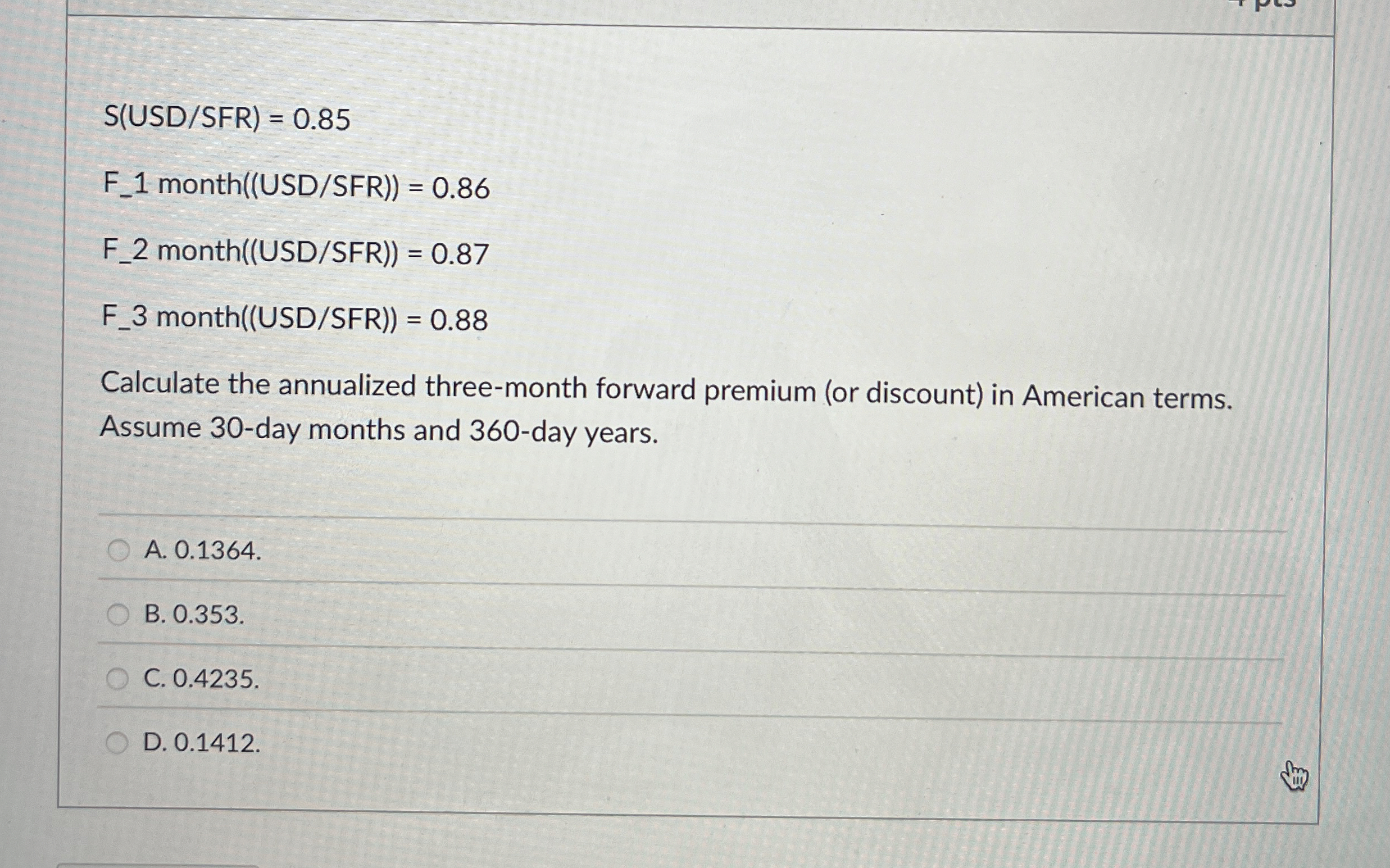

Question: S ( U S D S F R ) = 0 . 8 5 F _ 1 month ( ( U S D S F

F month

F month

F monthUSDSFR

Calculate the annualized threemonth forward premium or discount in American terms.

Assume day months and day years.

A

B

C

D

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock