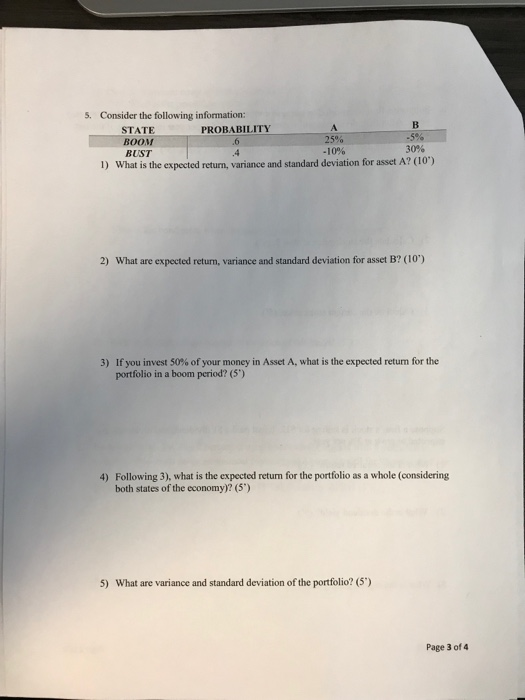

Question: s. Consider the following information: STATE BOOM BUST PROBABILITY .6 A. 25% -10% -5% 30% 1) What is the expected return, variance and standard deviation

s. Consider the following information: STATE BOOM BUST PROBABILITY .6 A. 25% -10% -5% 30% 1) What is the expected return, variance and standard deviation for asset A? (10) 2) What are expected returm, variance and standard deviation for asset B? (10') If you invest 50% of your money in Asset A, what is the expected return for the portfolio in a boom period? (5') 3) 4) Following 3), what is the expected return for the portfolio as a whole (considering both states of the economy)? (5) 5) What are variance and standard deviation of the portfolio? (5") Page 3 of 4

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock