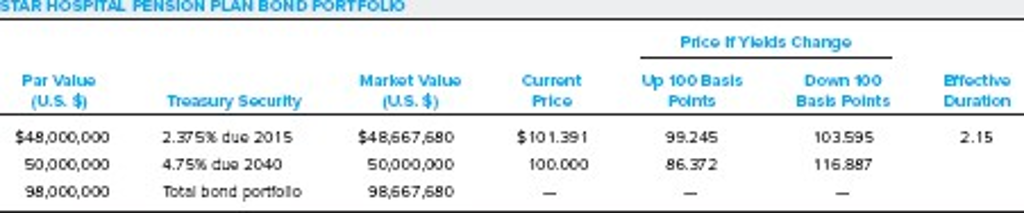

Question: Sandra Kapple presents Maria VanHusen with a description, given in the following exhibit, of the bond portfolio held by the Star Hospital Pension Plan. All

Sandra Kapple presents Maria VanHusen with a description, given in the following exhibit, of the bond portfolio held by the Star Hospital Pension Plan. All securities in the bond portfolio are noncallable U.S. Treasury securities.

a) Calculate the effective duration of each of the following:

1) The 4.75% Treasury security due 2040. 2) The total bond portfolio

b) VanHusen remarks to Kapple, If you changed the maturity structure of the bond portfolio to result in a portfolio duration of 5.25, the price sensitivity of that portfolio would be identical to the price sensitivity of a single, noncallable Treasury security that has a duration of 5.25. In what circumstance would VanHusen's remark be correct?

SHOW ALL WORK!

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts