Question: Richard Derick has asked you to develop a sampling plan to determine the extent of misstatements in classifying expenditures as repairs and maintenance expense or

Richard Derick has asked you to develop a sampling plan to determine the extent of misstatements in classifying expenditures as repairs and maintenance expense or factory equipment additions. Given the problems noted during control testing (as described in Module II), Derick believes that significant misstatements may have occurred.

The same vendor's invoice frequently contains charges for parts and supplies as well as equipment, and the Brony's Bikes employees preparing the vouchers sometimes fail to distinguish among the charges and simply indicate "factory equipment" as the debit if the invoice amount is large. Inasmuch as this type of misstatement would cause an overstatement in the factory equipment account, Derick instructs you to use MUS sampling for the lower stratum to determine the extent to which such misstatements may have occurred during 20X9. In the Johnstone textbook, MUS is used interchangeably with the term PPS, which MUS is a subset. Of the total debits, $89,860,000 to factory equipment during 20X9, major additions in the amount of $77,260,000 have been made to replace worn-out equipment. The lower stratum contains 1,246 items for a total dollar amount of $12,600,000. Derick has decided to audit the upper stratum of the population containing the major additions in its entirety. You are asked to test the lower stratum on a sampling basis.

Requirements

1. What is the objective of performing the test of factory equipment expenditures? What is the population? What is the sampling unit?

2. Using Excel download the file labeled "20X9_mus." Locate the following documentation in the file:

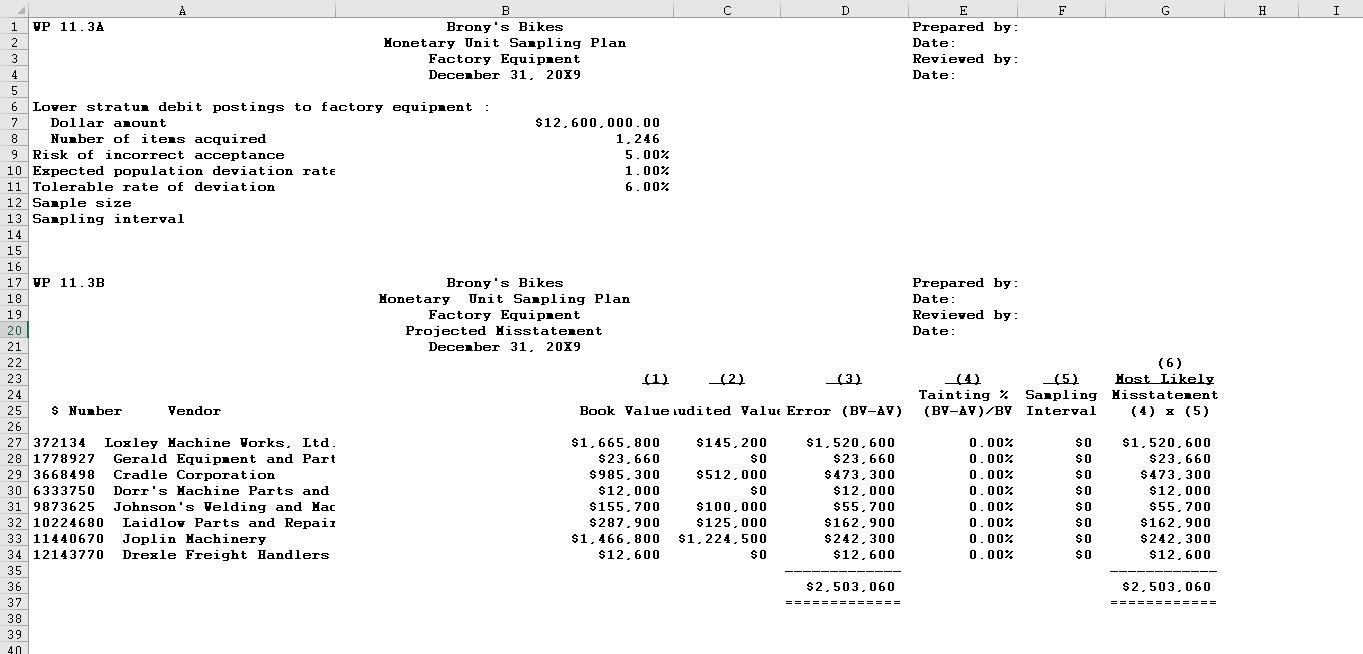

WP 11.3A—Monetary unit sampling plan;

WP 11.3B—Monetary unit sampling plan—projected misstatement; and

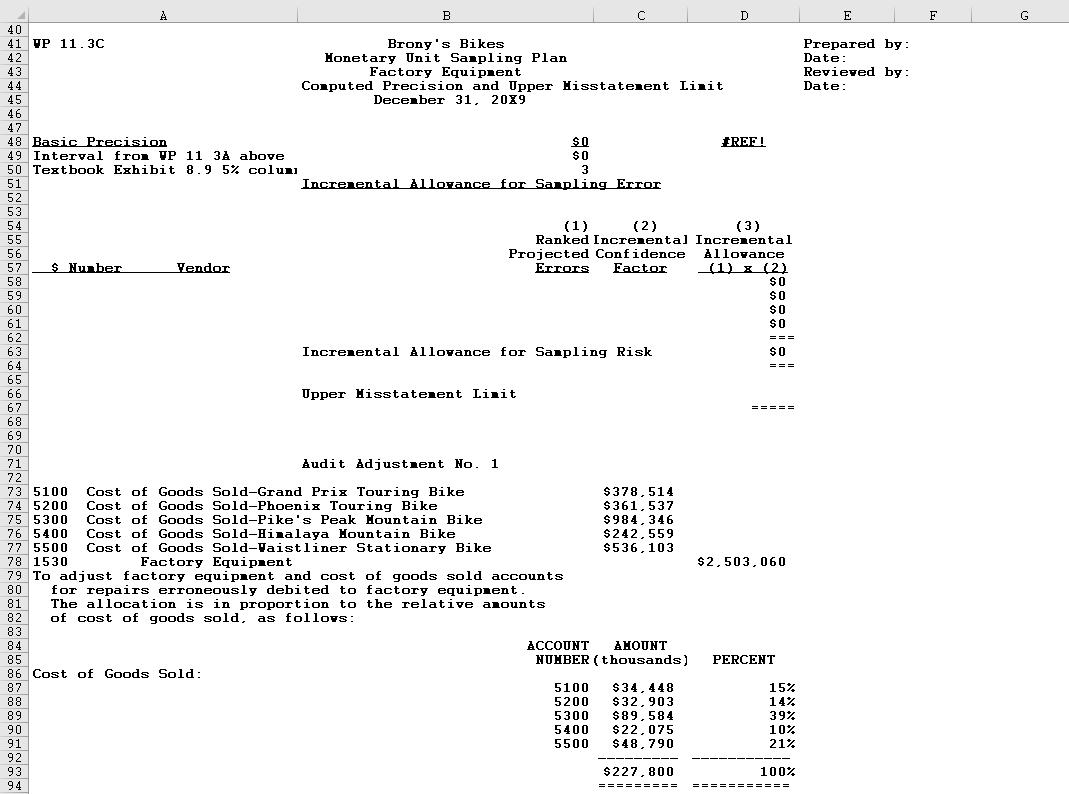

WP 11.3C—Monetary unit sampling plan—computed precision and upper misstatement limit.

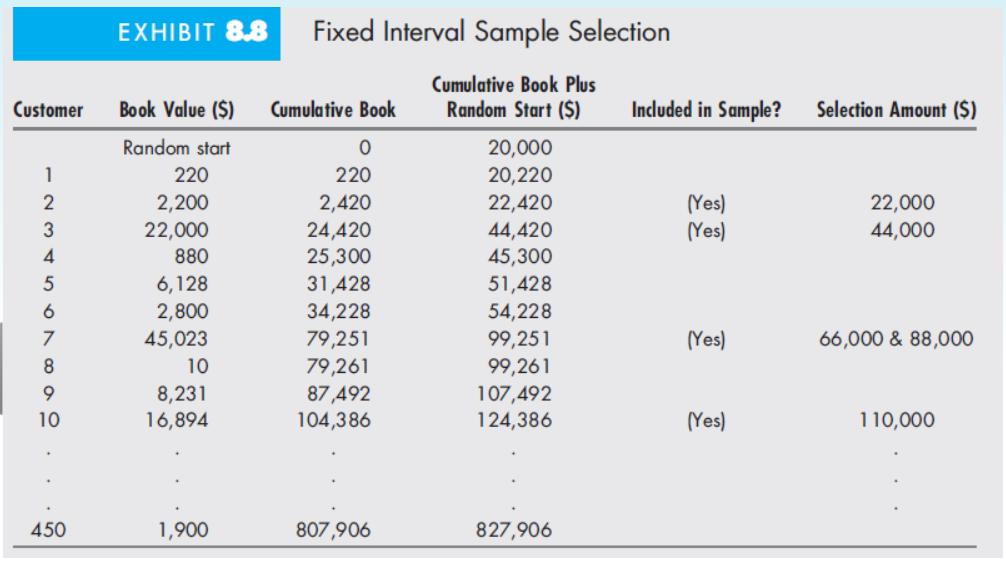

Scroll to WP 11.3A, "Monetary Unit Sampling Plan." Determine sample size from textbook Exhibit 8.5 Table 1 assuming Derick has set the parameters stated below. Calculate the sampling interval.

| Risk of incorrect acceptance: | 5% or 95% confidence |

| Expected population deviation rate: | 1% based on auditor's prior experience with the entity |

| Tolerable rate of deviation: | 6% determined by auditor; if actual exceeds 6%, the control probably has failed |

3. What factors did Derick consider in setting these parameters?

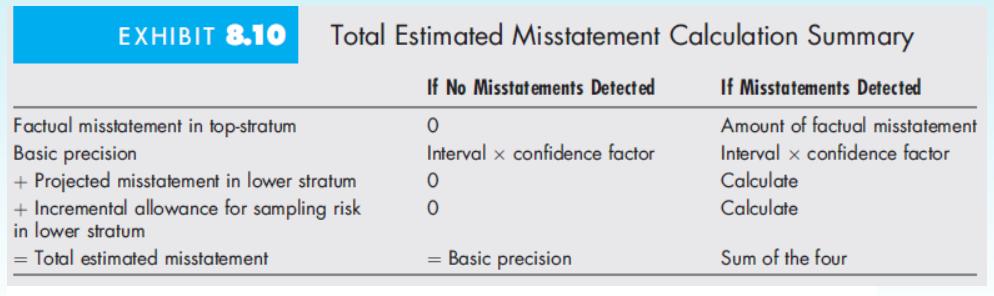

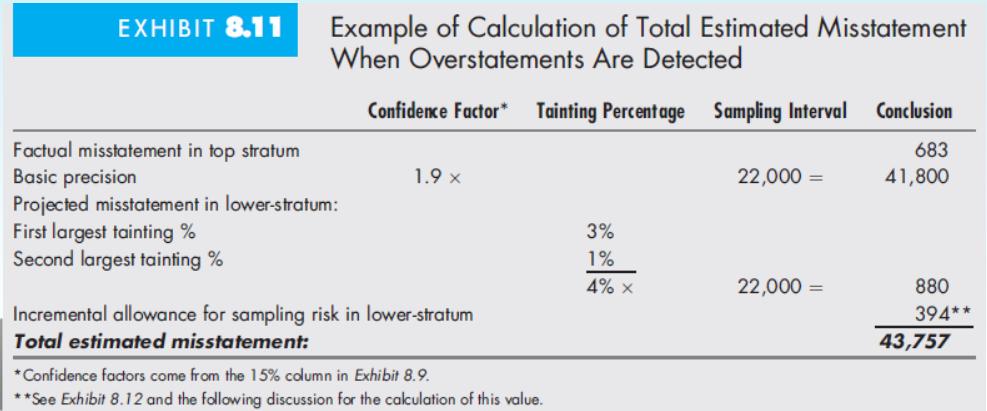

4. Scroll to WP 11.3B, "Monetary Unit Sampling Plan—Projected Misstatement." This document summarizes all invoices containing posting errors and calculates the projected misstatement. Column 3 is already computed for you to determine the amount of the misstatement for that item. The equations for columns 4, 5 and 6 have been incorporated into the worksheet for you. Refer to textbook Exhibit 8.11 to see how the formulas were determined. What factor determines whether a "tainting percentage" appears in column 4?

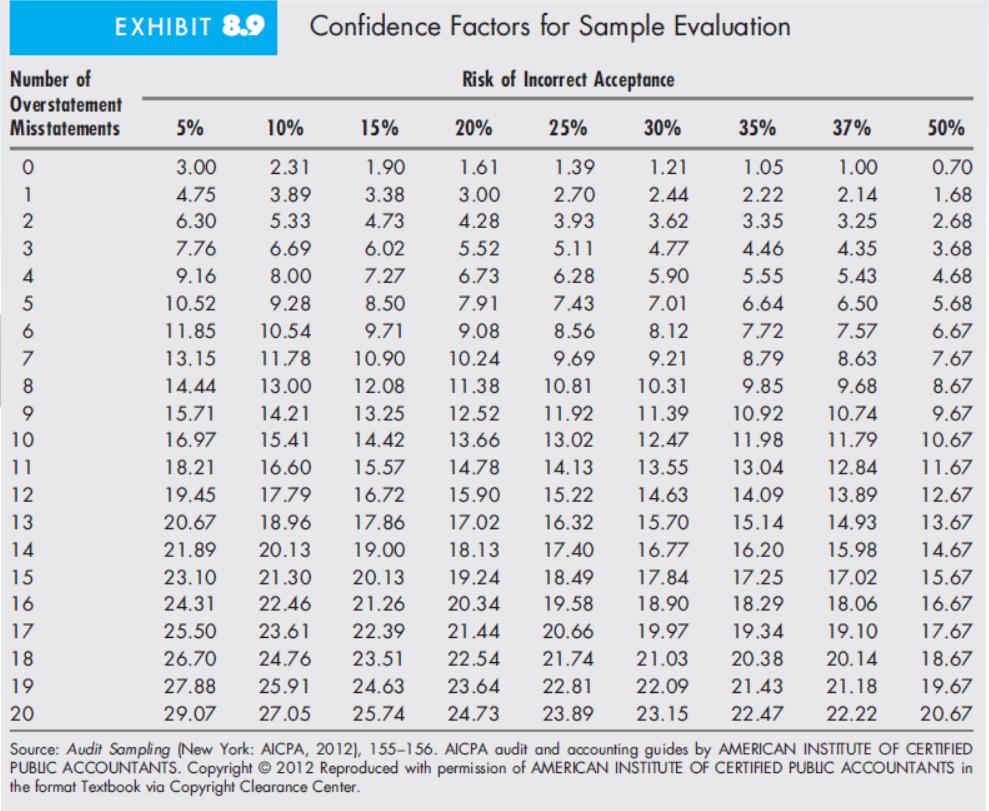

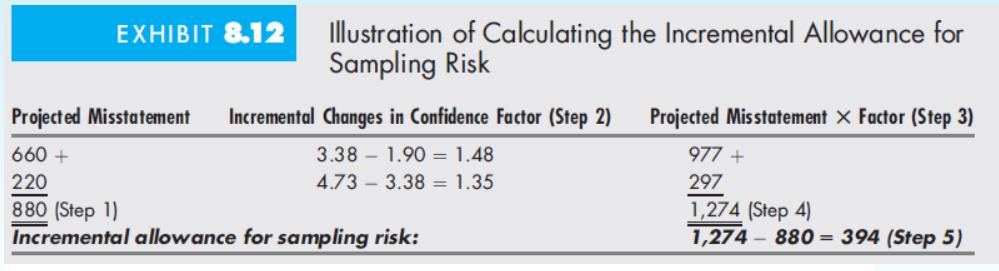

5. Scroll to WP 11.3C, "Monetary Unit Sampling Plan—Computed Precision and Upper Misstatement Limit." Complete the "Incremental Allowance for Sampling Risk" schedule by ranking the projected misstatements as appropriate. Textbook Exhibit 8.11 and Exhibit 8.12 (illustrate how this calculation is performed manually. There are four misstatements identified. Use the values in textbook Exhibit 8.9 5% risk of incorrect acceptance column and the rows 0-4.

6. Explain the meaning of the following amounts:

a. Basic precision;

b. Incremental allowance for sampling error;

c. Upper misstatement limit.

7. Evaluate the sampling results. Do they support Derick's concerns regarding possible material misstatement? Note the audit adjustment based on misstatements discovered while examining the sample. Is this adjustment adequate to bring the population into acceptable bounds? If not, what alternate actions might you choose to pursue, based on the sampling results?

EXCEL FILE 20X9_MUS:

A B D E F G H I 11. Brony's Bikes Honetary Unit Sanpling Plan Factory Equipnent Decenber 31, 20X9 Prepared by: Date: 3. Revieved by: 4 Date: 5 6. Lover stratun debit postings to factory equipnent : 7 Dollar anount $12,600,000.00 Nuaber of itens acquired 1.246 9. 9 Risk of incorrect acceptance 5.00% 1.00% 10 Expected population deviation rate 11 Tolerable rate of deviation 6.00% 12 Sanple size 13 Sampling interval 14 15 16 17 UP 11. 3B Prepared by: Brony's Bikes Unit Sanpling Plan 18 Honetary Date: Revieved by : Factory Equipnent Projected Hisstatenent Deceaber 31, 20X9 19 20 21 Date: 22 (6) Host Likely 23 (4) Tainting % Sampling Hisstatenent (BV-AV)/BV Interval (1) (2) (3) (5) 24 25 $ Nunber Vendor Book Value iudited Value Error (BV-AV) (4) x (5) 26 27 372134 Loxley Hachine Vorks, Ltd. $1,665,800 $145, 200 $1.520,600 0.00% $0 $1,520,600 28 1778927 Gerald Equipnent and Part Cradle Corporation $23,660 $0 $23,660 $473, 300 0.00% $0 $23,660 29 3668498 $512,000 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% $985, 300 $0 $473, 300 30 6333750 Dorr's Hachine Parts and $12,000 $0 $12,000 $0 $12,000 Johnson's Velding and Hac Laidlov Parts and Repair 31 9873625 $155,700 $100.000 $55, 700 $0 $55, 700 32 10224680 $125,000 $287, 900 $1,466,800 $1, 224,500 $12,600 $162,900 $242,300 $162,900 $242,300 $0 33 11440670 Joplin Hachinery $0 34 12143770 Drexle Freight Handlers $0 $12,600 $0 $12,600 35 36 $2,503,060 $2,503.060 37 ==-= ===== ===- I-- 38 39 40

Step by Step Solution

3.55 Rating (172 Votes )

There are 3 Steps involved in it

The objectives are as follows The audit team as described in the passage expects to find few misstatements having done all the planning in module 12 and m to eliminate the errors Provide evidence rega... View full answer

Get step-by-step solutions from verified subject matter experts