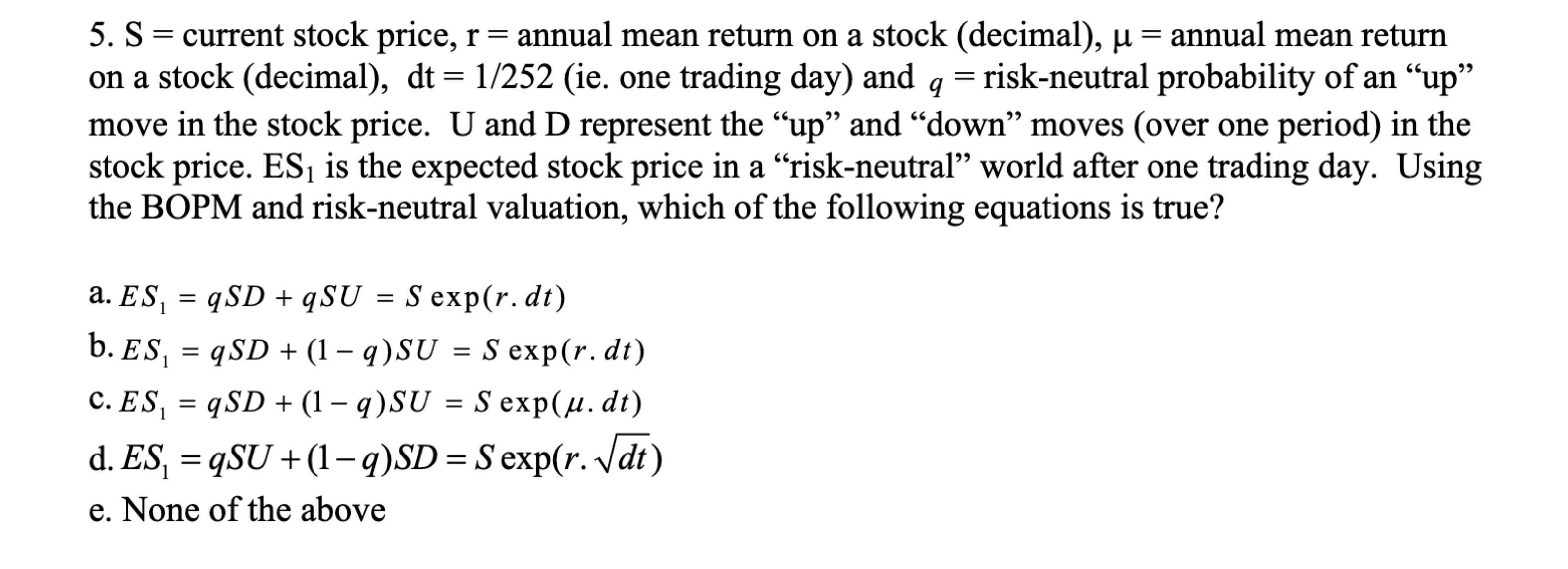

Question: S = current stock price, r = annual mean return on a stock ( decimal ) , = annual mean return on a stock (

current stock price, annual mean return on a stock decimal annual mean return

on a stock decimalie one trading day and riskneutral probability of an up

move in the stock price. U and D represent the up and "down" moves over one period in the

stock price. is the expected stock price in a "riskneutral" world after one trading day. Using

the BOPM and riskneutral valuation, which of the following equations is true?

aqSUSexp

bSexp

cSexp

dqSUSexp

e None of the above

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock