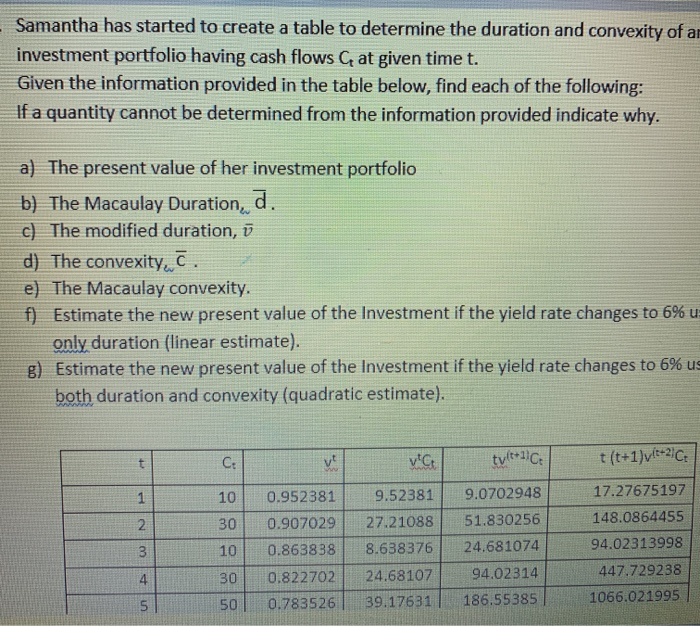

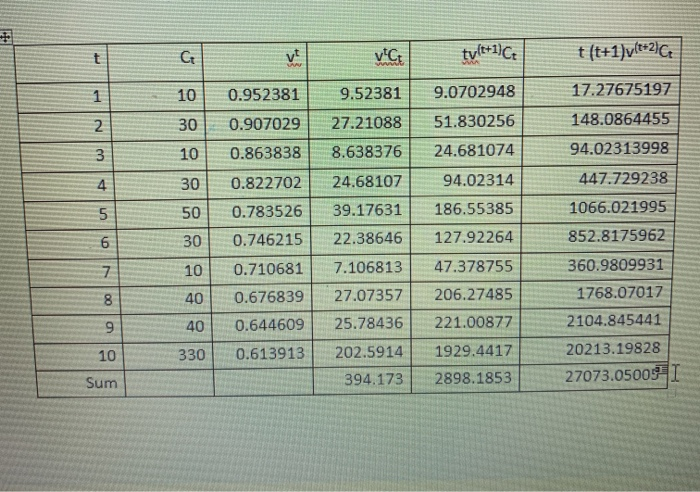

Question: Samantha has started to create a table to determine the duration and convexity of a investment portfolio having cash flows C at given time t.

Samantha has started to create a table to determine the duration and convexity of a investment portfolio having cash flows C at given time t. Given the information provided in the table below, find each of the following: If a quantity cannot be determined from the information provided indicate why. a) The present value of her investment portfolio b) The Macaulay Duration, d. c) The modified duration, d) The convexity, C. e) The Macaulay convexity. f) Estimate the new present value of the Investment if the yield rate changes to 6% u only duration (linear estimate). 8) Estimate the new present value of the Investment if the yield rate changes to 6% us both duration and convexity (quadratic estimate). N 0.952381 0.907029 0.863838 0.822702 0.783526 vice 9.52381 27.21088 8.638376 24.68107 39.17631 tvlt! 9.0702948 51.830256 24.681074 94.02314 186.55385 t(t+1)v-2C: 17.27675197 148.0864455 94.02313998 447.729238 1 066.021995 un 50 G WN 50 v VG 0.952381 9.52381 0.907029 27.21088 0.863838 8.638376 0.822702 24.68107 | 0.783526 39.17631 0.746215 22.38646 0.710681 7.106813 0.676839 27.07357 0.644609 25.78436 0.613913 | 202.5914 394.173 tv(t+1)Ctt (t+1]y[t*2 9.0702948 17.27675197 51.830256 148.0864455 24.681074 94.02313998 94.02314 447.729238 186.55385 1066.021995 127.92264 852.8175962 47.378755 360.9809931 206.27485 1768.07017 221.00877 2104.845441 1929.4417 20213.19828 2898.1853 27073.050031 00 O 3 30 10 Sum

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts