipping documents, and customer purchase orders for these customers. We calculated the total sales and total number of empeabes sold from supporting documents. The total number of cupcakes sold and total dollar value of sales ties to AR 3.3 for each customer. No aceptis unted. ARS.3 AR.3.3 AR.3.4: pg. 2 of 2 Q4. Review the accounts receivable lead sheet memo and related workpapers (AR.3.1 to AR.3.4). Evaluate the auditors' tickmarks, comments, and explanations in the memo and on the lead sheet. Identify any of the following issues: a. Did they perform all of the steps associated with the AR.3 audit procedure? b. Did they perform the steps accurately? If not, specifically state the nature of the problem and follow up on it to the extent possible with the information given. c. Do you see any other issues or problems with the auditors' work or client documentation? This question relates to Step 4 of the Garcia and Foster Audit Plan. Alpine Cupcakes, Inc. Audit Program Audit Year December 31, 20X2 No. Audit Procedure AR.3 Perform substantive analytical procedures. A. Create an analysis comparing prior year sales, AR, and allowance balances to current year. Calculate both the $ change and % change from prior year. Analyze sales by product and perform additional ratio analysis. B. Reconcile the amounts on the lead sheet to the Trial Balance. C. Identify any fluctuations greater than the tolerable misstatement (TM) threshold and greater than a 10% change. D. Discuss significant fluctuations with the client and substantiate client explanations. By 7ES TES Date TES 02/10/20x3 02/10/20x3 7ES 02/10/2013 02/10/20x3 WP Ref. # AR.3.1-3.4 AR.3.1-3.2 AR.3.1-3.4 AR.3.1-3.4 Garcia and Foster, CPAS Performed By: 7Es Date: 02/10/2013 Client: Alpine Cupcakes, Inc. Year End: 12/31/20X2 Alpine Cupcakes, Inc. AR Lead Sheet Memo Audit Year December 31, 20X2 Reviewed By: SDM Date: 2/12/20x3 We analyzed the AR and sales account balances and performed ratio analysis of the 12/31/20X2 balances and activity. See AR.3.2-AR.3.4 for analysis. Per our firm methodology, we identified any significant fluctuation in account balances from the prior year as a change of over 25% of TM ($3,700 x 25% = $925) and over a 4% change. For the ratio analysis, our firm methodology is to investigate ratio changes from the prior year that are over a 4% change. For substantiating the fluctuations in sales revenue, our firm methodology is to look at specific customer accounts that had a change greater than $6,000. In order to substantiate sales to these customers, we reviewed supporting documentation to validate the sales transactions to these customers. See AR.3.4 for more details. No. C.5 AR.1 AR and Sales Related Account Analysis: Account Sales Revenue: Corporate Accounts Sales Revenue: Storefront Total Sales Revenue COGS: Ingredients COGS: Boxes and Cupcake Cups COGS: Beverages Total COGS Accounts Receivable Allowance for Uncollectible Accounts Ratio Analysis: Alpine Cupcakes, Inc. AR Lead Sheet Audit Year December 31, 20X2 AR Turnover Net Credit Sales/Avg. AR Days Sales Outstanding 365/AR Turnover Gross Margin %-(Sales-COGS)/Sales Product Analysis (Number Sold): Total Cupcakes Coffee Sodas Hot Chocolate Milk Garcia and Foster Audit Workpaper $ Change Total Balance 12/31/X1 P $1,400,349.58 $1,465,488.42 8 $65,138.84 3,503.50 345,317.00 348,820.50 $1,745,666.58 $1,815,308.93 7 7 264,716.87 15,389.90 23,081.20 $303,187.97 9 $191,451.64 $0.00 12/31/20X1 Ratio 10.13 35.39 0.83 20X1 Total Balance 12/31/X2 653,347 33,063 31,240 11,466 16,484 132 275,649.21 76 10,932.34 16,093.95 704.05 23,390.80 309.60 $315,133.96 7 $195,120.87 78 $3,669.23 $0.00 V $0.00 12/31/20X2 Ratio 7.58 Performed by: 755 02/10/2013 Reviewed by: SDM 2/12/20x3 48.14 0.83 20X2 682,514 32,775 30,418 11,573 17,013 % Change % Change 4.46% -0.87% -2.63% % Change 0.93% 3.21% 4.65% 1.01% 4.13% 4.57% -27% 3 36% 0% 1.34% 1.92% 0.00% C16 AR.3.2: pg. 1 of 2 Alpine Cupcakes, Inc. AR Lead Sheet Audit Year December 31, 20X2 Auditor Notes 76-Agreed to December Trial Balance. P-Agreed to P workpapers. -The fluctuation is less than 25% of 7M ($925) and less than a 4% change. The ratio fluctuation is less than a 4% change. #- 7-Fosted Performed by: 785 02/10/2013 Reviewed by: SDM 2/12/20x3 1-Per discussion with Lisa Mercer, the company has seen a significant increase in several customers' sales during 2022. The following customers all had an increase in sales revenue from 2001 of over $6.000: Bon Appetito Restaurants. Elkhorn Coffee Shops. High Country Coffee. Julie's Wraps. Increase in sales leads to the increased shipping revenue as the revenue is charged on a per cupcake basis. See AR. 3.3 2- Por discussion with Lisa Morcer. Alpine Cupcakes does a careful credit check of customers prior to issuing credit. and they have not had a problem collecting in the past. Were they to have a customer who did not pay, they would use the direct write-off method to eliminate the receivable. 3- Per discussion with Lisa Morcer, the collection of AR balances is within industry standards. 4- Per discussion with Lisa Morcer. Alpine Cupcakes experienced increased customers' sales in 2012. These changes also led to increases in the number of cupcakes being sold. See AR.3.3 and AR.3.4. Customer Name Bon Appetito Restaurants Boulder Tea House Broken Eggs Restaurant Brown's Tavern Bubba's Fish House Buckhead Restaurants Chavez Cantina Country Barrel Restaurants Denver Bakery Café Denver Sirloin Restaurants Elkhorn Coffee Shops Fontana Catering & Café Granny's Café High Country Coffee Julie's Wraps Little's Grill Luigi's Bistro Mile High Steakhouses Mountain Lion Restaurant Mountain Trout Fish House Nora's Café Papa's Restaurant Pebbles Inn Scotty's Taverns Smokey's Barbeque Pit Southside Café St. Francis Hotel and Spa Steinberg Delis Alpine Cupcakes, Inc. The Breakfast Place The Sandwich Place UC Boulder Food Service UC Denver Food Service Cupcake Sales Revenue Shipping Revenue Corporate Sales Revenue Alpine Cupcakes, Inc. 20x2 Cupcake Corporate Sales Analysis Audit Year December 31, 20x2 2001 Cupcakes Ordered 59,493 5,095 7,052 5,694 9,622 13,057 14.016 35,419 22,809 19,529 31,674 15,210 13,766 23,784 7,602 5,608 8.396 44,794 10,235 11,391 17,922 12,677 4,310 6,079 14,005 9,304 13,449 10,752 18,984 4,474 58,948 44,305 579,455 2001 Invoice Total 142,783.20 12,228.00 16.924.80 13,665.60 Garcia and Foster Audit Workpaper 23,092.80 31,336.80 33,638.40 85,005.60 54,741.60 46,869.60 76,017.60 36,504.00 33,038.40 57,081.60 18,244.80 13,459.20 14,589.60 33,612.00 22,329.60 32,277.60 25,804.80 45,561.60 10,737.60 141,475.20 106,332.00 1,390,692.00 9,657.52 AR3.2 1,400,349.52 7 20,150.40 107,505.60 24,564.00 27,338.40 43,012.80 30,424.80 10,344.00 2012 Cupcakes Ordered 62,088 4,464 7,150 4,225 10,485 14,913 15,842 35,044 24,259 18,578 34,449 12,269 20,005 13,496 3,520 6,288 20x2 Invoice Total 149,011.20 10,713.60 17,160.00 10,140.00 25,164.00 16,067 13,994 27,365 10,613 6,218 6,683 45,569 109,365.60 10,429 25,029.60 29,445.60 48,012.00 32,390.40 8,448.00 AR. 3.2 35,791.20 38,020.80 84,105.60 58,221.60 44,587.20 82,677.60 38,560.80 33,585.60 65,676.00 25,471.20 14,923.20 16,039.20 15,091.20 42,072.00 22,473.60 37,572.00 22,236.00 49,305.60 12,688.80 17,530 9,364 15,655 9,265 20,544 5,287 58,118 139,483.20 46.633 111,919.20 606,409 1,455,381.60 10,106.82 1,465,488.42 7 Performed by: TES 08/10/2013 Reviewed by: SDM 2/12/20x3 Change Cupcakes Ordered $ Change Invoice Total 2,595 (631) 98 235.20 (1,469) (3.525.60) 863 2,071.20 4,454.40 6,228.00 (1,514.40) 1,856 1,826 (375) (900.00) 1,450 3,480.00 (951) (2,282.40) 2,775 6,660.00 857 2,056.80 228 3,581 3,011 610 4,382,40 547.20 8,594.40 7,226.40 1,464.00 (1,713) (4,111.20) 775 194 878 2,083 819 1,860.00 465.60 2,107.20 4,999.20 1,965.60 (790) (1,896.00) 209 501.60 3,525 8,460.00 60 V 1 144.00 7 5,294.40 2,206 (1,487) (3,568.80) 1,560 3,744.00 813 1,951.20 (830) (1,992.00) 2,328 5,587.20 1 AR.3.3: pg. 1 of 2 Inc. 20X2 Cupcake Corporate Sales Analysis Audit Year December 31, 20X2 Performed by: 7ES 02/10/20x3 Reviewed by: SDM 2/12/20x3 Auditor Notes 76-Agreed to December Trial Balance. P-Agreed to Py workpapers. immaterial ✓ The fluctuation is less than $6.000 7-Footed 1-Any fluctuations of the customer's dollar value of cupcakes sold that were greater than $6.000 were substantiated by obtaining and reviewing all sales invoices, shipping documents, and customer purchase orders for 20X2. We calculated the total sales and total number of cupcakes sold from supporting documents. See AR.3.4 08 0. 5 Inqui A. DI 2 B.D 1 Un A. Customer Name Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Bon Appetito Restaurants Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops Elkhorn Coffee Shops High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee High Country Coffee Alpine Cupcakes, Inc. 20x2 Monthly Sales Analysis Audit Year December 31, 20X2 Garcia and Foster Audit Workpaper Monthly Sales January February March April May June July August September October November TOTAL January February March April May June July August September October November December TOTAL January February March April May June July August September October November December TOTAL 20x2 Total Cupcakes Ordered 4,049 5,508 4,572 4,390 3,519 6,300 5,484 6,267 4,692 4,570 5,667 62,088 2,892 2,873 1,977 2,678 2,052 3,038 3,487 3,153 2,131 3,322 2,486 4,360 34,449 2,292 2,241 2,172 1,502 1,468 2,904 2,388 3,464 1,757 2,022 2,736 2,419 27,365 Performed by: 7ES 02/10/202 Reviewed by: SDM 2/12/20x3 20X2 Invoice Total 9,717.60 13,219.20 10,972.80 10,536.00 8,445.60 15,120.00 13,161.60 15,040.80 11,260.80 10,968.00 13,600.80 149,011.20 6,940.80 6,895.20 4,744.80 6,427.20 4,924.80 7,291.20 8,368.80 7,567.20 5,114.40 7,972.80 5,966.40 10,464.00 82,677.60 5,500.80 5,378.40 5,212.80 3,604.80 3,523.20 6,969.60 5,731.20 8,313.60 4,216.80 4,852.80 6,566.40 5,805.60 65,676.00 AR 3.3 AR33 AR3.3 1of2 Customer Name le's Wraps Ale's Wraps le's Wraps Ale's Wraps le's Wraps Wraps Julie's e's Wraps le's Wraps Julle's Wraps le's Wraps Jule's Wraps le's Wraps Alle's Wraps Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Smokey's Barbeque Pit Alpine Cupcakes, Inc. 20x2 Monthly Sales Analysis Audit Year December 31, 20X2 Garcia and Foster Audit Workpaper Monthly Sales January February March April May June July August September October November December TOTAL January February March April May June July August September October November December TOTAL 2002 Total Cupcakes Ordered 925 1,251 137 872 936 463 1,367 1,143 609 678 692 1,006 671 10,613 1,050 1,935 1,109 758 1,263 1,788 1,032 2,177 841 1,850 1,743 1,984 17,530 7 Performed by: 785 233 Reviewed by: SDM 2/12/2003 2012 Invoice Total 2,220.00 3,002,40 2,092.80 2,246.40 1,111.20 3,280.80 2,743.20 1,461.60 1,627.20 1,660.80 2,414.40 1,610.40 25,471.20 2,520.00 4,644.00 2,661.60 1,819.20 3,031.20 4,291.20 2,476.80 5,224.80 2,018.40 4,440.00 4,183.20 4,761.60 42,072.00 Audition Notes 7-Frated We desired all monthly supporting documents for customers that had a change in sales from 20X2 that were greater than $6.000. To validate the sales for 20X2, we reviewed all sales invoices, shipping documents, and customer purchase orders for these customers. We calculated the total sales and total number of empeabes sold from supporting documents. The total number of cupcakes sold and total dollar value of sales ties to AR 3.3 for each customer. No aceptis unted. ARS.3 AR.3.3 AR.3.4: pg. 2 of 2

Expert Answer:

Related Book For

Intermediate Accounting IFRS

ISBN: 978-1119372936

3rd edition

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield

Posted Date:

Students also viewed these accounting questions

-

1. Read the accounts receivable narrative (AR.1.1) and review the sales and accounts receivable flowchart (AR.1.2). Review the narrative and flowchart to identify all of the internal control...

-

Auditors develop overall audit plans to ensure that they obtain sufficient appropriate audit evidence. The timing and extent of audit procedures auditors use is a matter of professional judgment,...

-

Information related to accounts receivable is given for two cases: Case 1 Technology Solutions uses the credit sales method to estimate bad debt expense. Sales this year were $ 5,600,000, of which...

-

The following is a summary of the petty cash transactions of Jockfield Ltd for May 2012. You are required to: (a) Rule up a suitable petty cash book with analysis columns for expenditure on cleaning,...

-

Discuss the concept of steps into the shoes. Does this concept pertain to the partnership, the partners, or both?

-

The power spectral density of a random process X (t) is shown in Figure. It contains of a delta function at f = 0 and a triangular component. (a) Determine and sketch the autocorrelation function RX...

-

Plaintiff purchases a new car that has defects in its paint job. Three times the dealership repaints the care, but to no avail. The plaintiff continues to drive the car as he has no other option in...

-

Sanchez Corporation is considering three long-term capital investment proposals. Relevant data on each project are as follows. Salvage value is expected to be zero at the end of each project....

-

Calculate the dividends paid per share of common stock. ( Note: Number of shares shown on balance sheet is not shown in thousands. The number of shares " in thousands" is 2 , 0 0 0 . ) Round...

-

Franklin Manufacturing manufactures two models of windows, bay windows and casement windows. Franklin uses an activity based costing system. The following information about the activities used to...

-

Exercise: Create a single script file that will evaluate all the equations below and display their respective results X= 5 . . y=10 x2y x + 2xy + y sin(x) + cos(y)

-

The campus bus at Haverford College is scheduled to arrive at the business school at 8:00 a.m. Usually, the bus arrives at the bus stop during the interval 7:568:03. Assume that the arrival time...

-

A sample of 100 former basketball players from Slam Dunk University shows that 55 of the players graduated in 4 years. Construct a 90 % confidence interval for the proportion of basketball players...

-

As a CEO, you are trying to decide whether to acquire a foreign firm. The size of your firm will double after this acquisition to become the largest in your industry. On the one hand, you are excited...

-

Suppose a bowler takes a random sample of 15 games she has bowled and finds the sample mean to be 172. She knows that the standard deviation of her score is 8. Construct a 99 % confidence interval...

-

Wolves are the planets most widespread land-based large mammals. They used to be humans most direct competitors for meat. As a result, the Big Bad Wolf occupied a center stage in our psyche as a...

-

"Compare and contrast the concepts of Total Quality Management ( TQM ) and Lean Management in the context of improving operational efficiency and quality within organizations. Discuss the fundamental...

-

When a company has a contract involving multiple performance obligations, how must the company recognize revenue?

-

Callaway SA has a deferred tax asset account with a balance of 150,000 at the end of 2018 due to a single cumulative temporary difference of 375,000. At the end of 2019, this same temporary...

-

Bradburn plc was formed 5 years ago through a public subscription of ordinary shares. Daniel Brown, who owns 15% of the ordinary shares, was one of the organizers of Bradburn and is its current...

-

To what extent do you consider the following items to be proper costs of the fixed asset? Give reasons for your opinions. (a) Overhead of a business that builds its own equipment. (b) Cash discounts...

-

If 25 women are randomly selected, find the probability that the mean of their red blood cell counts is less than 4.444. Assume that red blood cell counts of women are normally distributed with a...

-

Find the probability of an IQ less than 85.

-

What percentage of women have red blood cell counts in the normal range from 4.2 to 5.4? Assume that red blood cell counts of women are normally distributed with a mean of 4.577 and a standard...

Study smarter with the SolutionInn App