Question: sas ' 1. Sales Journal 2. Purchases Journal 3. Cash Receipts Journal 4. Cash Payments Journal 5. General Journal 6. General Ledger 7. Account Rec

sas

sas

'

'

1. Sales Journal

2. Purchases Journal

3. Cash Receipts Journal

4. Cash Payments Journal

5. General Journal

6. General Ledger

7. Account Rec Ledger

8. Account Pay Ledger

9. Employee Earnings

10. Payroll Reg

11. Checkbook

12. Bank Reconciliation

13. Sechedule of Open Accounts

14. Worksheet

15. Income Statement

16. Statement of Owner's Equity

17. Balance Sheet

18. Post Closing Trial Balance

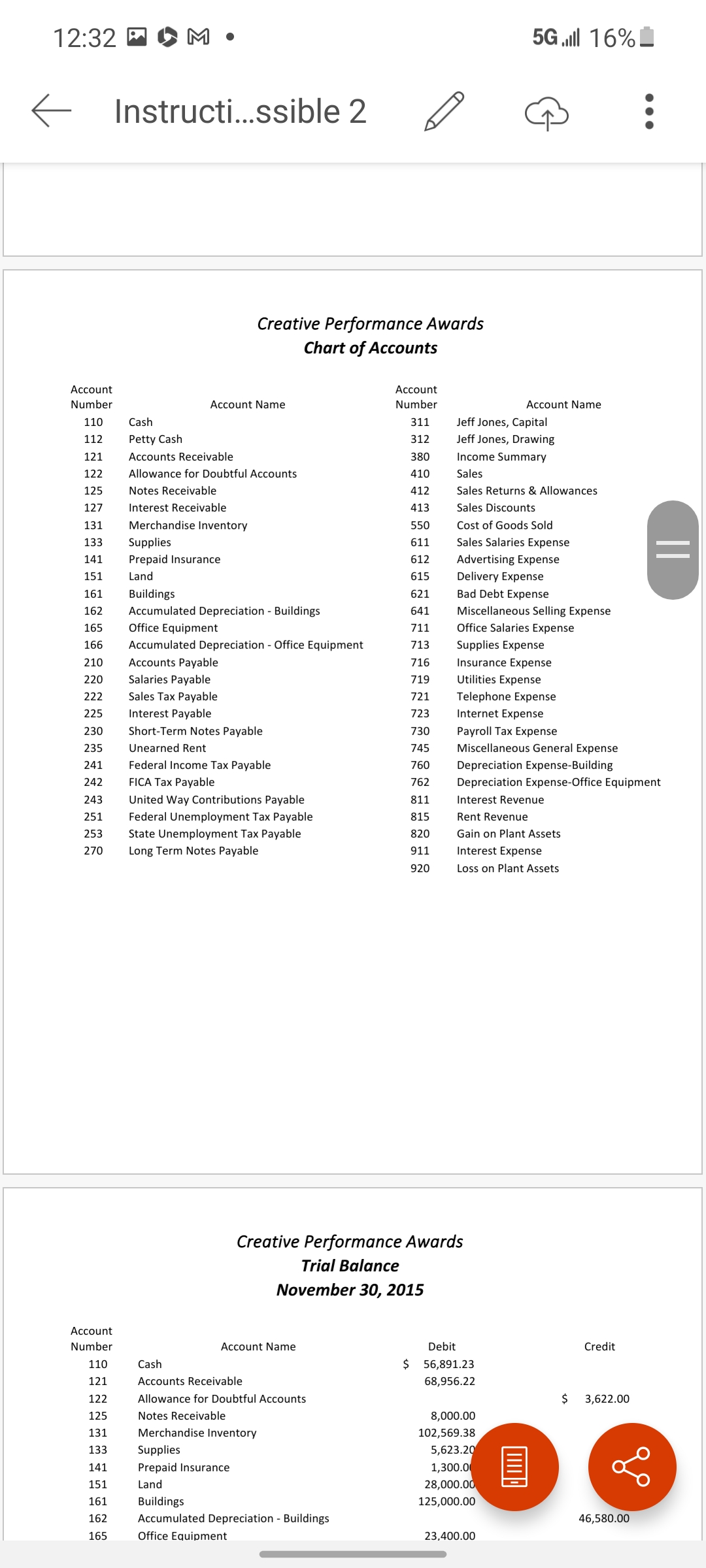

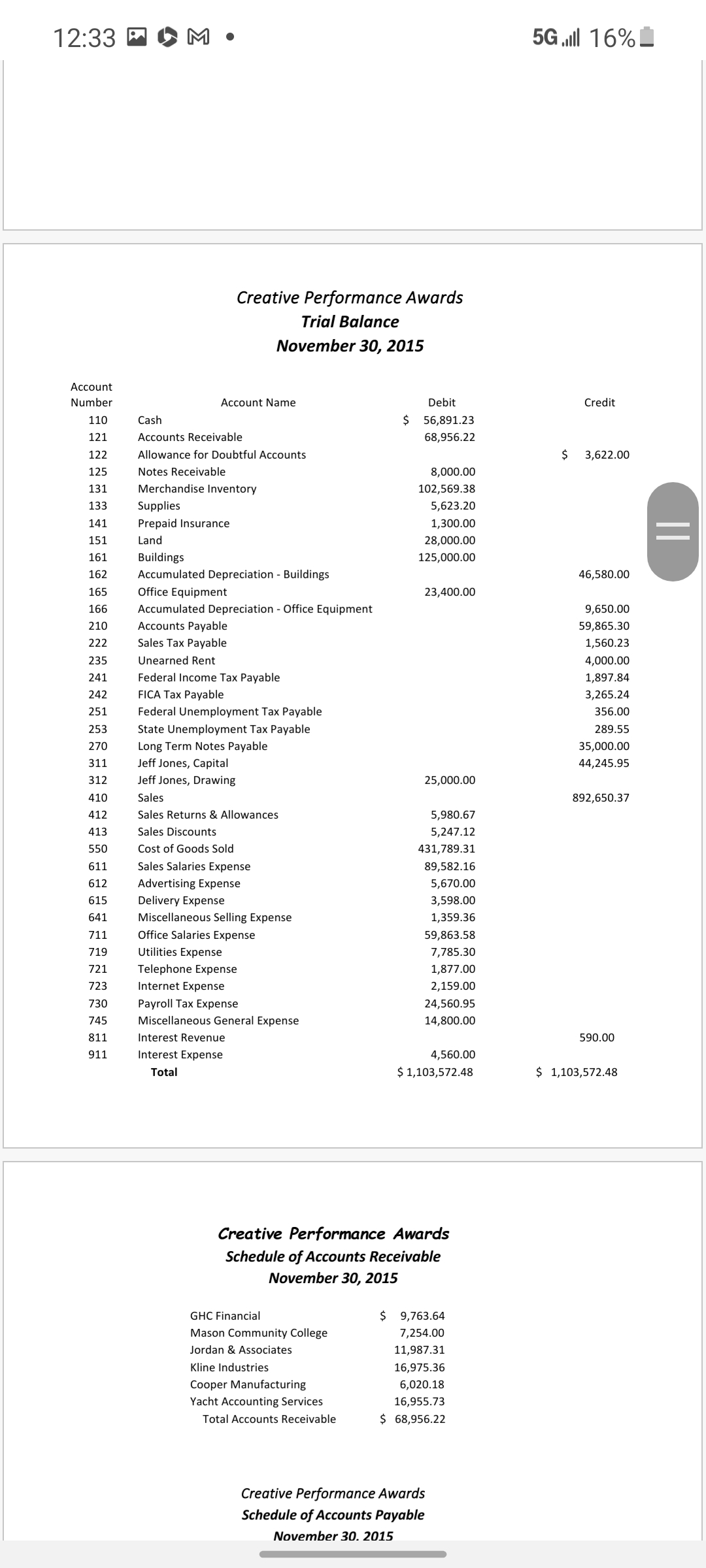

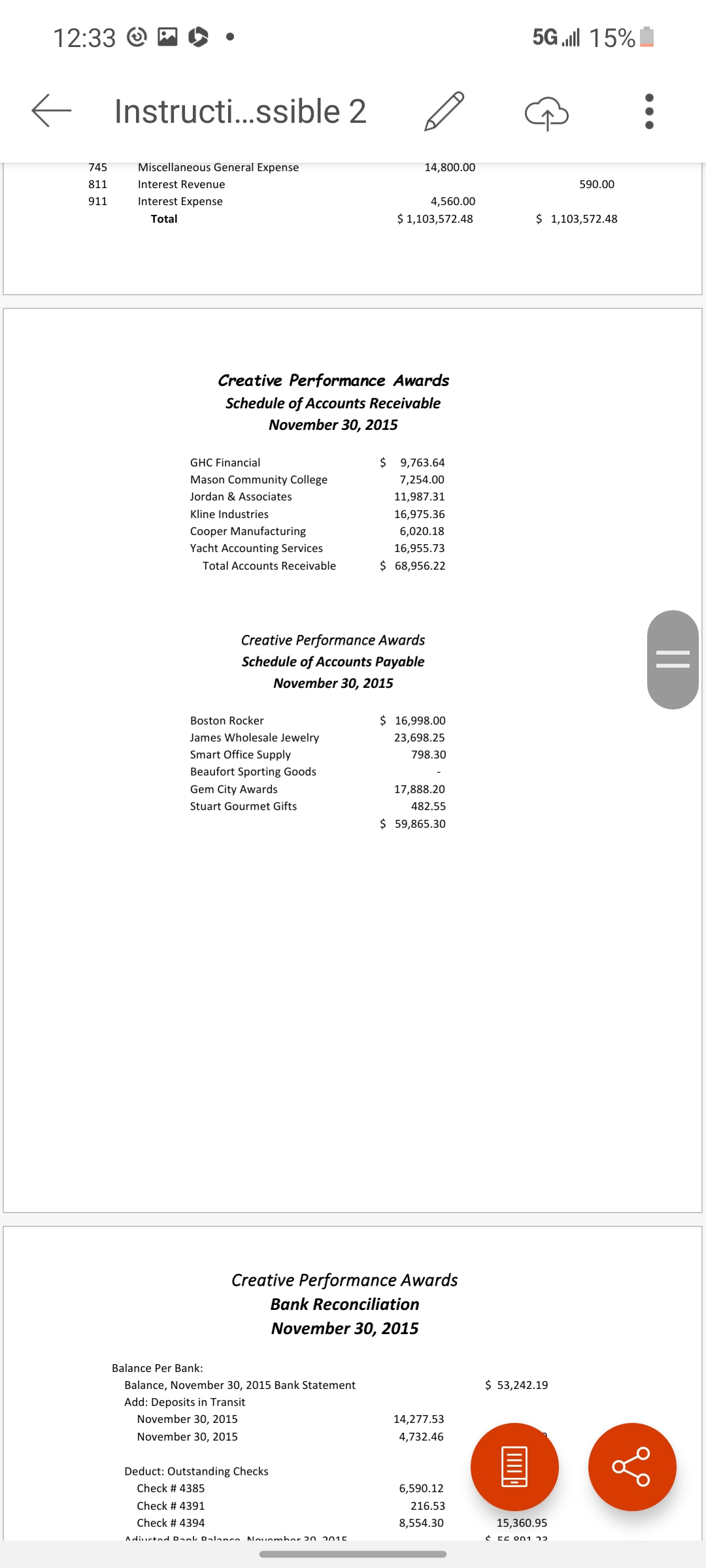

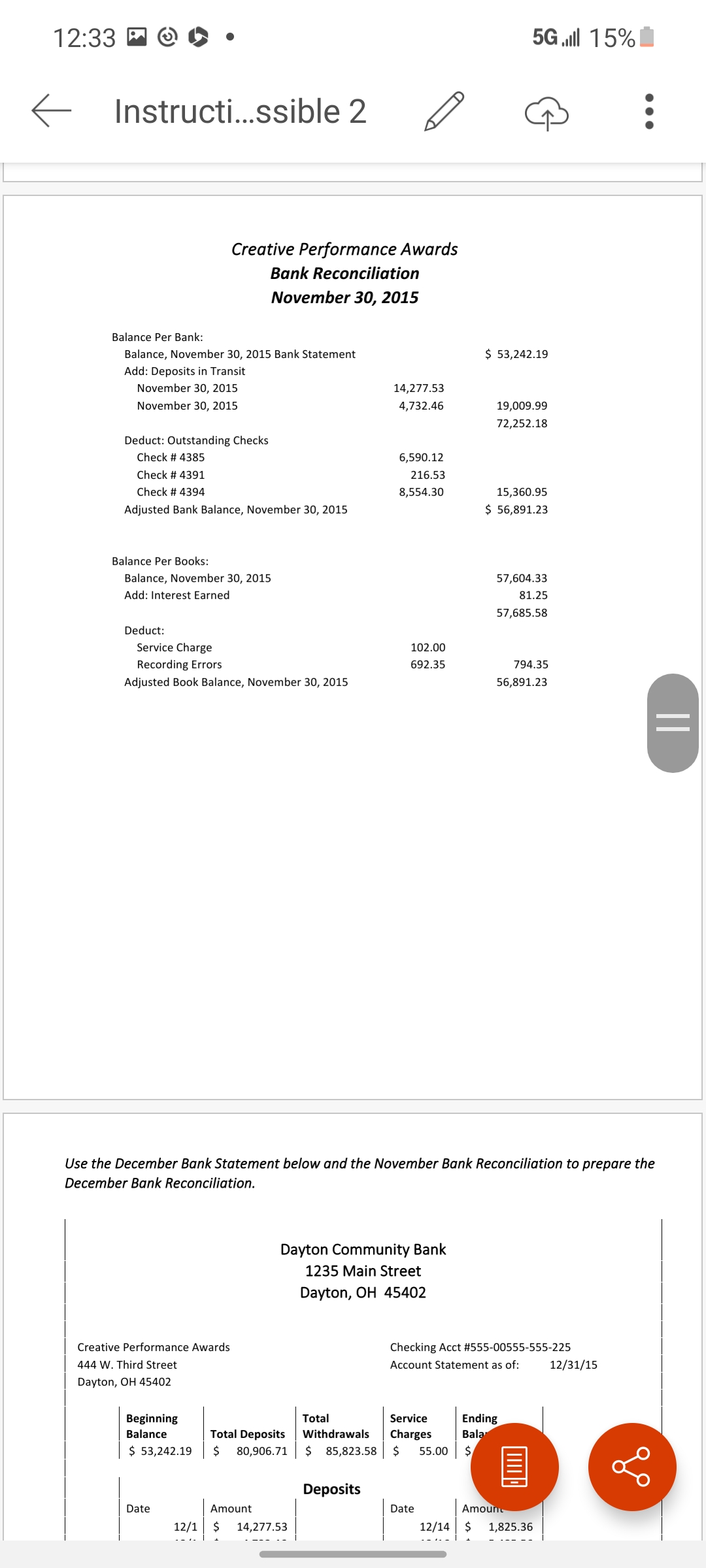

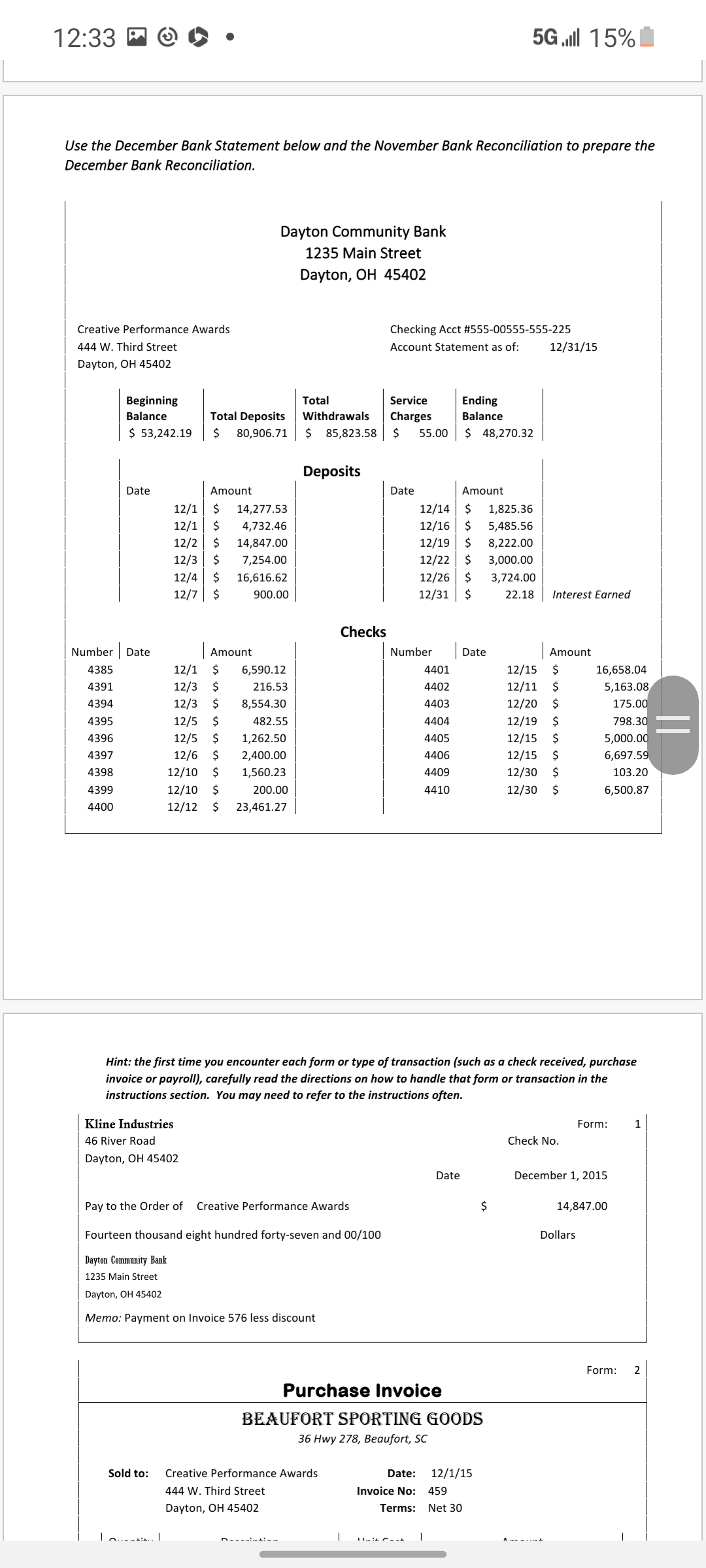

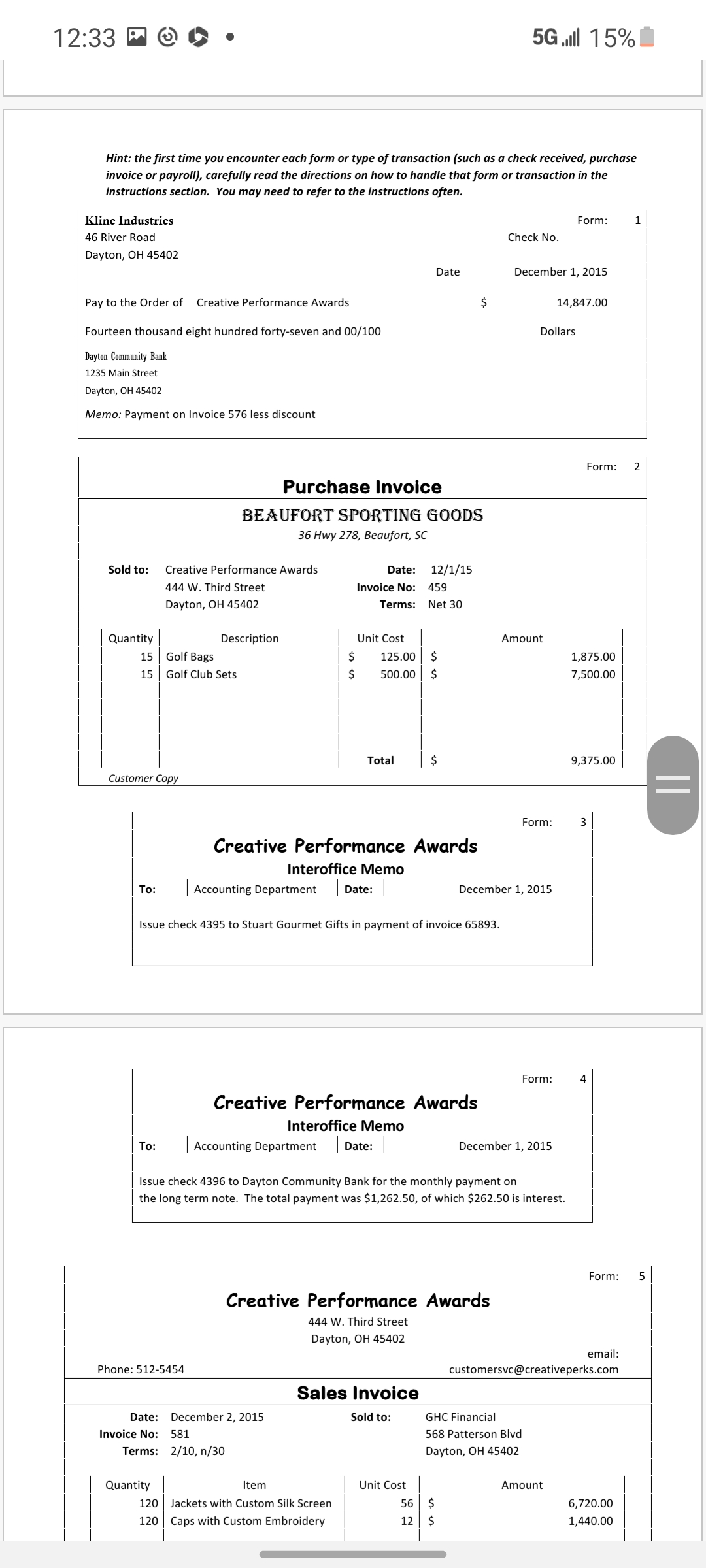

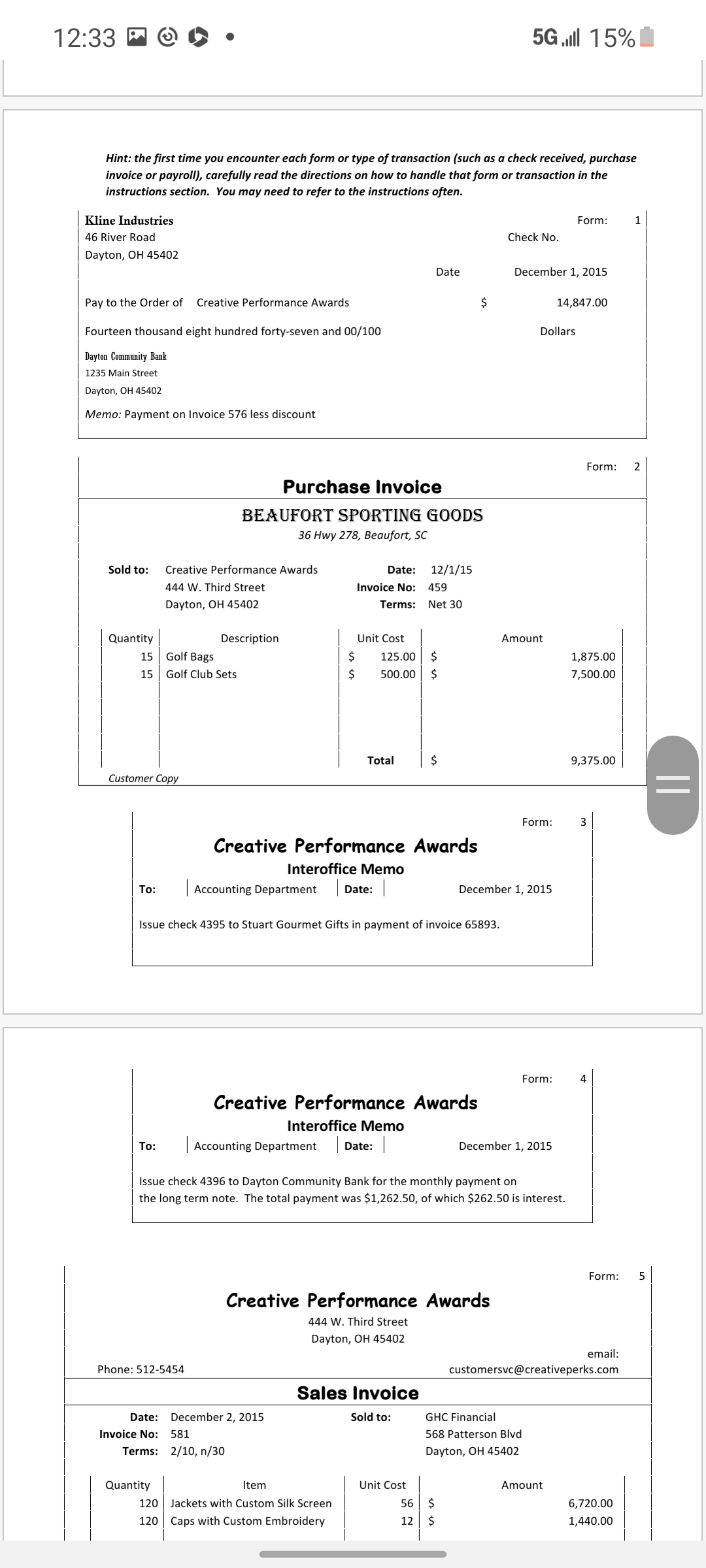

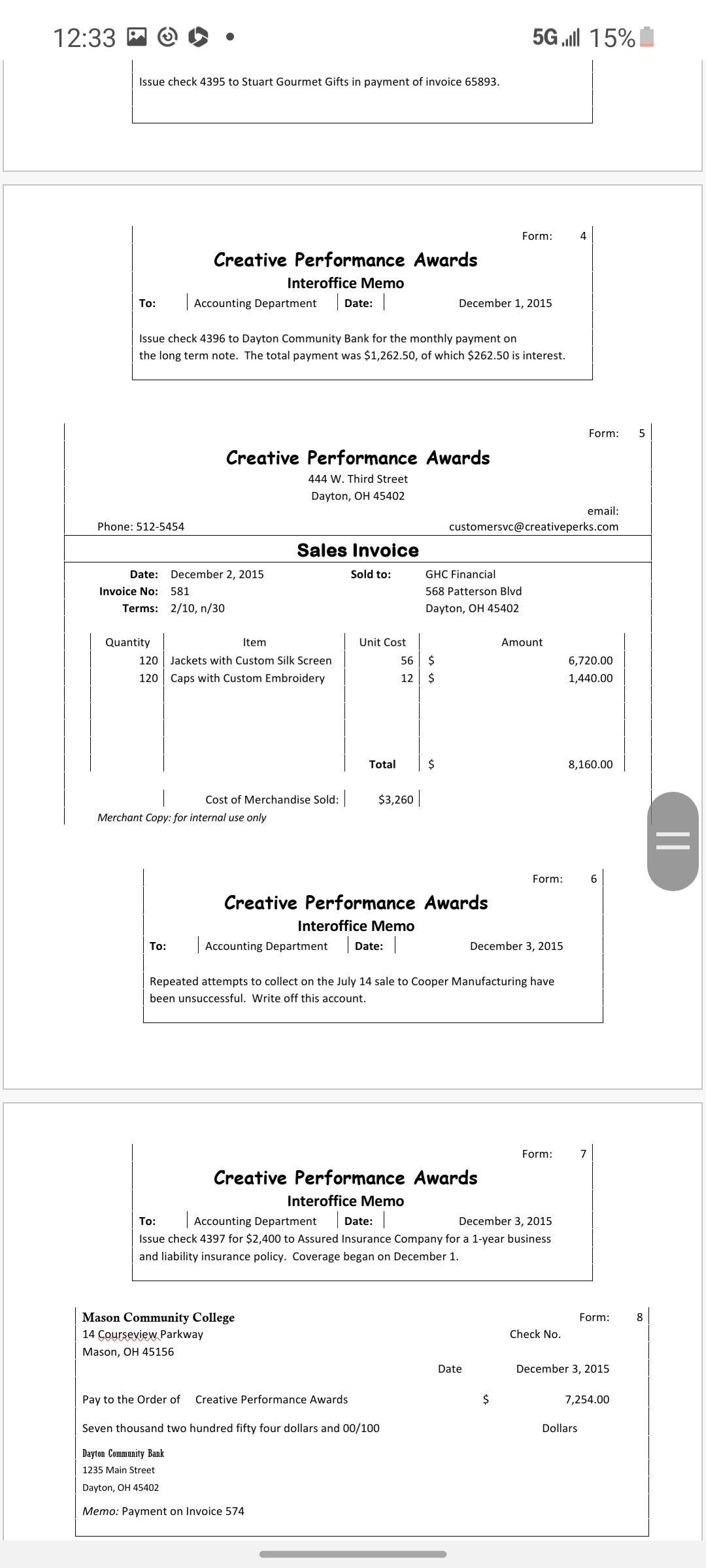

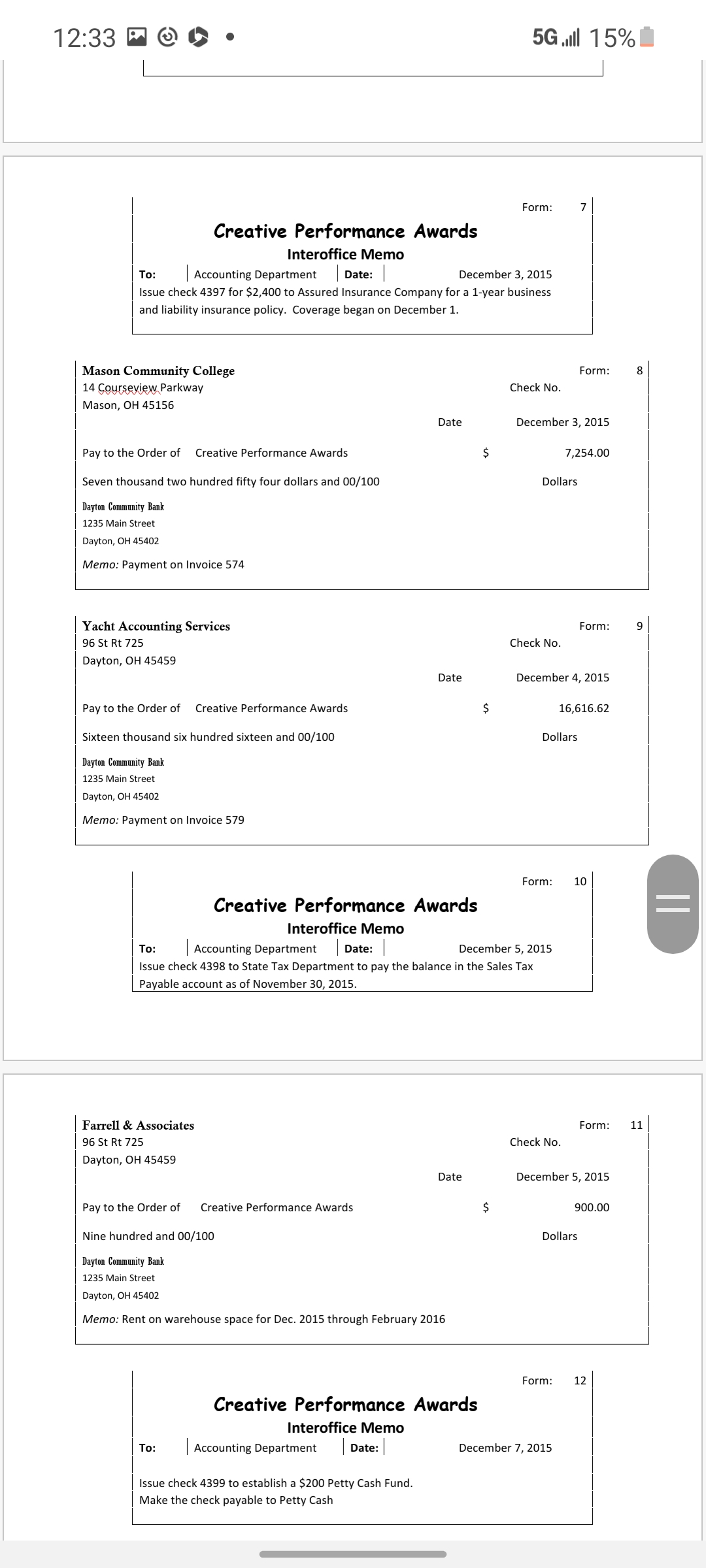

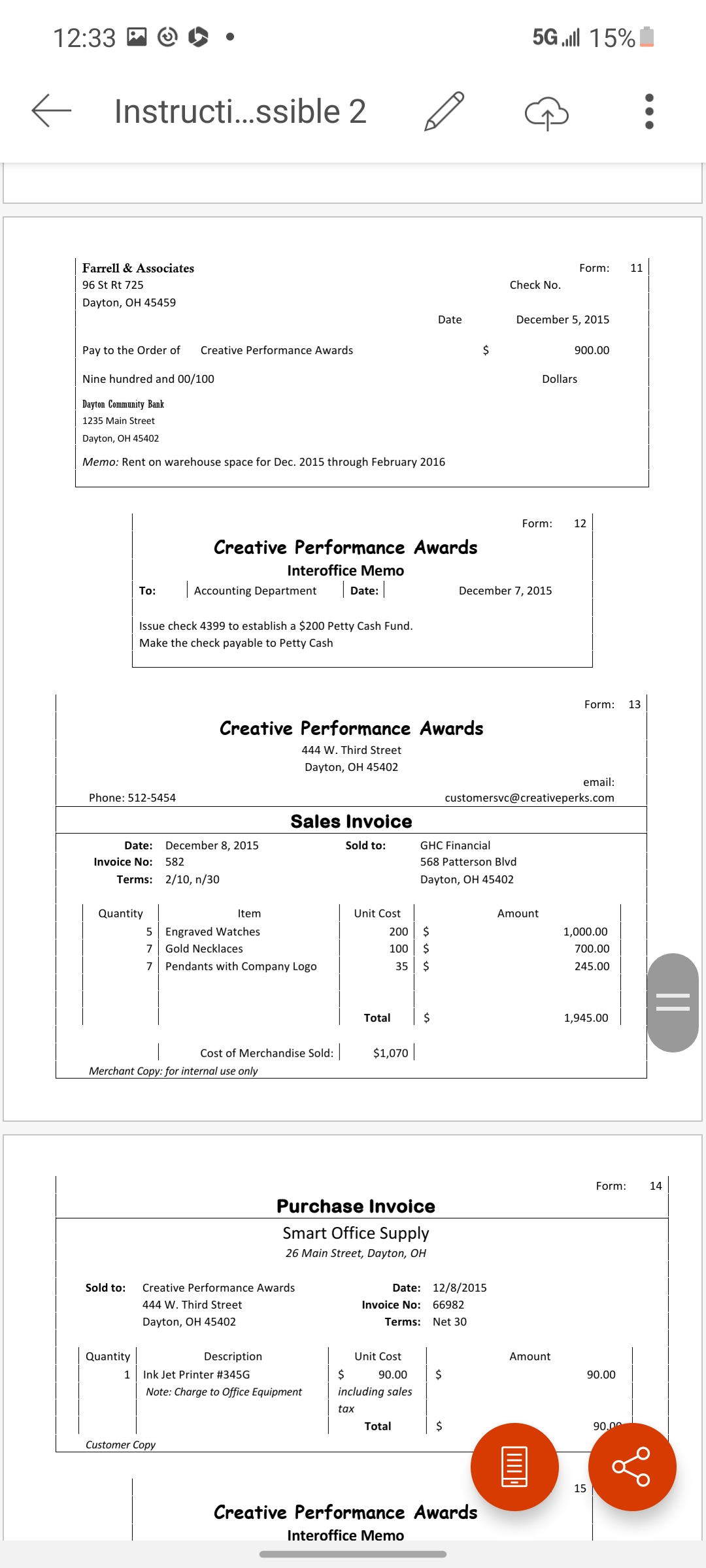

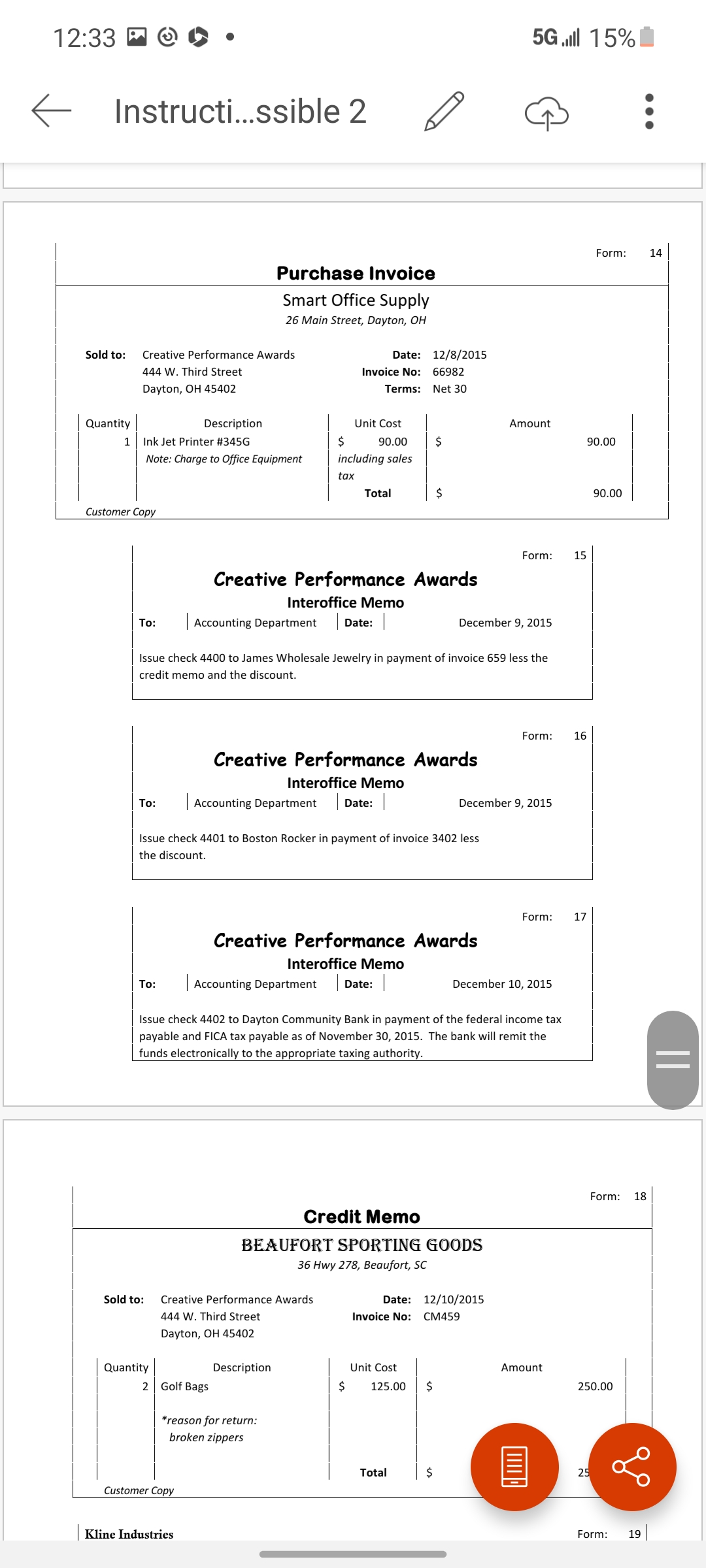

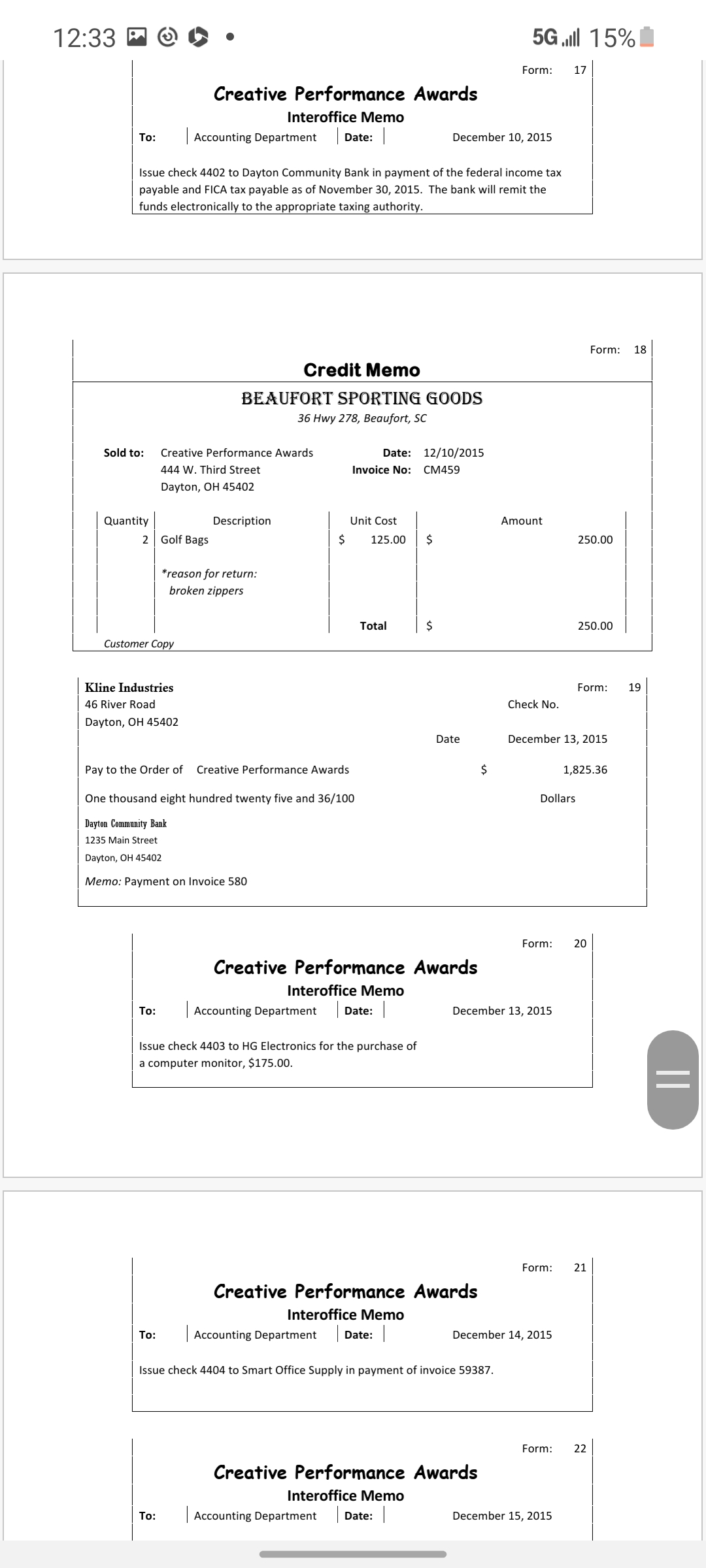

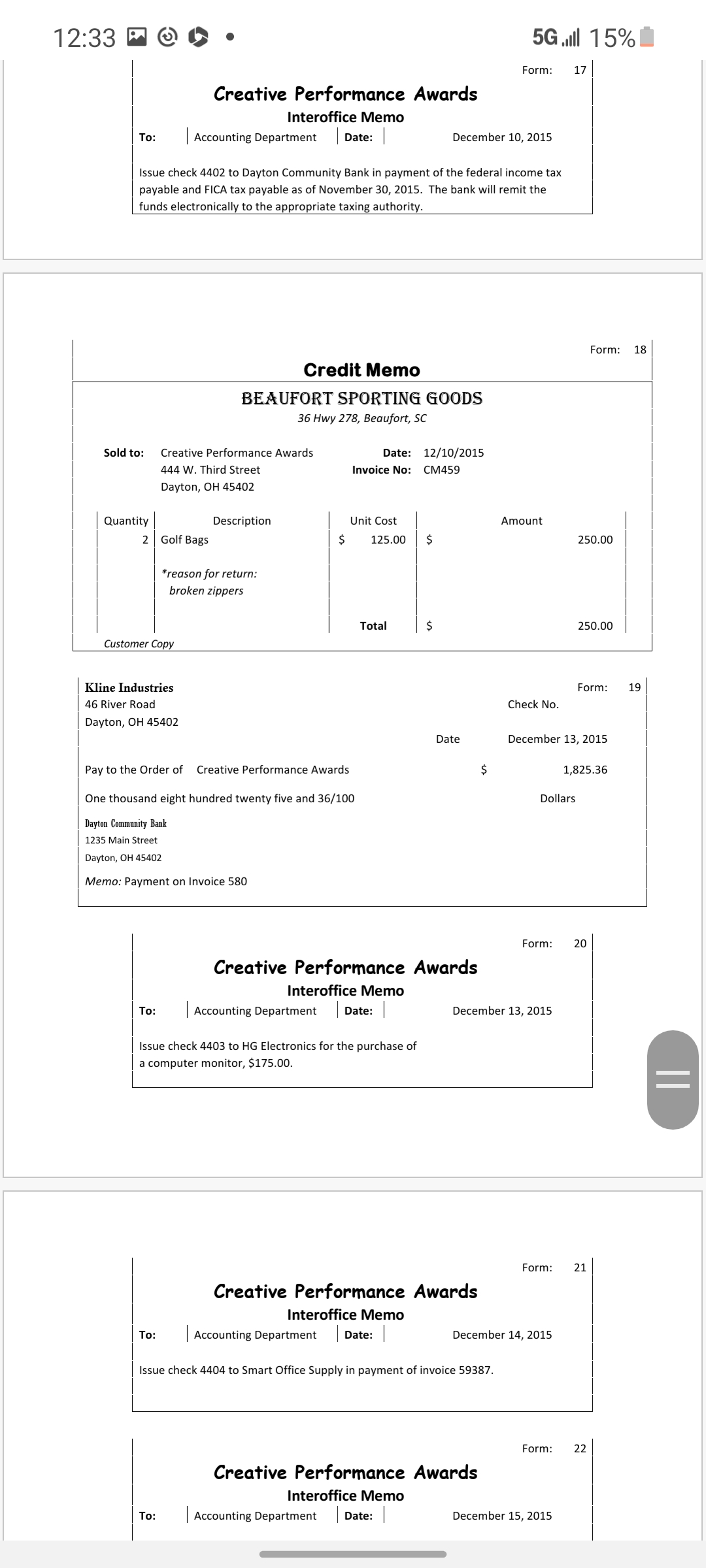

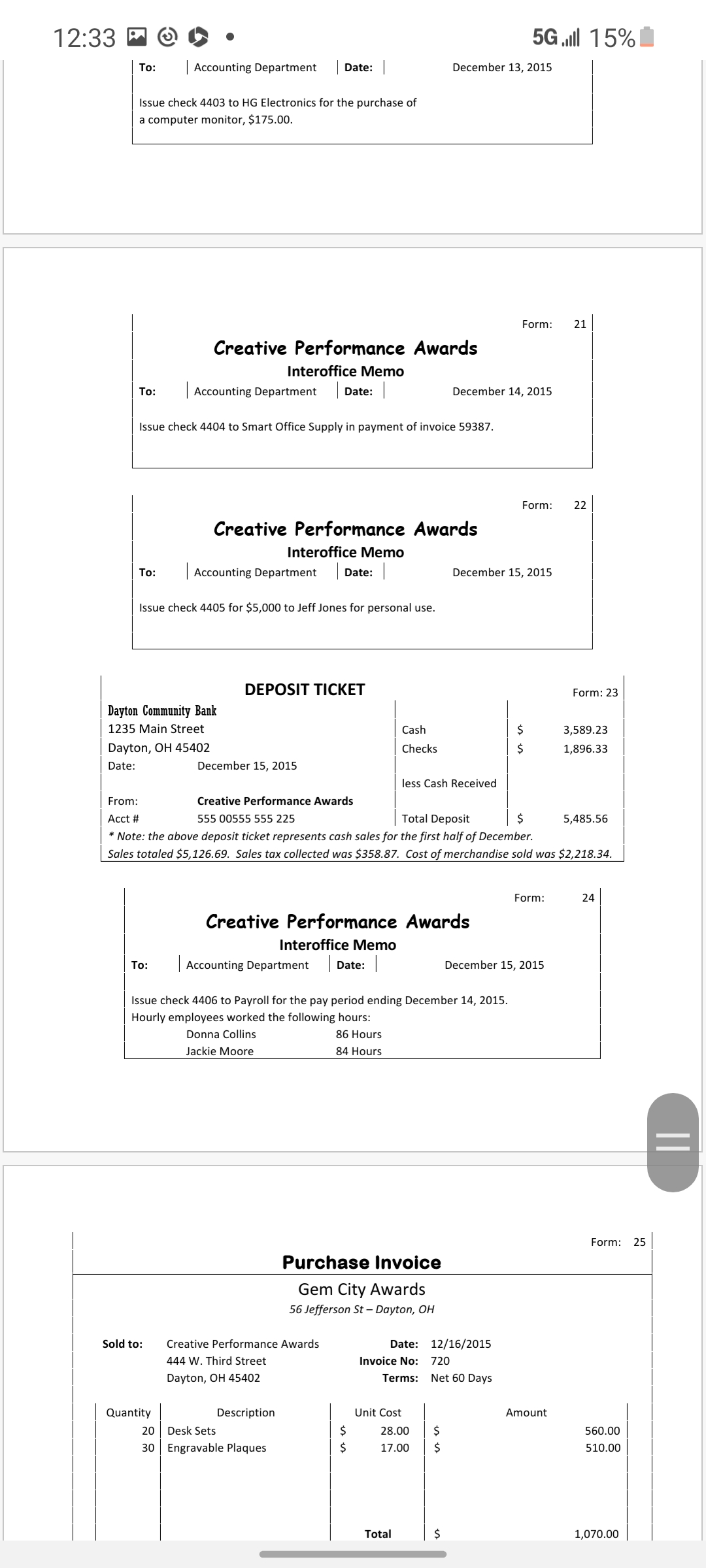

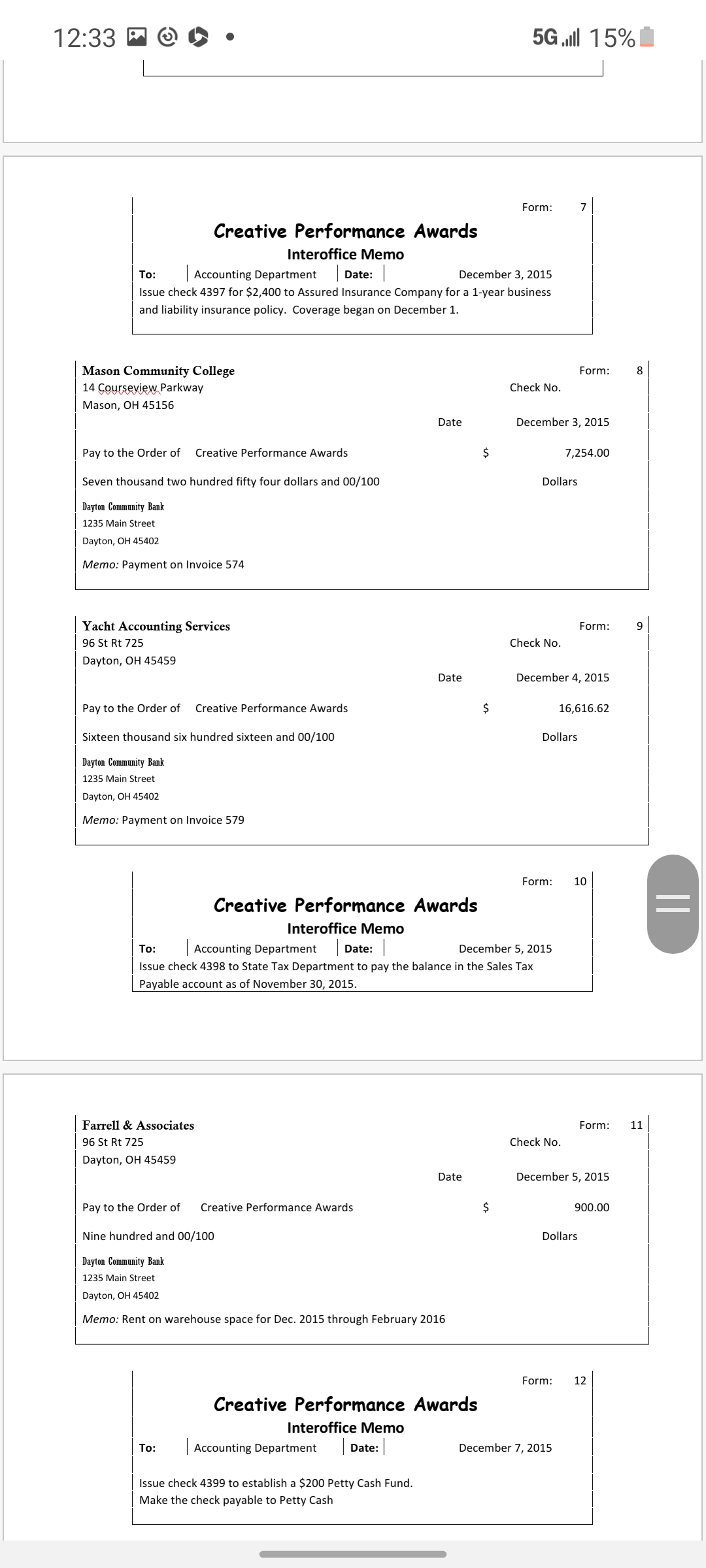

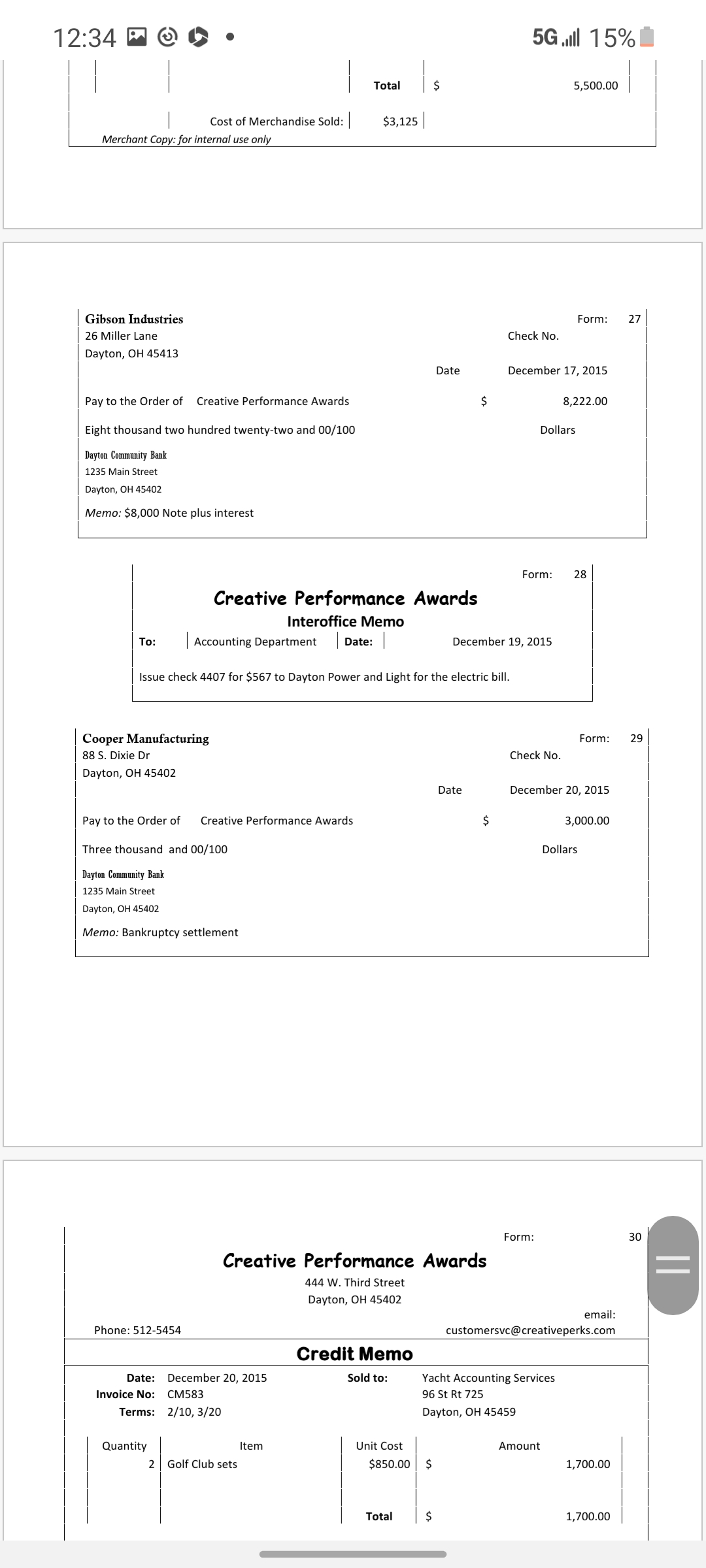

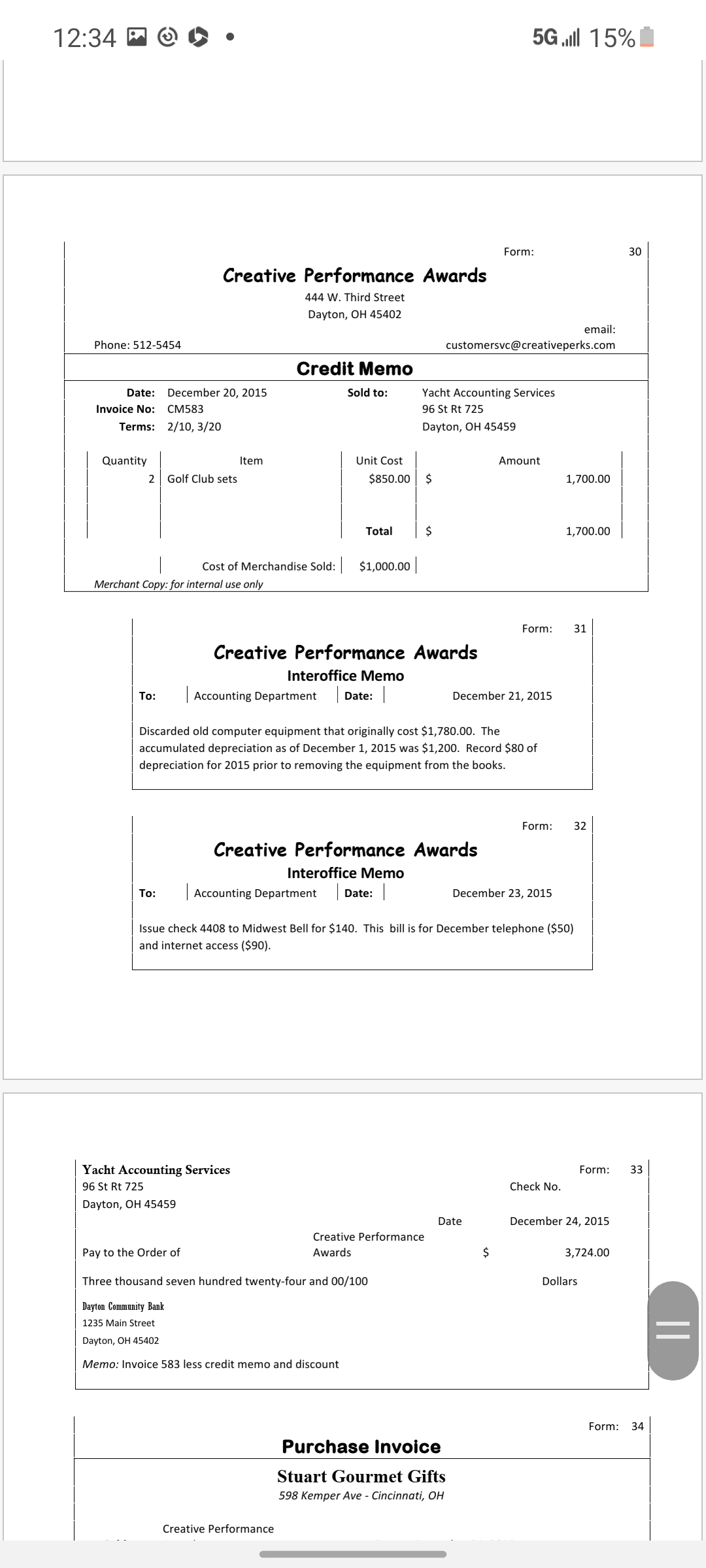

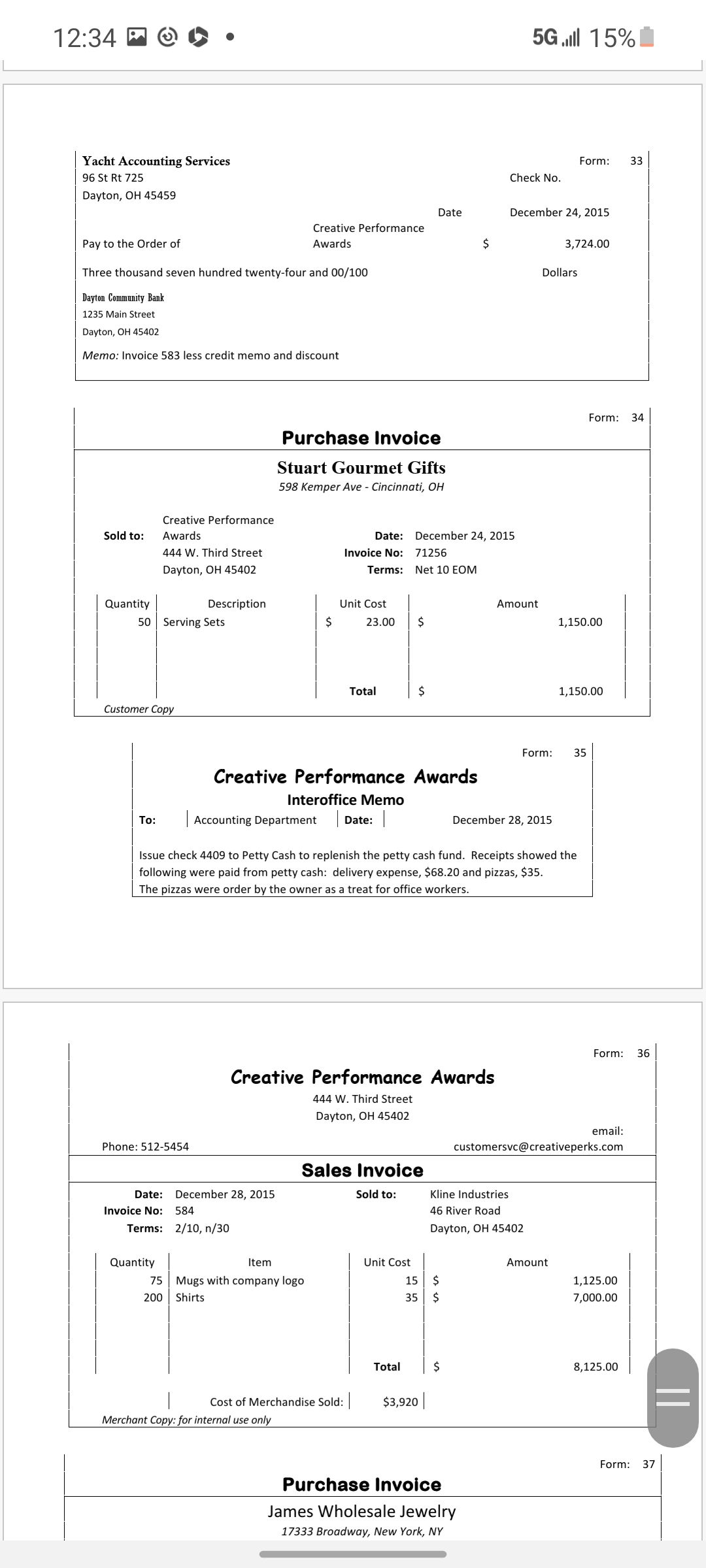

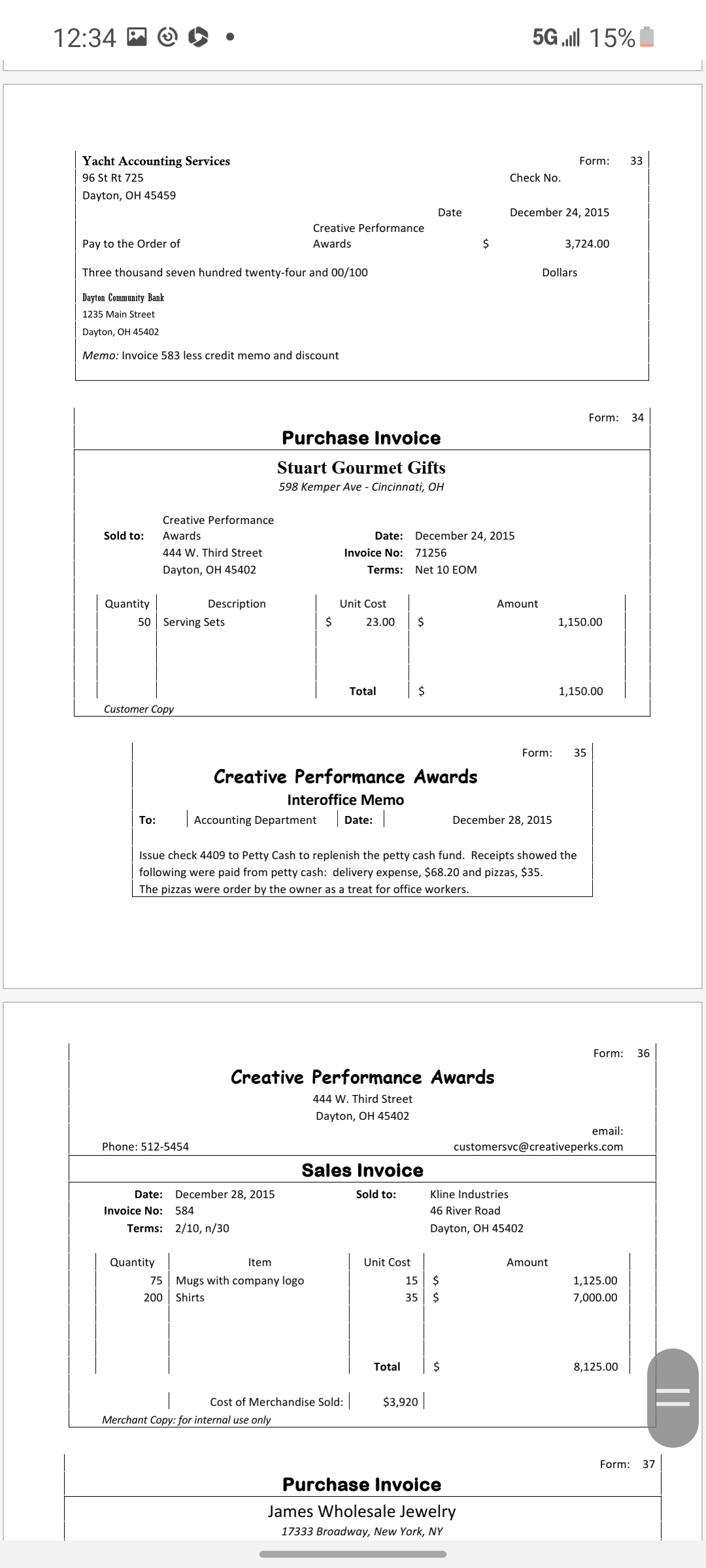

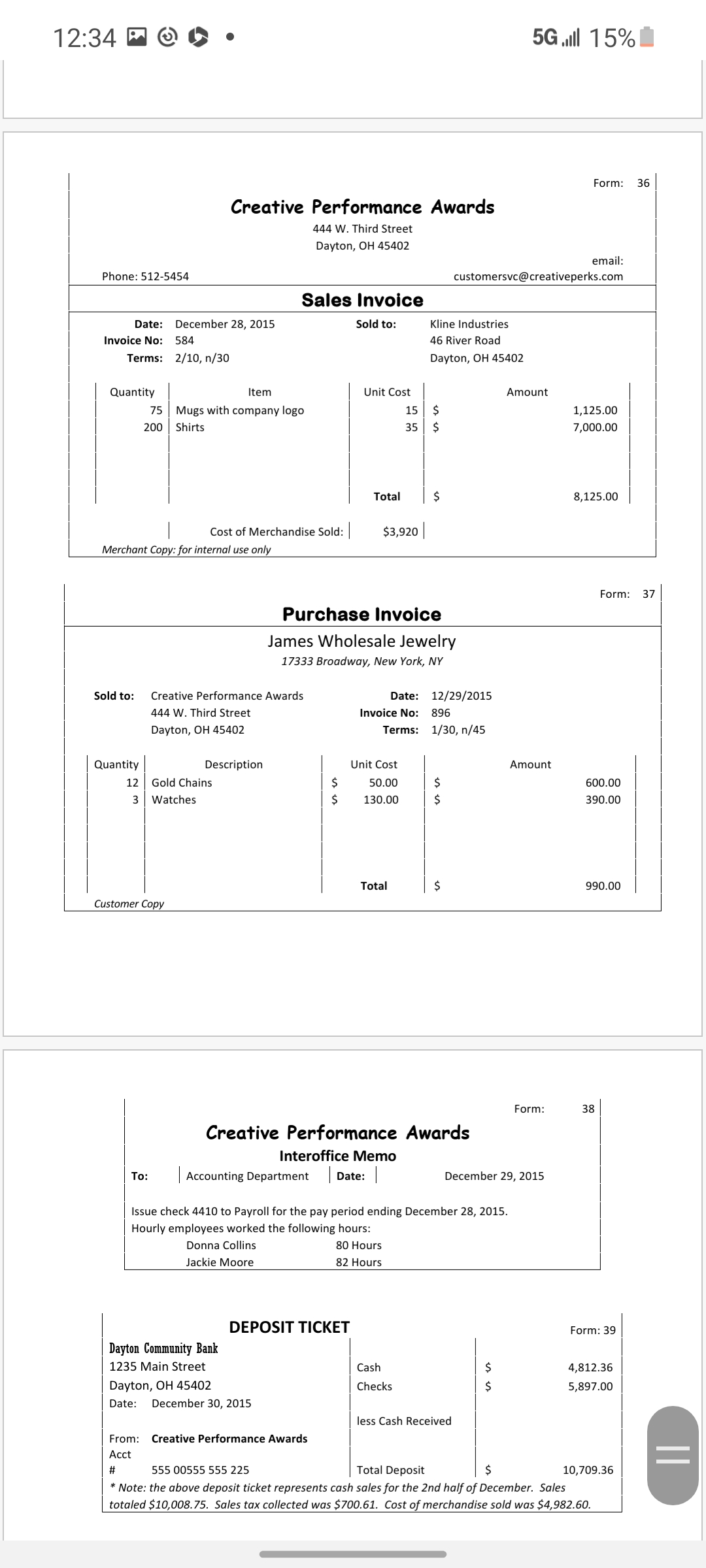

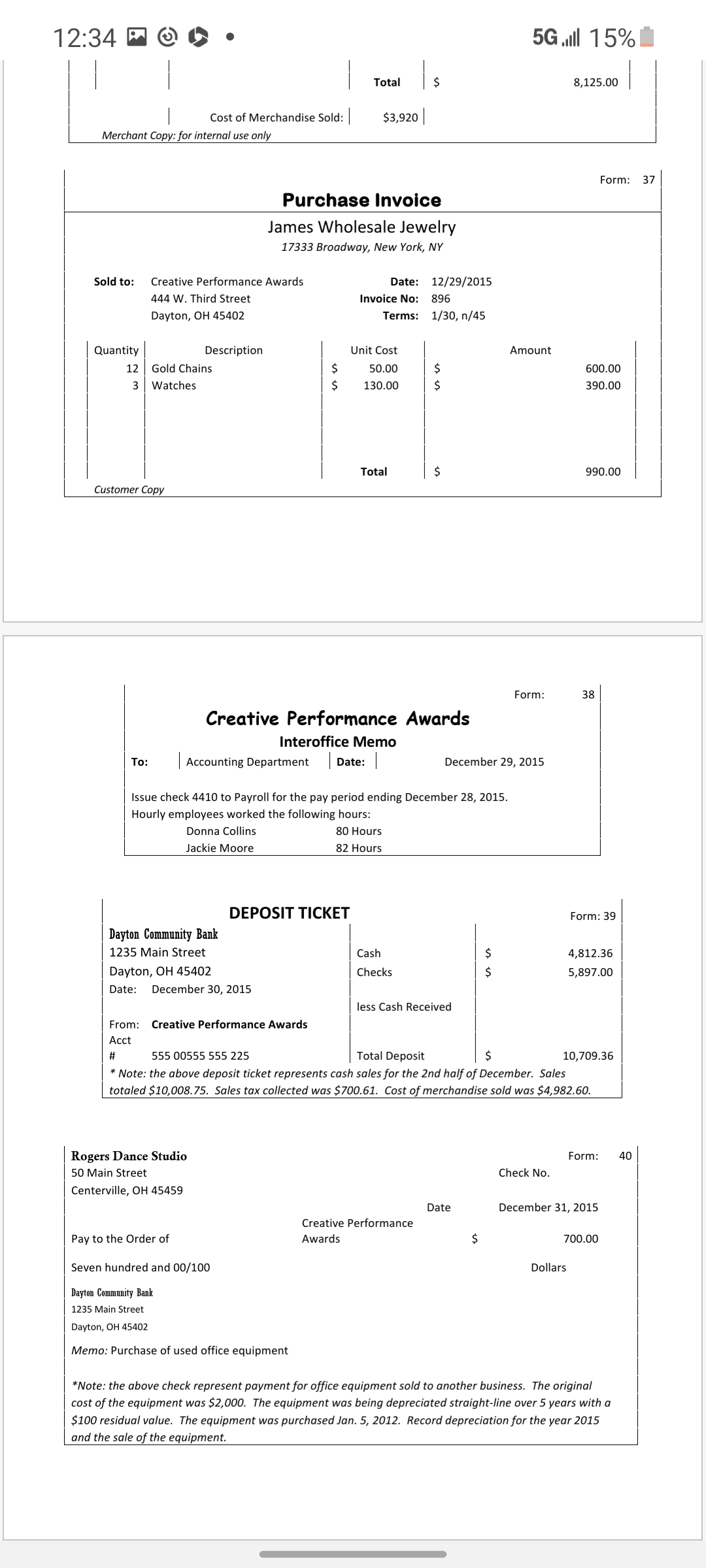

Creative Performance Awards (CPA) Instructions Creative Performance Awards is a small business owned by Jeff Jones. The company sells merchandise that is often customized with company logos or engraving. Companies purchase these goods to reward employees for years of service or meeting company goals. Companies also purchase personalized items to hand out to customers. Creative Performance Awards has a warehouse that is used to store inventory. The warehouse is currently larger than needed, so CPA rents out some of the space to Farrell \& Associates. Assume you are employed as the accountant for this small business. In this assignment, you will complete all of the tasks in the accounting cycle for the month of December 2015. Step 1: Record daily transactions \& post to the subsidiary ledgers to keep track of customer and vendor balances In this step, you will use the following papers: (1) these Instructions, (2) all of your Journals, (3) the Checkbook, (4) the Accounts Receivable and Accounts Payable Subsidiary Ledgers, and (4) Payroll Forms. Provided with this practice set are transaction forms representing CPA's daily transactions for December. Your first step is to record the transactions in the appropriate journals. CPA uses special journals. Special Journals are used to group similar transactions. When Special Journals are used, a transaction is recorded in ONE of the following journals: 1. Sales Journal: Used to record sales ON ACCOUNT. The terms for all sales are 2/10,n/30. 2. Cash Receipts Journal: Used to record any transaction where cash is received. This includes cash sales, collections on accounts receivable, sale of stock to shareholders or owner's contributions. 3. Purchases Journal: Used to record purchases of MERCHANDISE INVENTORY ON ACCOUNT. 4. Cash Payments Journal: Used to record any transaction where cash is paid. This includes cash purchases of inventory or supplies, paying expenses, paying employees, paying dividends, etc. 5. General Journal: used for any transaction that does not fit in a special journal. This includes sales returns or purchase returns on account, adjusting entries, closing entries, reversing entries, correcting entries. It could also include purchases of non-inventory items (supplies, equipment) on account since the Purchases Journal is used just for inventory. Most transactions will be recorded in a Special Journal. As a hint, you should only have about 15 transactions (give or take a few due to how you group entries) in the General Journal from the daily transactions. CPA uses a general ledger and two subsidiary ledgers. Subsidiary ledgers track information about an account in the General Ledger. The subsidiary ledgers you will use are: 1. Accounts Receivable Ledger: Used to keep track of the balances owed to CPA by its customers. 2. Accounts Payable Ledger: Used to keep track of amount CPA owes to its vendors. Any daily transaction that effect Accounts Receivable or Accounts Payable will be immediately posted to the appropriate Customer or Vendor account in the Accounts Receivable or Accounts Payable Ledger. Wait on all postings to the General Ledger until all daily transactions are completed at the end of the month. The following is a list of forms or types of transactions you will record and specific instructions or hints: 1. Sales Invoices: These represent sales on account and they are recorded in the Sales Journal. The customer's name is written in the "Account Debited" column. Because these transactions will increase (debit) Accounts Receivable, you must keep track of who owes for the merchandise. After recording the sale in the Sales Journal, post the amount that will be debited to Accounts Receivable to the specific customer's account in the Accounts Receivable Subsidiary Ledger. Put a V (check mark) in the "Ref" column. The V indicates the amount was posted to the subsidiary ledger. Do not post any amounts to the general ledger until the end of the month. There is no sales tax on business to business transactions recorded in the Sales Journal. 2. Purchase Invoices: These represent purchases on account. If they are for inventory purchases, they are recorded in the Purchases Journal. (Purchases of non-inventory items go in the General Journal). The vendor's name is written in the "Account Creditec transactions will increase (credit) Accounts Payable, you must k amount. After recording the purchase in the Purchases Journal, credited to Accounts Payable to the specific vendor's account in Ledger. Put a V in the "Ref" column to indicate the amount was Do not post any amounts to the general ledger until the end of 1 Any daily transaction that effect Accounts Receivable or Accounts Payable will be immediately posted to the appropriate Customer or Vendor account in the Accounts Receivable or Accounts Payable Ledger. Wait on all postings to the General Ledger until all daily transactions are completed at the end of the month. The following is a list of forms or types of transactions you will record and specific instructions or hints: 1. Sales Invoices: These represent sales on account and they are recorded in the Sales Journal. The customer's name is written in the "Account Debited" column. Because these transactions will increase (debit) Accounts Receivable, you must keep track of who owes for the merchandise. After recording the sale in the Sales Journal, post the amount that will be debited to Accounts Receivable to the specific customer's account in the Accounts Receivable Subsidiary Ledger. Put a V (check mark) in the "Ref" column. The V indicates the amount was posted to the subsidiary ledger. Do not post any amounts to the general ledger until the end of the month. There is no sales tax on business to business transactions recorded in the Sales Journal. 2. Purchase Invoices: These represent purchases on account. If they are for inventory purchases, they are recorded in the Purchases Journal. (Purchases of non-inventory items go in the General Journal). The vendor's name is written in the "Account Credited" column. Because these transactions will increase (credit) Accounts Payable, you must keep track of who CPA owes and the amount. After recording the purchase in the Purchases Journal, post the amount that will be credited to Accounts Payable to the specific vendor's account in the Accounts Payable Subsidiary Ledger. Put a V in the "Ref" column to indicate the amount was posted to the subsidiary ledger. Do not post any amounts to the general ledger until the end of the month. 3. Checks Received: These are checks made payable to Creative Performance Awards. These will be recorded in the Cash Receipts Journal. If the check was received from a customer paying on account, the entry will credit Accounts Receivable. Whenever Accounts Receivable is credited, you need to write the name of the customer in the "Account Credited" column. You also need to post the payment received to the specific customer's account in the Accounts Receivable Subsidiary Ledger and show the posting with a v in the "Ref" column. Sometimes, you may need to credit an account that is not listed in the column headings on the journal. If this occurs, write the amount in the "Other Accounts Cr." Column and write the specific name of the account to be credited (such as Interest Revenue or Unearned Rent, for example) in the "Account Credited" column. CPA needs to always know how much cash is on deposit in the bank. To accomplish this, the cash account balance is tracked on the check stubs in the company's Checkbook. When a check is received, fill in the amount on the "Deposit" line of the next check's stub in the checkbook. This will allow you to subtotal the amount of cash available. (You can assume you will be depositing the check in the bank on the day it is received.) You may have more than one deposit before writing the next check. If so, use the second deposit line on the check stub. 4. Checks Issued (Paid). An interoffice memo is used to notify you that you need to write a check. In addition to writing the check and recording the amount of the check on the stub of the Checkbook, you will need to record the transaction in the Cash Payments Journal. If the check is issued to pay a vendor for items purchased on account, you will need to debit Accounts Payable. Whenever Accounts Payable is debited, you write the name of the vendor in the "Account Debited" column. You also need to post the payment made to the specific vendor's account in the Accounts Payable Subsidiary Ledger and show the posting with a V in the "Ref" column. Sometimes, you may need to debit an account that is not listed in the column headings on the journal. If this occurs, write the amount in the "Other Accounts Dr." Column and write the specific name of the account to be credited (such as Supplies or Utilities Expense, for example) in the "Account Debited" column. 5. Deposit Ticket. The deposit tickets represent deposits made for Cash Sales to customers. While these cash receipts should be deposited daily, to reduce the number of transactions you need to record in this assignment, there will only be 2 deposits tickets. Record the information provided in the Cash Receipts Journal. 6. Payroll. There are several steps required to complete the 2 payroll transactions. a. Fill out the Employee Earnings Record for each employee. There are 4 employees. You will only be given hours worked for 2 employees because the other 2 employees are in salaried positions. (You can enter 80 as the hours worked for each two-week pay period for salaried employees on payroll forms.) Employees that are paid per hour earn time and a half for overtime. The Employee Earnings records show the filing status (married or single) and number of exemptions for each employee. This information will be needed to find the correct federal income tax to be withheld using the tax tables provided in the payroll documents. FICA Tax is withheld at a rate of 7.65% (which includes Medicare) on the first $118,500 each employee earns during a year. Assume the amounts withheld as United Way contributions are the same each pay period. b. When all 4 Employee Earning Records are complete, you need to transfer that data to the Payroll Register to the appropriate week. Total each column in the Payroll Register to 4. Checks Issued (Paid). An interoffice memo is used to notify you that you need to write a check. In addition to writing the check and recording the amount of the check on the stub of the Checkbook, you will need to record the transaction in the Cash Payments Journal. If the check is issued to pay a vendor for items purchased on account, you will need to debit Accounts Payable. Whenever Accounts Payable is debited, you write the name of the vendor in the "Account Debited" column. You also need to post the payment made to the specific vendor's account in the Accounts Payable Subsidiary Ledger and show the posting with a v in the "Ref" column. Sometimes, you may need to debit an account that is not listed in the column headings on the journal. If this occurs, write the amount in the "Other Accounts Dr." Column and write the specific name of the account to be credited (such as Supplies or Utilities Expense, for example) in the "Account Debited" column. 5. Deposit Ticket. The deposit tickets represent deposits made for Cash Sales to customers. While these cash receipts should be deposited daily, to reduce the number of transactions you need to record in this assignment, there will only be 2 deposits tickets. Record the information provided in the Cash Receipts Journal. 6. Payroll. There are several steps required to complete the 2 payroll transactions. a. Fill out the Employee Earnings Record for each employee. There are 4 employees. You will only be given hours worked for 2 employees because the other 2 employees are in salaried positions. (You can enter 80 as the hours worked for each two-week pay period for salaried employees on payroll forms.) Employees that are paid per hour earn time and a half for overtime. The Employee Earnings records show the filing status (married or single) and number of exemptions for each employee. This information will be needed to find the correct federal income tax to be withheld using the tax tables provided in the payroll documents. FICA Tax is withheld at a rate of 7.65% (which includes Medicare) on the first $118,500 each employee earns during a year. Assume the amounts withheld as United Way contributions are the same each pay period. b. When all 4 Employee Earning Records are complete, you need to transfer that data to the Payroll Register to the appropriate week. Total each column in the Payroll Register to provide the information for the payroll journal entry. Use Gross Pay when completing the Office and Sales Salaries Expense columns. c. Record the information from the Payroll Register in the General Journal. d. Write a check to "Payroll" for the total amount of payroll checks to be distributed. This check will transfer from the company's regular checking account to the payroll checking account exactly the amount of the employee paychecks. You do not need to write checks to each employee. Assume that is completed via direct deposits. Record the amount of the check for the total payroll in the Cash Disbursements Journal. e. Prepare an entry in the General Journal to record the company's payroll taxes for the pay period. The employer is required to match the employees' FICA tax withheld. The employer also pays Federal and State Unemployment taxes (FUTA and SUTA). The rate is 4.1% for State Unemployment tax (SUTA) and 0.8% for Federal Unemployment tax (FUTA). Unemployment taxes are paid only on the first $7,000 each employee earns in a calendar year. 7. Credit Memos. You will encounter credit memos received from vendors for purchase returns and credit memos issued to customer for sales returns. Credit memos will be recorded in the General Journal. Post the return amount to the appropriate account in the Accounts Payable Ledger or Accounts Receivable Ledger. Wait to the post to the general ledger until the end of the month. 8. Hints regarding Special Journals. a. Some of the Special Journals have an "Other Accounts" column. That column will state if the "Other Accounts" will be debited or credited. For example, in the Cash Receipts journal, there is a column labeled "Other Accounts Credit." If you need to record an entry that Debits an account not listed as a column heading, you can enter that number as a negative amount in the Other Accounts Credited column. b. An entry in a special journal may require more than one line. For example, let's say you need to credit 2 Other Accounts in a Cash Payments Journal. List each account and amount in the "Other Accounts" column. You can put the total Cash paid on one of the lines. Step 2: Post daily transactions to the General Ledger. In this step, you will use the following papers: (1) these Instructions, (2) all of your Journals, (3) the General Ledger accounts. After entering all of the transaction forms as journal entries, you will need to post these entries to the General Ledger. 1. Posting Special Journals to the General Ledger a. First add each column in the special journal. (This is called "footing" the journal.) Next, add the debit column totals and make sure they equal the total of the credit totals. (This is called "cross-footing.") If total debits = total credits, you need to find and correct errors before posting. b. Once you know the special journal balances, you are ready to post to the General Ledger. For any column where all of the entries go to one account (such as a column heading that says "Cash Dr."), post the column total to the account. For example, in the Cash Receipt Journals, post the total of the "Cash Dr." column to the Cash Account in the General Ledger as a debit. Do not post the individual amounts in the "Cash Dr." column; just post the column total. This saves you a lot of time! After you post the column total, write the account number under the total. For example, write "110" under the "Cash Dr." column total in the Cash Receipts Journal once the column total is posted. c. Some column totals will need to be posted to 2 accounts if that is indicated in the column heading. For example, the Purchases Journal column needs to be posted to Merchandise Inventory as a debit and Accounts Payable as a credit. d. The amounts in the "Other Accounts" column of a special journal must be posted individually. As you post each number in the "Other Accounts" column, write that account number in the "Ref" column. These means the "Ref" column will have a r for all items posted to a subsidiary ledger (Accounts Receivable or Accounts Payable) and an account number for all items posted to the general ledger from the "Other Accounts" column. 2. Posting the General Journal to the General Ledger. a. Each debit and credit entry in the General Journal must be posted to the appropriate account in the General Ledger. As you post each amount, write the account number in the "Post Ref" column. b. Entries to Accounts Receivable or Accounts Payable should have already been posted to the subsidiary ledgers and should already have a in the "Post Ref" column. These entries also need to be posted to Accounts Receivable or Accounts Payable in the General Ledger. As you post to the General Ledger, also put the account number in the "Post Ref" box (account \# 121 for Accounts Receivable and \#210 for Accounts Payable). Here is an example of the "Post Ref" box for an entry to Accounts Receivable in the General Journal (showing the dual posting to the Subsidiary Ledger and the General Ledger). As a hint to know if you are doing the posting correctly, when you have finished step 2 you should have just 2 or 3 postings to the Cash account. There should be about 5 postings to Accounts Receivable. Step 3: Prepare the bank reconciliation for December and resulting entries. Make sure the balance in the Cash account in the general ledger is equal to balance of Cash in your checkbook. If these do not match, you need to find and correct errors in your cash account or checkbook. When the cash balances match, you need to complete the December bank reconciliation. You will need to use the December Bank Statement and the November Bank Reconciliation. individually. As you post each number in the "Other Accounts" column, write that account number in the "Ref" column. These means the "Ref" column will have a for all items posted to a subsidiary ledger (Accounts Receivable or Accounts Payable) and an account number for all items posted to the general ledger from the "Other Accounts" column. 2. Posting the General Journal to the General Ledger. a. Each debit and credit entry in the General Journal must be posted to the appropriate account in the General Ledger. As you post each amount, write the account number in th "Post Ref" column. b. Entries to Accounts Receivable or Accounts Payable should have already been posted to the subsidiary ledgers and should already have a in the "Post Ref" column. These entries also need to be posted to Accounts Receivable or Accounts Payable in the General Ledger. As you post to the General Ledger, also put the account number in the "Post Ref" box (account \# 121 for Accounts Receivable and \#210 for Accounts Payable). Here is an example of the "Post Ref" box for an entry to Accounts Receivable in the General Journal (showing the dual posting to the Subsidiary Ledger and the General Ledger). As a hint to know if you are doing the posting correctly, when you have finished step 2 you should have just 2 or 3 postings to the Cash account. There should be about 5 postings to Accounts Receivable. Step 3: Prepare the bank reconciliation for December and resulting entries. Make sure the balance in the Cash account in the general ledger is equal to balance of Cash in your checkbook. If these do not match, you need to find and correct errors in your cash account or checkbook. When the cash balances match, you need to complete the December bank reconciliation. You will need to use the December Bank Statement and the November Bank Reconciliation. After the General Ledger cash balance has been reconciled to the Bank Statement, journalize any necessary entries in the General Journal. Also post these entries to the General Ledger and record the amounts in the checkbook. Bank service charges are recorded as a Miscellaneous General Expense. Step 4: Prepare the Schedule of Accounts Receivable and Accounts Payable On the Schedule of Accounts Receivable form, list all of your customers and the balance owed to CPA. Total the customer balances. This amount must match the balance of Accounts Receivable in the General Ledger. If not, you will need to find and correct errors. Repeat the same process for the vendors on the Accounts Payable form and verify the total matches Accounts Payable in the General Ledger. Step 5: Prepare the Worksheet Enter the balances from the General Ledger in Trial Balance columns of the worksheet. Enter the adjusting entries based on the information below and then complete the worksheet. 1. Accrued salaries on December 31 are $280 for Office employees and $500 for Sales employees. 2. Supplies on hand on Dec. 31 were $1,370. 3. Insurance policies which have not expired at the end of the year total $2,200. 4. The end of year physical inventory count showed that there is $94,927 of inventory on hand. 5. The annual depreciation that needs to be recorded on Office Equipment is $2,180. 6. The annual depreciation that needs to be recorded on the Building is $4,600. 7. The company estimates that $900 of the accounts receivable balance as of Dec. 31 will not be collected. 8. Unearned rent revenue that has been earned as of Dec. 31 is $4,300. 9. Interest accrued on the long-term note during December is $260. Step 5: Prepare the Worksheet Enter the balances from the General Ledger in Trial Balance columns of the worksheet. Enter the adjusting entries based on the information below and then complete the worksheet. 1. Accrued salaries on December 31 are $280 for Office employees and $500 for Sales employees. 2. Supplies on hand on Dec. 31 were $1,370. 3. Insurance policies which have not expired at the end of the year total $2,200. 4. The end of year physical inventory count showed that there is $94,927 of inventory on hand. 5. The annual depreciation that needs to be recorded on Office Equipment is $2,180. 6. The annual depreciation that needs to be recorded on the Building is $4,600. 7. The company estimates that $900 of the accounts receivable balance as of Dec. 31 will not be collected. 8. Unearned rent revenue that has been earned as of Dec. 31 is $4,300. 9. Interest accrued on the long-term note during December is $260. Step 6: Prepare the Financial Statements Based on the information from the worksheet, prepare the following financial statements. 1. Multiple Step Income Statement 2. Statement of Owner's Equity 3. Classified Balance Sheet Step 7: Journalize and Post the Adjusting Entries. The adjusting entries recorded on the worksheet need to be recorded in the general journal and posted to the general ledger. Step 8: Journalize and Post the Closing Entries Step 9: Prepare a Post-Closing Trial Balance Step 10: Journalize and Post Reversing Entries. Following the policy we used in this class when covering Chapter 3 , record and post reversing entries for the appropriate adjusting entries. Creative Performance Awards Creative Performance Awards Chart of Accounts Creative Performance A wards Creative Performance Awards Schedule of Accounts Receivable November 30, 2015 Creative Performance Awards Schedule of Accounts Receivable November 30, 2015 Creative Performance Awards Schedule of Accounts Payable November 30, 2015 Creative Performance Awards Bank Reconciliation November 30, 2015 Creative Performance Awards Bank Reconciliation November 30, 2015 Use the December Bank Statement below and the November Bank Reconciliation to prepare the December Bank Reconciliation. Use the December Bank Statement below and the November Bank Reconciliation to prepare the December Bank Reconciliation. Dayton Community Bank 1235MainStreet Hint: the first time you encounter each form or type of transaction (such as a check received, purchase invoice or payroll), carefully read the directions on how to handle that form or transaction in the instructions section. You may need to refer to the instructions often. Hint: the first time you encounter each form or type of transaction (such as a check received, purchase invoice or payroll), carefully read the directions on how to handle that form or transaction in the instructions section. You may need to refer to the instructions often. Hint: the first time you encounter each form or type of transaction (such as a check received, purchase invoice or payroll), carefully read the directions on how to handle that form or transaction in the instructions section. You may need to refer to the instructions often. Issue check 4395 to Stuart Gourmet Gifts in payment of invoice 65893. Creative Performance Awards 444 W. Third Street Dayton, OH45402 5125454 customersvc@creativeperks Form: Creative Performance Awards Interoffice Memo To: Accounting Department Date: December 3, 2015 Repeated attempts to collect on the July 14 sale to Cooper Manufacturing have been unsuccessful. Write off this account. Form: 7 Creative Performance Awards Interoffice Memo To: Accounting Department Date: December 3, 2015 Issue check 4397 for $2,400 to Assured Insurance Company for a 1 -year business and liability insurance policy. Coverage began on December 1 . Creative Performance Awards Interoffice Memo To: | Accounting Department | Date: | December 3, 2015 Issue check 4397 for $2,400 to Assured Insurance Company for a 1 -year business and liability insurance policy. Coverage began on December 1. Accounting Services 725 Check No. n,OH45459 the Order of Creative Performance Awards n thousand six hundred sixteen and 00/100 Dollars nmunity Bank ain Street OH45402 Payment on Invoice 579 Creative Performance Awards Interoffice Memo To: | Accounting Department | Date: | December 5, 2015 Issue check 4398 to State Tax Department to pay the balance in the Sales Tax Payable account as of November 30, 2015. Creative Performance Awards Interoffice Memo To: Accounting Department Date: December 7, 2015 Issue check 4399 to establish a $200 Petty Cash Fund. Make the check payable to Petty Cash Creative Performance Awards 444W. Third Street Dayton, OH 45402 12:33 (0) 5G, 15%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts