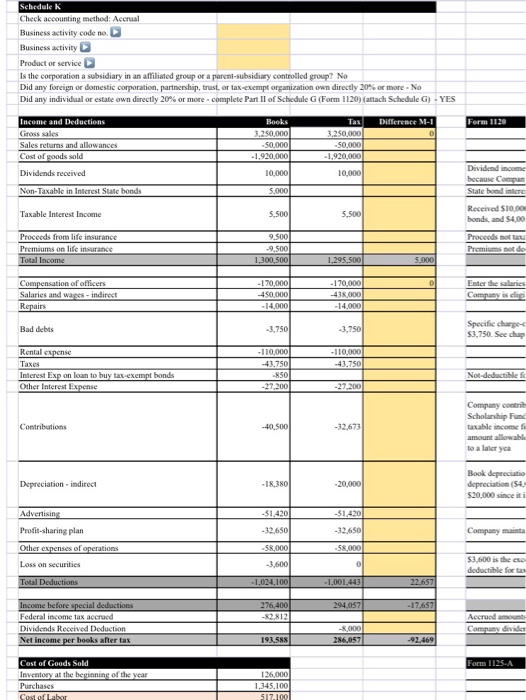

Question: Schedule K Check accounting method: Accrual Business activity code no. ? Business activity ? Product or service ? Is the corporation a subsidiary in an

| Schedule K | ||||||

| Check accounting method: Accrual | ||||||

| Business activity code no. ? | ||||||

| Business activity ? | ||||||

| Product or service ? | ||||||

| Is the corporation a subsidiary in an affiliated group or a parent-subsidiary controlled group? No | ||||||

| Did any foreign or domestic corporation, partnership, trust, or tax-exempt organization own directly 20% or more - No | ||||||

| Did any individual or estate own directly 20% or more - complete Part II of Schedule G (Form 1120) (attach Schedule G) - YES | ||||||

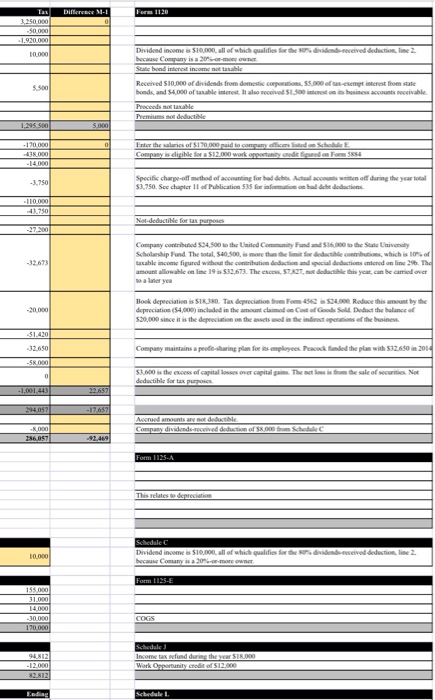

| Income and Deductions | Books | Tax | Difference M-1 | Form 1120 | ||

| Gross sales | 3,250,000 | 3,250,000 | - | |||

| Sales returns and allowances | (50,000) | (50,000) | ||||

| Cost of goods sold | (1,920,000) | (1,920,000) | ||||

| Dividends received | 10,000 | 10,000 | Dividend income is $10,000, all of which qualifies for the 80% dividends-received deduction, line 2, because Company is a 20%-or-more owner. | |||

| Non-Taxable in Interest State bonds | 5,000 | State bond interest income not taxable | ||||

| Taxable Interest Income | 5,500 | 5,500 | Received $10,000 of dividends from domestic corporations, $5,000 of tax-exempt interest from state bonds, and $4,000 of taxable interest. It also received $1,500 interest on its business accounts receivable. | |||

| Proceeds from life insurance | 9,500 | Proceeds not taxable | ||||

| Premiums on life insurance | (9,500) | Premiums not deductible | ||||

| Total Income | 1,300,500 | 1,295,500 | 5,000 | |||

| Compensation of officers | (170,000) | (170,000) | - | Enter the salaries of $170,000 paid to company officers listed on Schedule E. | ||

| Salaries and wages - indirect | (450,000) | (438,000) | Company is eligible for a $12,000 work opportunity credit figured on Form 5884 | |||

| Repairs | (14,000) | (14,000) | ||||

| Bad debts | (3,750) | (3,750) | Specific charge-off method of accounting for bad debts. Actual accounts written off during the year total $3,750. See chapter 11 of Publication 535 for information on bad debt deductions. | |||

| Rental expense | (110,000) | (110,000) | ||||

| Taxes | (43,750) | (43,750) | ||||

| Interest Exp on loan to buy tax-exempt bonds | (850) | Not-deductible for tax purposes | ||||

| Other Interest Expense | (27,200) | (27,200) | ||||

| Contributions | (40,500) | (32,673) | Company contributed $24,500 to the United Community Fund and $16,000 to the State University Scholarship Fund. The total, $40,500, is more than the limit for deductible contributions, which is 10% of taxable income figured without the contribution deduction and special deductions entered on line 29b. The amount allowable on line 19 is $32,673. The excess, $7,827, not deductible this year, can be carried over to a later yea | |||

| Depreciation - indirect | (18,380) | (20,000) | Book depreciation is $18,380. Tax depreciation from Form 4562 is $24,000. Reduce this amount by the depreciation ($4,000) included in the amount claimed on Cost of Goods Sold. Deduct the balance of $20,000 since it is the depreciation on the assets used in the indirect operations of the business. | |||

| Advertising | (51,420) | (51,420) | ||||

| Profit-sharing plan | (32,650) | (32,650) | Company maintains a profit-sharing plan for its employees. Peacock funded the plan with $32,650 in 2014 | |||

| Other expenses of operations | (58,000) | (58,000) | ||||

| Loss on securities | (3,600) | - | $3,600 is the excess of capital losses over capital gains. The net loss is from the sale of securities. Not deductible for tax purposes. | |||

| Total Deductions | (1,024,100) | (1,001,443) | 22,657 | |||

| Income before special deductions | 276,400 | 294,057 | (17,657) | |||

| Federal income tax accrued | (82,812) | Accrued amounts are not deductible. | ||||

| Dividends Received Deduction | (8,000) | Company dividends-received deduction of $8,000 from Schedule C | ||||

| Net income per books after tax | 193,588 | 286,057 | (92,469) | |||

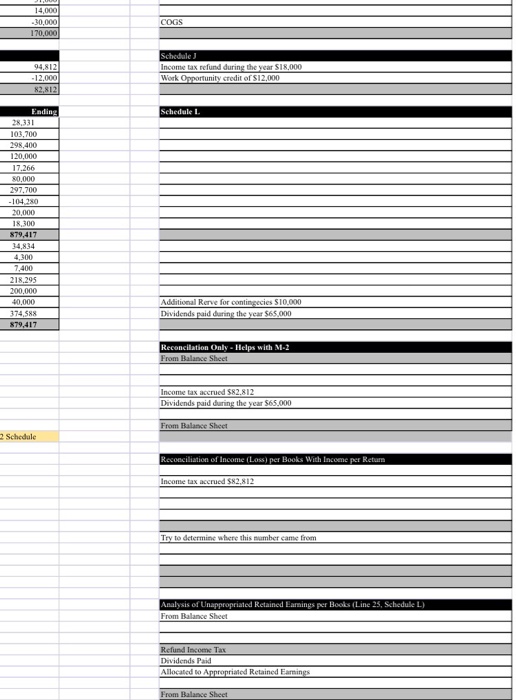

| Cost of Goods Sold | Form 1125-A | |||||

| Inventory at the beginning of the year | 126,000 | |||||

| Purchases | 1,345,100 | |||||

| Cost of Labor | 517,100 | |||||

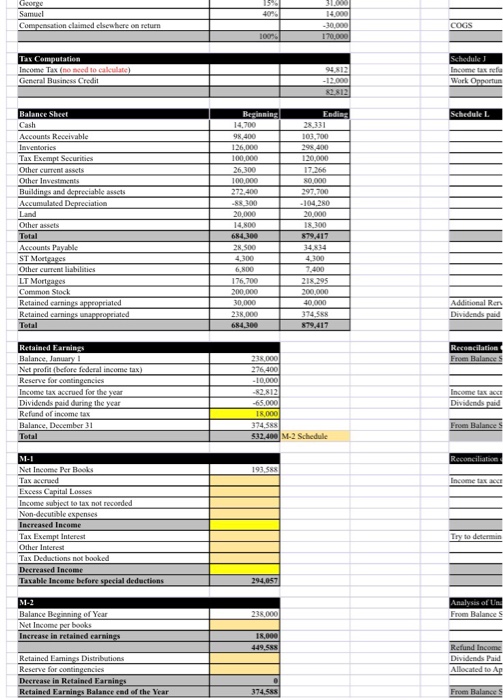

| Additional Sec 263A costs | 85,000 | This relates to depreciation | ||||

| Other costs | 145,200 | |||||

| Inventory at end of year | (298,400) | |||||

| Cost of Goods Sold | 1,920,000 | |||||

| Dividends and Special Deductions | Schedule C | |||||

| Dividends from 20% of more owns stock | -80% | 10,000 | Dividend income is $10,000, all of which qualifies for the 80% dividends-received deduction, line 2, because Comany is a 20%-or-more owner. | |||

| Compensation of Officers | Ownership | Form 1125-E | ||||

| James | 45% | 155,000 | ||||

| George | 15% | 31,000 | ||||

| Samuel | 40% | 14,000 | ||||

| Compensation claimed elsewhere on return | (30,000) | COGS | ||||

| 100% | 170,000 | |||||

| Tax Computation | Schedule J | |||||

| Income Tax (no need to calculate) | 94,812 | Income tax refund during the year $18,000 | ||||

| General Business Credit | (12,000) | Work Opportunity credit of $12,000 | ||||

| 82,812 | ||||||

| Balance Sheet | Beginning | Ending | Schedule L | |||

| Cash | 14,700 | 28,331 | ||||

| Accounts Receivable | 98,400 | 103,700 | ||||

| Inventories | 126,000 | 298,400 | ||||

| Tax Exempt Securities | 100,000 | 120,000 | ||||

| Other current assets | 26,300 | 17,266 | ||||

| Other Investments | 100,000 | 80,000 | ||||

| Buildings and depreciable assets | 272,400 | 297,700 | ||||

| Accumulated Depreciation | (88,300) | (104,280) | ||||

| Land | 20,000 | 20,000 | ||||

| Other assets | 14,800 | 18,300 | ||||

| Total | 684,300 | 879,417 | ||||

| Accounts Payable | 28,500 | 34,834 | ||||

| ST Mortgages | 4,300 | 4,300 | ||||

| Other current liabilities | 6,800 | 7,400 | ||||

| LT Mortgages | 176,700 | 218,295 | ||||

| Common Stock | 200,000 | 200,000 | ||||

| Retained earnings appropriated | 30,000 | 40,000 | Additional Rerve for contingecies $10,000 | |||

| Retained earnings unappropriated | 238,000 | 374,588 | Dividends paid during the year $65,000 | |||

| Total | 684,300 | 879,417 | ||||

| Retained Earnings | Reconcilation Only - Helps with M-2 | |||||

| Balance, January 1 | 238,000 | From Balance Sheet | ||||

| Net profit (before federal income tax) | 276,400 | |||||

| Reserve for contingencies | (10,000) | |||||

| Income tax accrued for the year | (82,812) | Income tax accrued $82,812 | ||||

| Dividends paid during the year | (65,000) | Dividends paid during the year $65,000 | ||||

| Refund of income tax | 18,000 | |||||

| Balance, December 31 | 374,588 | From Balance Sheet | ||||

| Total | 532,400 | M-2 Schedule | ||||

| M-1 | Reconciliation of Income (Loss) per Books With Income per Return | |||||

| Net Income Per Books | 193,588 | |||||

| Tax accrued | Income tax accrued $82,812 | |||||

| Excess Capital Losses | ||||||

| Income subject to tax not recorded | ||||||

| Non-decutible expenses | ||||||

| Increased Income | ||||||

| Tax Exempt Interest | Try to determine where this number came from | |||||

| Other Interest | ||||||

| Tax Deductions not booked | ||||||

| Decreased Income | ||||||

| Taxable Income before special deductions | 294,057 | |||||

| M-2 | Analysis of Unappropriated Retained Earnings per Books (Line 25, Schedule L) | |||||

| Balance Beginning of Year | 238,000 | From Balance Sheet | ||||

| Net Income per books | ||||||

| Increase in retained earnings | 18,000 | |||||

| 449,588 | Refund Income Tax | |||||

| Retained Earnings Distributions | Dividends Paid | |||||

| Reserve for contingencies | Allocated to Appropriated Retained Earnings | |||||

| Decrease in Retained Earnings | - | |||||

| Retained Earnings Balance end of the Year | 374,588 | From Balance Sheet | ||||

1. Complete the Instructor provided Excel spreadsheet by creating the book and tax column - the difference between book and tax is used for the M-1 and M 2 schedules. 2. Complete the M-1 and M-2 calculations on the Excel Spreadsheet. 1. Complete the Instructor provided Excel spreadsheet by creating the book and tax column - the difference between book and tax is used for the M-1 and M 2 schedules. 2. Complete the M-1 and M-2 calculations on the Excel Spreadsheet

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock