Question: Sato Awards has had a request for a special order of 10 silver-plated trophies from the provincial tennis association. The normal selling price of such

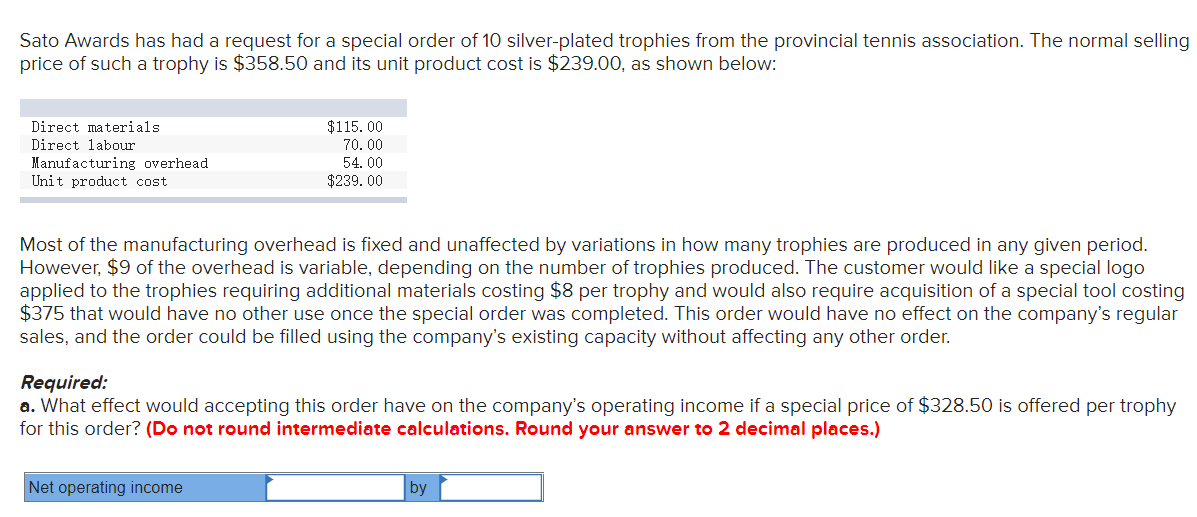

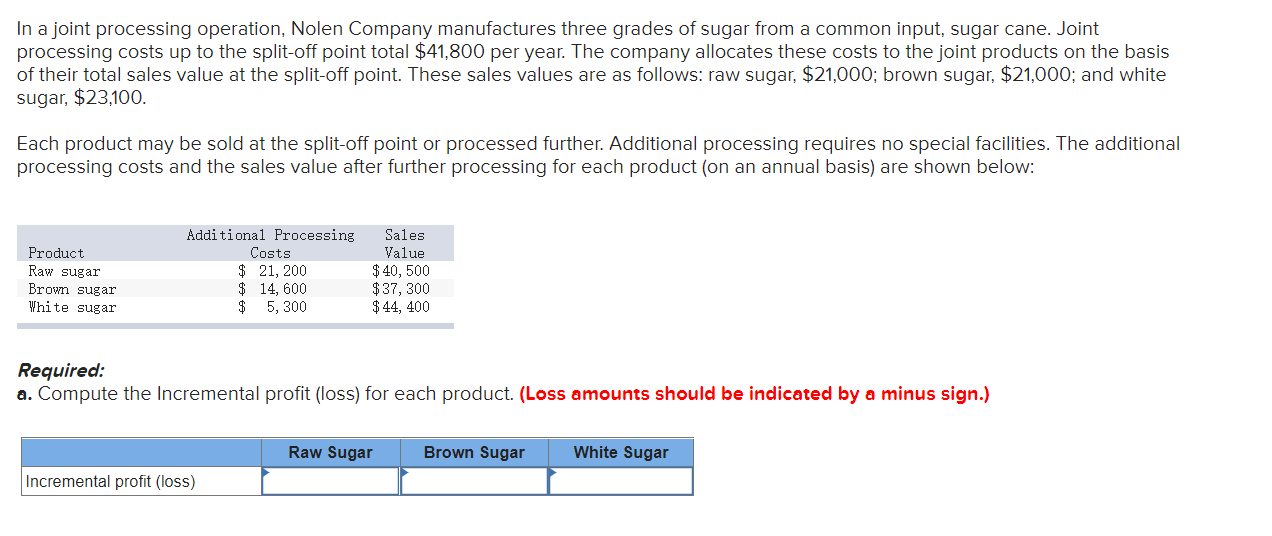

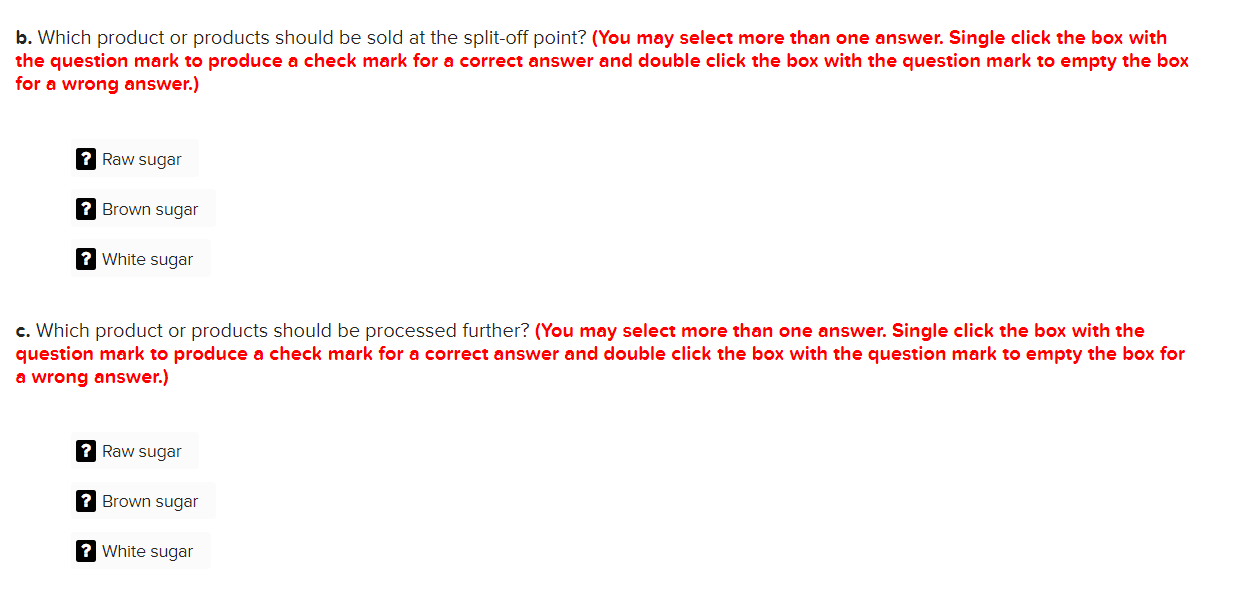

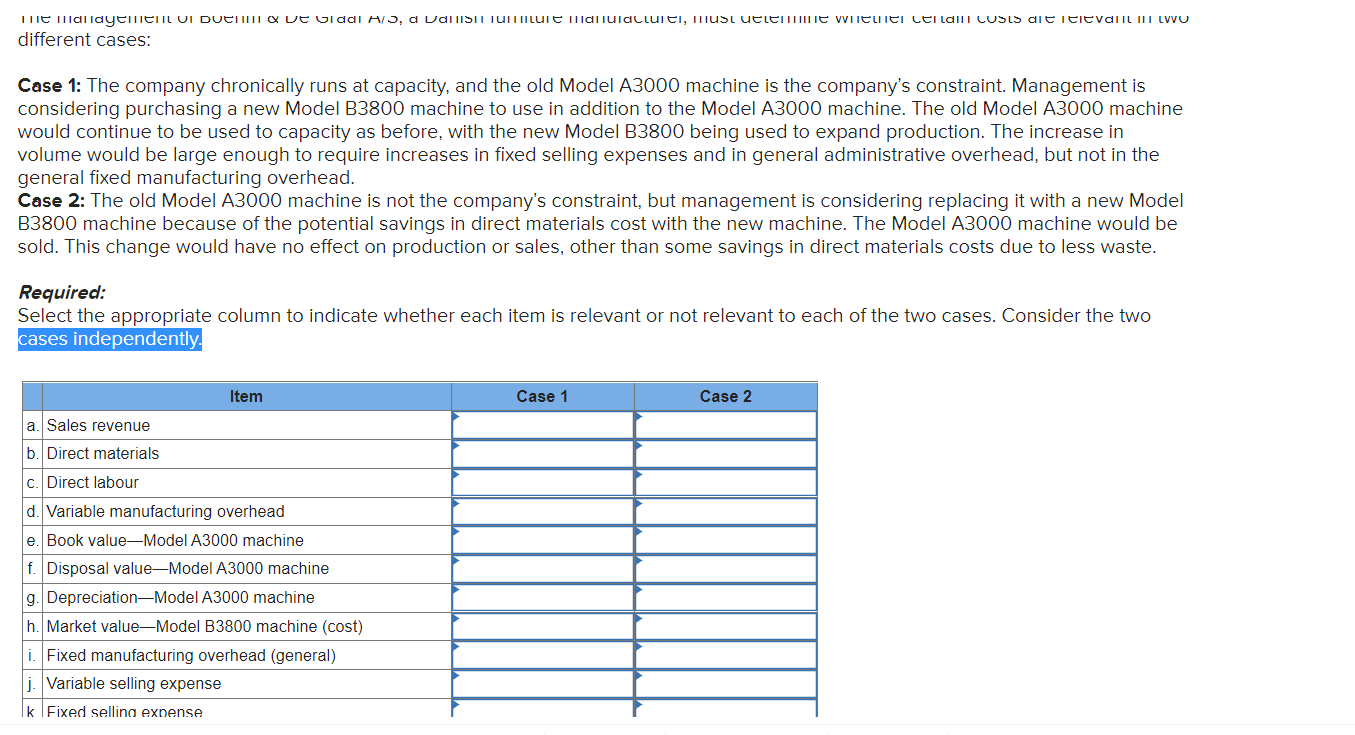

Sato Awards has had a request for a special order of 10 silver-plated trophies from the provincial tennis association. The normal selling price of such a trophy is $358.50 and its unit product cost is $239.00, as shown below: Most of the manufacturing overhead is fixed and unaffected by variations in how many trophies are produced in any given period. However, $9 of the overhead is variable, depending on the number of trophies produced. The customer would like a special logo applied to the trophies requiring additional materials costing $8 per trophy and would also require acquisition of a special tool costing $375 that would have no other use once the special order was completed. This order would have no effect on the company's regular sales, and the order could be filled using the company's existing capacity without affecting any other order. Required: a. What effect would accepting this order have on the company's operating income if a special price of $328.50 is offered per trophy for this order? (Do not round intermediate calculations. Round your answer to 2 decimal places.) In a joint processing operation, Nolen Company manufactures three grades of sugar from a common input, sugar cane. Joint processing costs up to the split-off point total $41,800 per year. The company allocates these costs to the joint products on the basis of their total sales value at the split-off point. These sales values are as follows: raw sugar, $21,000; brown sugar, $21,000; and white sugar, $23,100 Each product may be sold at the split-off point or processed further. Additional processing requires no special facilities. The additional processing costs and the sales value after further processing for each product (on an annual basis) are shown below: Required: a. Compute the Incremental profit (loss) for each product. (Loss amounts should be indicated by a minus sign.) b. Which product or products should be sold at the split-off point? (You may select more than one answer. Single click the box with the question mark to produce a check mark for a correct answer and double click the box with the question mark to empty the box for a wrong answer.) ? Raw sugar ? Brown sugar White sugar c. Which product or products should be processed further? (You may select more than one answer. Single click the box with the question mark to produce a check mark for a correct answer and double click the box with the question mark to empty the box for a wrong answer.) ? Brown sugar White sugar different cases: Case 1: The company chronically runs at capacity, and the old Model A3000 machine is the company's constraint. Management is considering purchasing a new Model B3800 machine to use in addition to the Model A3000 machine. The old Model A3000 machine would continue to be used to capacity as before, with the new Model B3800 being used to expand production. The increase in volume would be large enough to require increases in fixed selling expenses and in general administrative overhead, but not in the general fixed manufacturing overhead. Case 2: The old Model A3000 machine is not the company's constraint, but management is considering replacing it with a new Model B3800 machine because of the potential savings in direct materials cost with the new machine. The Model A3000 machine would be sold. This change would have no effect on production or sales, other than some savings in direct materials costs due to less waste. Required: Select the appropriate column to indicate whether each item is relevant or not relevant to each of the two cases. Consider the two

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts