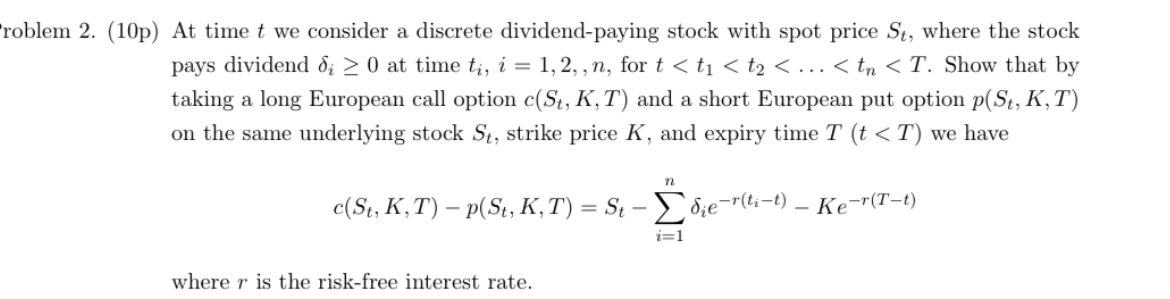

Question: roblem 2 . ( 1 0 p ) At time t we consider a discrete dividend - paying stock with spot price S t ,

roblem p At time we consider a discrete dividendpaying stock with spot price where the stock

pays dividend at time for

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock