Santiago Hernandez, was 65 when he retired in 2014. Maria, his wife of 40 years, passed away

Question:

Santiago Hernandez, was 65 when he retired in 2014. Maria, his wife of 40 years, passed away the next year. Her will left everything to Santiago. Although Maria's estate was valued at $2,250,000, there was no estate tax due because of the 100 percent marital deduction. Their only child, Samuel, is married to Luna. They have four children, two in college and two in high school. In 2015, Santiago made a gift of Microsoft stock worth $260,000 jointly to Samuel and Luna. Because of the two $14,000 annual exclusions and the unified credit, no gift taxes were due. When Santiago died in 2018, his home was valued at $850,000, his vacation cabin was valued at $500,000, his investments in stocks and bonds were valued at $1,890,000, and his pension funds were worth $650,000 (Samuel was named beneficiary). Santiago also owned a life insurance policy that paid proceeds of $720,000 to Samuel. He left $60,000 to his church and $25,000 to his high school to start a scholarship fund in his wife's name. The rest of the estate was left to Samuel. Funeral costs were $13,000. Debts were $90,000 and miscellaneous expenses were $25,000. Attorney and accounting fees came to $37,000. Use Worksheet 15.1 to guide your estate tax calculations as you complete these exercises.

- Compute the value of Santiago's probate estate.

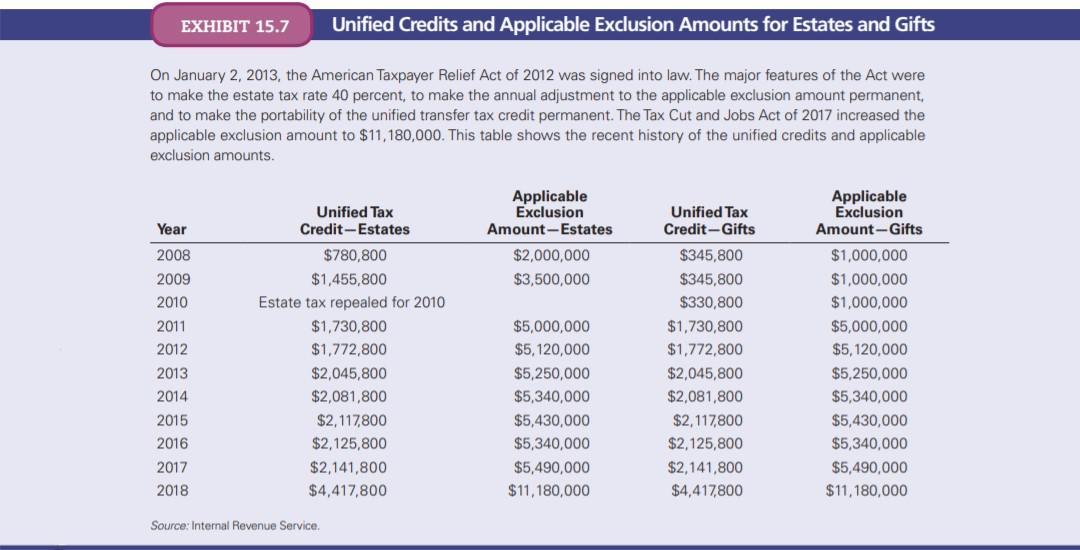

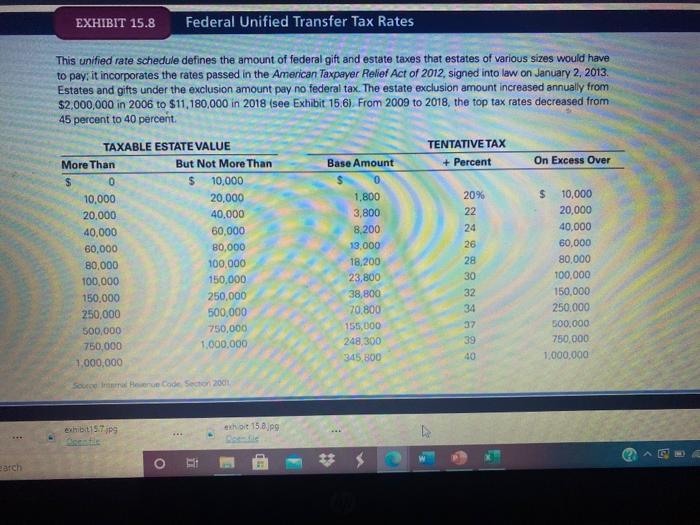

| aUse Exhibit 15.8 to calculate the tentative tax. | ||||||||||

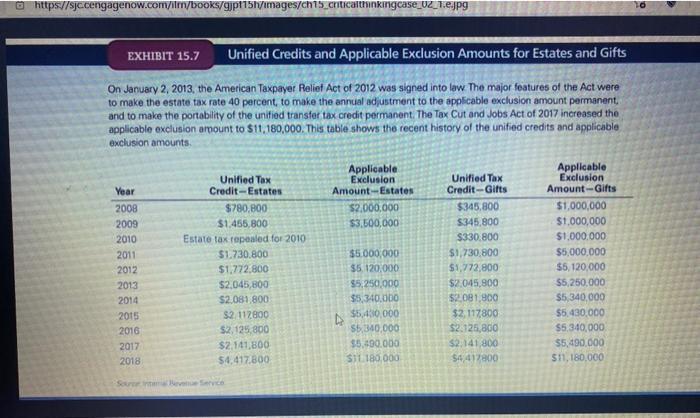

| bUse Exhibit 15.7 to determine the appropriate unified credit. | ||||||||||

| cNote that the amount shown on line 7 is a significant number, because most states use the same estate tax base as is used for the federal tax | ||||||||||

Expert Answer:

Answer PARTICULARS Grass estate Lesso Funeral expense Administrative Expense Debts othe... View the full answer