Question: Rework Example 4.3 but using a 2-year zero coupon bond for hedging, instead of the 10 year zero coupon bond. How do the results in

Rework Example 4.3 but using a 2-year zero couponbond for hedging, instead of the 10 year zero coupon bond. How do the results in Table 4.2 change?

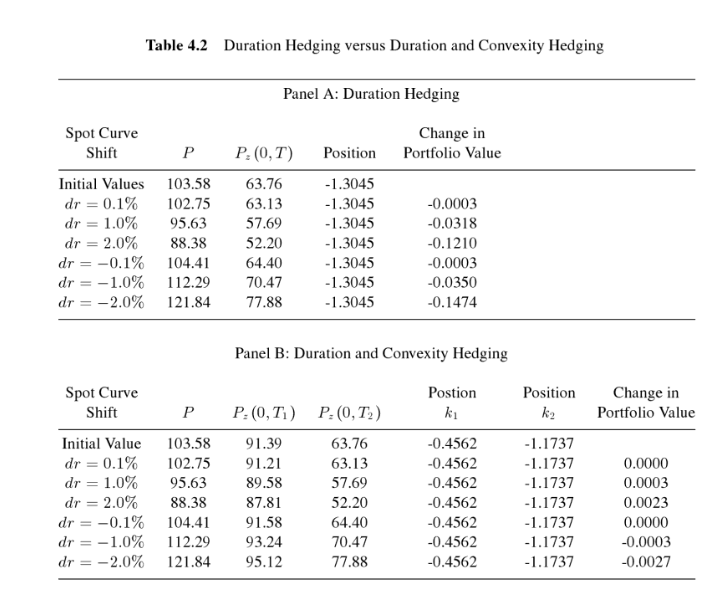

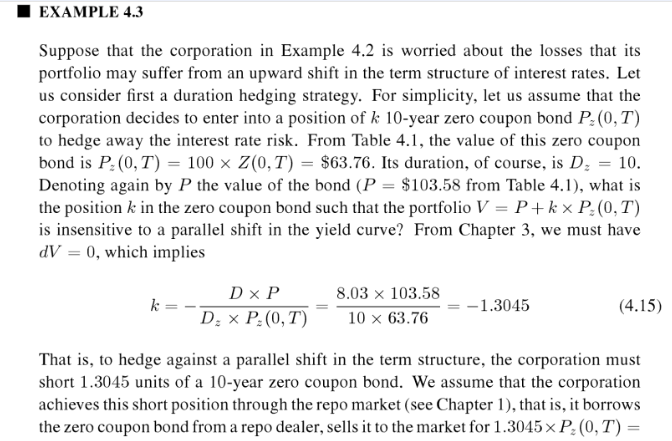

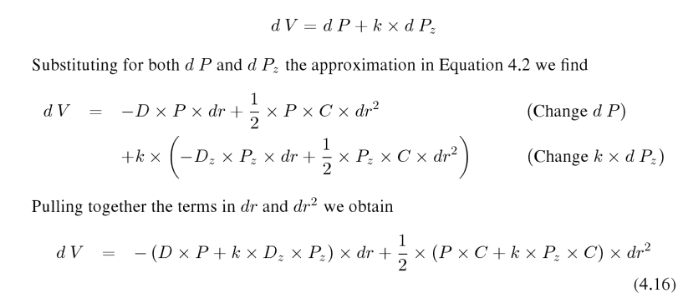

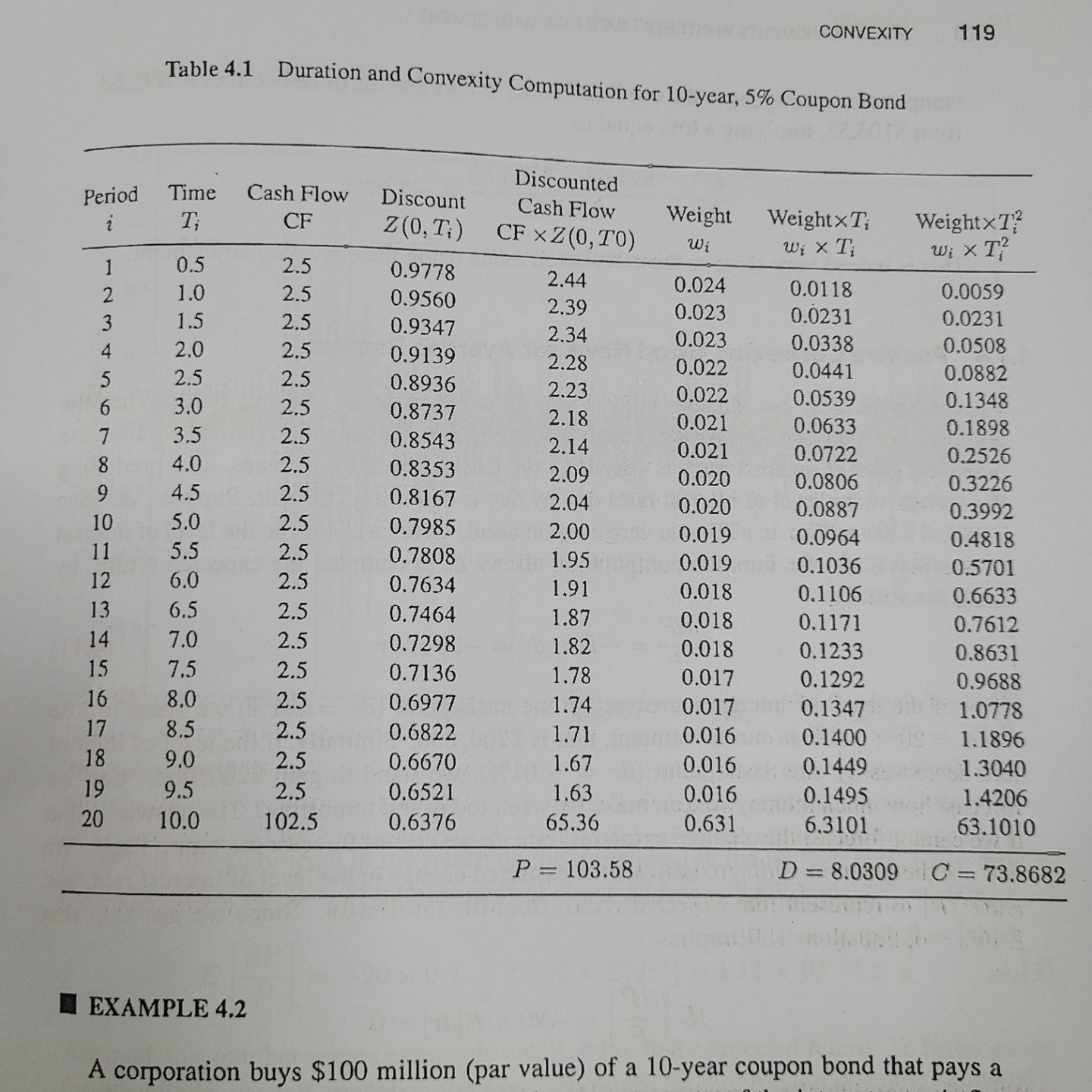

Table 4.2 Duration Hedging versus Duration and Convexity Hedging Panel A: Duration Hedging Spot Curve Change in Shift P P. (0, T) Position Portfolio Value Initial Values 103.58 63.76 -1.3045 dr = 0.1% 102.75 63.13 -1.3045 -0.0003 dr = 1.0% 95.63 57.69 -1.3045 -0.0318 dr = 2.0% 88.38 52.20 -1.3045 -0.1210 dr = -0.1% 104.41 64.40 -1.3045 -0.0003 dr = -1.0% 112.29 70.47 -1.3045 -0.0350 dr = -2.0% 121.84 77.88 -1.3045 -0.1474 Panel B: Duration and Convexity Hedging Spot Curve Postion Position Change in Shift P P. (0, TI) P. (0, T2 ) k1 k2 Portfolio Value Initial Value 103.58 91.39 63.76 -0.4562 -1.1737 dr = 0.1% 102.75 91.21 63.13 -0.4562 -1.1737 0.0000 dr = 1.0% 95.63 89.58 57.69 -0.4562 -1.1737 0.0003 dr = 2.0% 88.38 87.81 52.20 -0.4562 -1.1737 0.0023 dr = -0.1% 104.41 91.58 64.40 -0.4562 -1.1737 0.0000 dr = -1.0% 112.29 93.24 70.47 -0.4562 -1.1737 -0.0003 dr = -2.0% 121.84 95.12 77.88 -0.4562 -1.1737 -0.0027I EXAMPLE 4.3 Suppose that the corporation in Example 4.2 is worried about the losses that its portfolio may suffer from an upward shift in the term structure of interest rates. Let us consider rst a duration hedging strategy. For simplicity. let us assume that the corporation decides to enter into a position of k [Ct-year zero coupon bond P: (U, T) to hedge away the interest rate risk. From Table 4.1. the value of this zero coupon bond is Pgi, T] = me x Z(0,T) = $63.76. Its duration, of course. is D; = 1!}. Denoting again by P the value of the bond {P = $103.58 from Table 4.1), what is the position i: in me zero coupon bond such that the portfolio V = P + k x P: (0, T) is insensitive to a parallel shift in the yield curve? From Chapter 3. we must have 411' = D, which implies D x P 3.03 x 103.53 is = = = 4.3045 4.1 D; x PAM") 10 x cars l 5} That is. to hedge against a parallel shift in the term structure, the corporation must short 1.3045 units of a 10-year zero coupon bond. We assume that the corporation achieves this short position through the repo market (see Chapter 1}, that is, it borrows the zero coupon bond from a repo dealer. sells it to the market for 1.3045 x P: [0, T) = dV = dP+ kxdP. Substituting for both d P and d P. the approximation in Equation 4.2 we find dV = -D x P x dr + - x P x C x dr2 (Change d P) + x -D; X P X dr + - x P. x C x dr2 (Change k x d P.) Pulling together the terms in dr and dr? we obtain dV = - (D x P + k x D, x P ) x dr + NIK x (P X C + k xP x C) x dr2 (4.16)CONVEXITY 119 Table 4.1 Duration and Convexity Computation for 10-year, 5% Coupon Bond Period Time Cash Flow Discounted Discount Cash Flow Z (0, Ti ) Weight 2 CF Weightx Ti CF X Z(0, TO) WeightXT? Wi wi X Ti Wi X T? 0.5 2.5 0.9778 2.44 1.0 2.5 0.024 0.9560 0.0118 0.0059 2.39 0.023 0.0231 0.0231 A W N 1.5 2.5 0.9347 2.34 2.0 2.5 0.023 0.9139 0.0338 0.0508 2.28 2.5 2.5 0.022 0.0441 0.8936 0.0882 2.23 3.0 2.5 0.022 0.0539 0.8737 0.1348 2.18 0.021 3.5 2.5 0.0633 0.1898 0.8543 2.14 0.021 4.0 2.5 0.0722 0.2526 0.8353 2.09 0.020 4.5 0.0806 9 2.5 0.3226 0.8167 2.04 0.020 0.0887 0.3992 10 5.0 2.5 0.7985 2.00 0.019 0.0964 0.4818 11 5.5 2.5 0.7808 1.95 0.019 0.1036 0.5701 12 6.0 2.5 0.7634 1.91 0.018 0.1106 0.6633 W 6.5 2.5 0.7464 1.87 0.018 0.1171 0.7612 14 7.0 2.5 0.7298 1.82 0.018 0.1233 0.8631 15 7.5 2.5 0.7136 1.78 0.017 0.1292 0.9688 16 8.0 2.5 0.6977 1.74 0.017 0.1347 1.0778 17 8.5 2.5 0.6822 1.71 0.016 0.1400 1.1896 18 9.0 2.5 0.6670 1.67 0.016 0.1449 1.3040 19 9.5 2.5 0.6521 1.63 0.016 0.1495 1.4206 20 10.0 102.5 0.6376 65.36 0.631 6.3101 63.1010 P = 103.58 D = 8.0309 C = 73.8682 EXAMPLE 4.2 A corporation buys $100 million (par value) of a 10-year coupon bond that pays a

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!