Rual Ltd. is a Canadian controlled private corporation (CCPC) with a December 31 year end. The...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

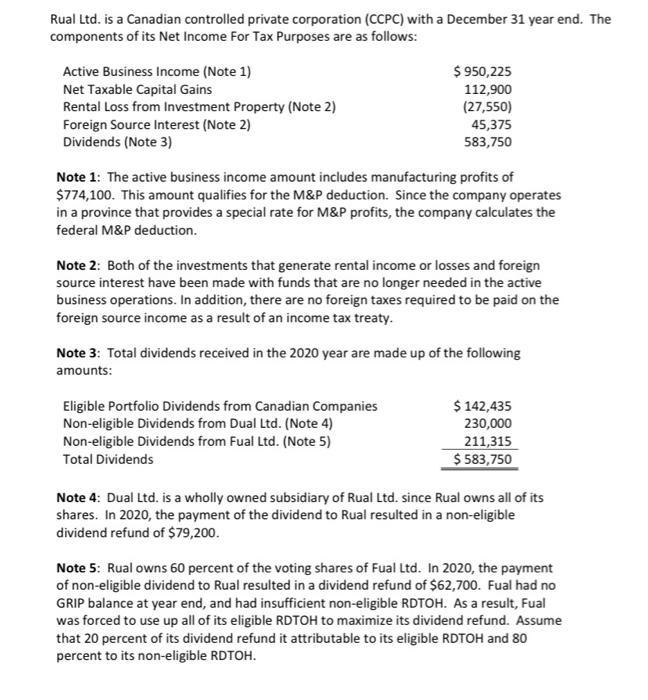

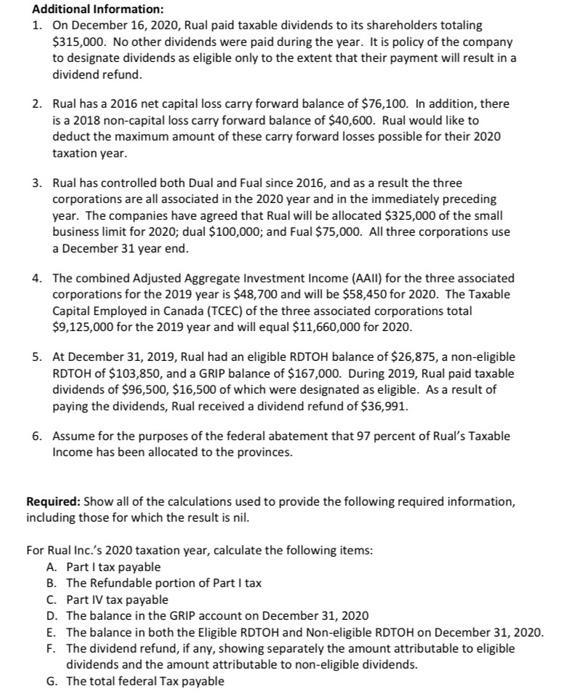

Rual Ltd. is a Canadian controlled private corporation (CCPC) with a December 31 year end. The components of its Net Income For Tax Purposes are as follows: Active Business Income (Note 1) Net Taxable Capital Gains Rental Loss from Investment Property (Note 2) Foreign Source Interest (Note 2) Dividends (Note 3) $ 950,225 112,900 (27,550) 45,375 583,750 Note 1: The active business income amount includes manufacturing profits of $774,100. This amount qualifies for the M&P deduction. Since the company operates in a province that provides a special rate for M&P profits, the company calculates the federal M&P deduction. Note 2: Both of the investments that generate rental income or losses and foreign source interest have been made with funds that are no longer needed in the active business operations. In addition, there are no foreign taxes required to be paid on the foreign source income as a result of an income tax treaty. Note 3: Total dividends received in the 2020 year are made up of the following amounts: Eligible Portfolio Dividends from Canadian Companies Non-eligible Dividends from Dual Ltd. (Note 4) Non-eligible Dividends from Fual Ltd. (Note 5) Total Dividends $ 142,435 230,000 211,315 $ 583,750 Note 4: Dual Ltd. is a wholly owned subsidiary of Rual Ltd. since Rual owns all of its shares. In 2020, the payment of the dividend to Rual resulted in a non-eligible dividend refund of $79,200. Note 5: Rual owns 60 percent of the voting shares of Fual Ltd. In 2020, the payment of non-eligible dividend to Rual resulted in a dividend refund of $62,700. Fual had no GRIP balance at year end, and had insufficient non-eligible RDTOH. As a result, Fual was forced to use up all of its eligible RDTOH to maximize its dividend refund. Assume that 20 percent of its dividend refund it attributable to its eligible RDTOH and 80 percent to its non-eligible RDTOH. Additional Information: 1. On December 16, 2020, Rual paid taxable dividends to its shareholders totaling $315,000. No other dividends were paid during the year. It is policy of the company to designate dividends as eligible only to the extent that their payment will result in a dividend refund. 2. Rual has a 2016 net capital loss carry forward balance of $76,100. In addition, there is a 2018 non-capital loss carry forward balance of $40,600. Rual would like to deduct the maximum amount of these carry forward losses possible for their 2020 taxation year. 3. Rual has controlled both Dual and Fual since 2016, and as a result the three corporations are all associated in the 2020 year and in the immediately preceding year. The companies have agreed that Rual will be allocated $325,000 of the small business limit for 2020; dual $100,000; and Fual $75,000. All three corporations use a December 31 year end. 4. The combined Adjusted Aggregate Investment Income (AAII) for the three associated corporations for the 2019 year is $48,700 and will be $58,450 for 2020. The Taxable Capital Employed in Canada (TCEC) of the three associated corporations total $9,125,000 for the 2019 year and will equal $11,660,000 for 2020. 5. At December 31, 2019, Rual had an eligible RDTOH balance of $26,875, a non-eligible RDTOH of $103,850, and a GRIP balance of $167,000. During 2019, Rual paid taxable dividends of $96,500, $16,500 of which were designated as eligible. As a result of paying the dividends, Rual received a dividend refund of $36,991. 6. Assume for the purposes of the federal abatement that 97 percent of Rual's Taxable Income has been allocated to the provinces. Required: Show all of the calculations used to provide the following required information, including those for which the result is nil. For Rual Inc.'s 2020 taxation year, calculate the following items: A. Part I tax payable B. The Refundable portion of Part I tax C. Part IV tax payable D. The balance in the GRIP account on December 31, 2020 E. The balance in both the Eligible RDTOH and Non-eligible RDTOH on December 31, 2020. F. The dividend refund, if any, showing separately the amount attributable to eligible dividends and the amount attributable to non-eligible dividends. G. The total federal Tax payable Rual Ltd. is a Canadian controlled private corporation (CCPC) with a December 31 year end. The components of its Net Income For Tax Purposes are as follows: Active Business Income (Note 1) Net Taxable Capital Gains Rental Loss from Investment Property (Note 2) Foreign Source Interest (Note 2) Dividends (Note 3) $ 950,225 112,900 (27,550) 45,375 583,750 Note 1: The active business income amount includes manufacturing profits of $774,100. This amount qualifies for the M&P deduction. Since the company operates in a province that provides a special rate for M&P profits, the company calculates the federal M&P deduction. Note 2: Both of the investments that generate rental income or losses and foreign source interest have been made with funds that are no longer needed in the active business operations. In addition, there are no foreign taxes required to be paid on the foreign source income as a result of an income tax treaty. Note 3: Total dividends received in the 2020 year are made up of the following amounts: Eligible Portfolio Dividends from Canadian Companies Non-eligible Dividends from Dual Ltd. (Note 4) Non-eligible Dividends from Fual Ltd. (Note 5) Total Dividends $ 142,435 230,000 211,315 $ 583,750 Note 4: Dual Ltd. is a wholly owned subsidiary of Rual Ltd. since Rual owns all of its shares. In 2020, the payment of the dividend to Rual resulted in a non-eligible dividend refund of $79,200. Note 5: Rual owns 60 percent of the voting shares of Fual Ltd. In 2020, the payment of non-eligible dividend to Rual resulted in a dividend refund of $62,700. Fual had no GRIP balance at year end, and had insufficient non-eligible RDTOH. As a result, Fual was forced to use up all of its eligible RDTOH to maximize its dividend refund. Assume that 20 percent of its dividend refund it attributable to its eligible RDTOH and 80 percent to its non-eligible RDTOH. Additional Information: 1. On December 16, 2020, Rual paid taxable dividends to its shareholders totaling $315,000. No other dividends were paid during the year. It is policy of the company to designate dividends as eligible only to the extent that their payment will result in a dividend refund. 2. Rual has a 2016 net capital loss carry forward balance of $76,100. In addition, there is a 2018 non-capital loss carry forward balance of $40,600. Rual would like to deduct the maximum amount of these carry forward losses possible for their 2020 taxation year. 3. Rual has controlled both Dual and Fual since 2016, and as a result the three corporations are all associated in the 2020 year and in the immediately preceding year. The companies have agreed that Rual will be allocated $325,000 of the small business limit for 2020; dual $100,000; and Fual $75,000. All three corporations use a December 31 year end. 4. The combined Adjusted Aggregate Investment Income (AAII) for the three associated corporations for the 2019 year is $48,700 and will be $58,450 for 2020. The Taxable Capital Employed in Canada (TCEC) of the three associated corporations total $9,125,000 for the 2019 year and will equal $11,660,000 for 2020. 5. At December 31, 2019, Rual had an eligible RDTOH balance of $26,875, a non-eligible RDTOH of $103,850, and a GRIP balance of $167,000. During 2019, Rual paid taxable dividends of $96,500, $16,500 of which were designated as eligible. As a result of paying the dividends, Rual received a dividend refund of $36,991. 6. Assume for the purposes of the federal abatement that 97 percent of Rual's Taxable Income has been allocated to the provinces. Required: Show all of the calculations used to provide the following required information, including those for which the result is nil. For Rual Inc.'s 2020 taxation year, calculate the following items: A. Part I tax payable B. The Refundable portion of Part I tax C. Part IV tax payable D. The balance in the GRIP account on December 31, 2020 E. The balance in both the Eligible RDTOH and Non-eligible RDTOH on December 31, 2020. F. The dividend refund, if any, showing separately the amount attributable to eligible dividends and the amount attributable to non-eligible dividends. G. The total federal Tax payable

Expert Answer:

Answer rating: 100% (QA)

To calculate the required information for Rual Incs 2020 taxation year we need to follow the steps below A Calculation of Part I Tax Payable 1 Calcula... View the full answer

Related Book For

Canadian Income Taxation Planning And Decision Making

ISBN: 9781259094330

17th Edition 2014-2015 Version

Authors: Joan Kitunen, William Buckwold

Posted Date:

Students also viewed these law questions

-

A bakery with a December 31 st year end purchased new equipment on October 31 st 2000 for $10,000. This was their first equipment purchase. Required: What are the tax consequences if the equipment is...

-

Falko Ltd. is canadian controlled privated corporation with a december31 year end. For its year ending december 31, 2020, its acounting net income before taxes before taxes, as determined using...

-

Tern Corporation, a calendar year C corporation, is solely owned by Jessica Ramirez. Terns only business since its incorporation in 2011 has been land surveying services. In Terns state of...

-

In a study of the Gender Aide method of gender selection used to increase the likelihood of a baby being born a girl, 2000 users of the method gave birth to 980 boys and 1020 girls. There is about a...

-

Delta Airlines is working on pricing its own flights between Detroit Metro Airport and Minneapolis-St. Paul Airport. Over years of flying the route, Delta knows that the weekly demand curve it faces...

-

Show that the competitive labor market compensates workers for the probability that they will be laid off.

-

Applin Corporation has a desired rate of return of 8 percent. Troy Anderson is in charge of one of Applins three investment centers. His center controlled operating assets of $5,000,000 that were...

-

Each of the four independent situations below describes a finance lease in which annual lease payments are payable at the beginning of each year. The lessee is aware of the lessor's implicit rate of...

-

Gourmet Coffee (GC) is a specialty coffee shop that sells roasted coffee beans. It buys green beans, roasts them in its shop, and then sells them to the consumer. GC estimates that it sells about...

-

A manufacturer produces goods at five US cities, from which the goods are sent to seven major customers in the following cities: Frankfort, Greenville, Jackson, Kankakee, Louisville, Miami, and...

-

Tom deposited $5000 in a savings account that paid 8% interest compounded quarterly what is the effective rate of interest

-

Dennis Dallas, the third-generation owner of Dallas Construction, met with his insurance group to review the group's annual summary of safety performance. To his surprise, Dallas Construction's...

-

Briefly outline the key points of the case found in the Lexis-Nexis database

-

In many Northern European urban areas, the bicycle is considered a serious mode of transport. Not just by fitness freaks or teenagers: in cities such as Amsterdam and Copenhagen you can expect to see...

-

What is the FINANCIAL relavance of liabilities ( debts of a company ) in dietetics practice?

-

Kuh Lin Hills Plc is a company which was financed by the issue of the following shares and debentures: $000 2000 1 000 500 2 000 000 Ordinary shares of $1 each 1 000 000 8% Preference shares of $1...

-

What is an access control list?

-

Using the information provided in Question Eight, determine TV Ltd.s refundable tax on investment income. Income tax reference: ITA 123.3, 129(4).

-

Robert Blackwell owns 100% of the outstanding shares of Black Inc., a qualified small business corporation. The shares have a paid-up capital (PUC) and an adjusted cost base of $50,000 and a fair...

-

Briefly explain how using a holding company to own the shares of an active business corporation may be beneficial when the shares of the active business corporation are about to be sold. In what...

-

Using the potential theory obtain the damping for a cycle of (i) plunge, (ii) pitch oscillations.

-

Consider a delta wing with sweep angle \(\Lambda\). Show that the expressions 8.11 and 8.12 give the same lift line slope for the delta wing. Eq 8.11 Eq 8.12 = CD CD+CL tan

-

Using the Polhamus theory obtain the drag polar for a delta wing with sweep angle \(75^{\circ}\).

Study smarter with the SolutionInn App