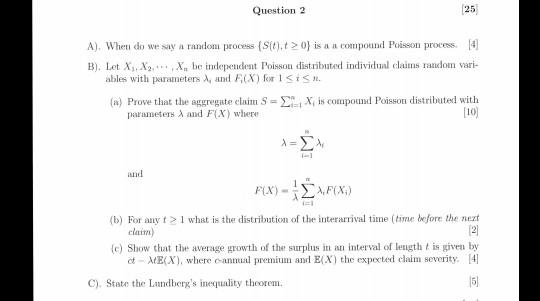

Question: risk theory Question 2 25 A). Where do we say a random process (Sit).t > 0) is a compound Poisson process. [4] B). Let X,

risk theory

Question 2 25 A). Where do we say a random process (Sit).t > 0) is a compound Poisson process. [4] B). Let X, XX, be independent Poisson distributed individual claims random vari- abiles with parameters, and F(X) for ISIS.. (a) Prove that the aggregate claimsis compound Poisson distributed with parameters, and F(X) where (10) = and F{X) - SFX (b) For any t > 1 what is the distribution of the interarrival time (time Iwfore the next claim) 2 c) Show that the average growth of the surplus in an interval of length is given by AE(X), where annual premium and E(X) the expected claim severity 141 C). State the Landberg's inequality theorem. 15 Question 2 25 A). Where do we say a random process (Sit).t > 0) is a compound Poisson process. [4] B). Let X, XX, be independent Poisson distributed individual claims random vari- abiles with parameters, and F(X) for ISIS.. (a) Prove that the aggregate claimsis compound Poisson distributed with parameters, and F(X) where (10) = and F{X) - SFX (b) For any t > 1 what is the distribution of the interarrival time (time Iwfore the next claim) 2 c) Show that the average growth of the surplus in an interval of length is given by AE(X), where annual premium and E(X) the expected claim severity 141 C). State the Landberg's inequality theorem. 15

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts