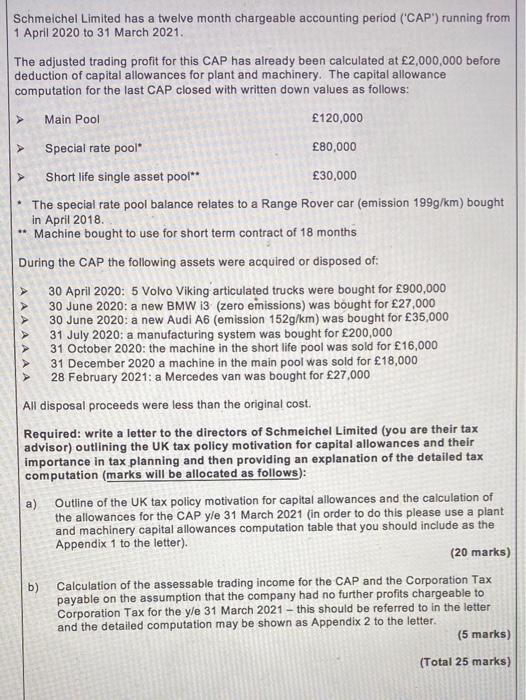

Schmeichel Limited has a twelve month chargeable accounting period ('CAP') running from 1 April 2020 to...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

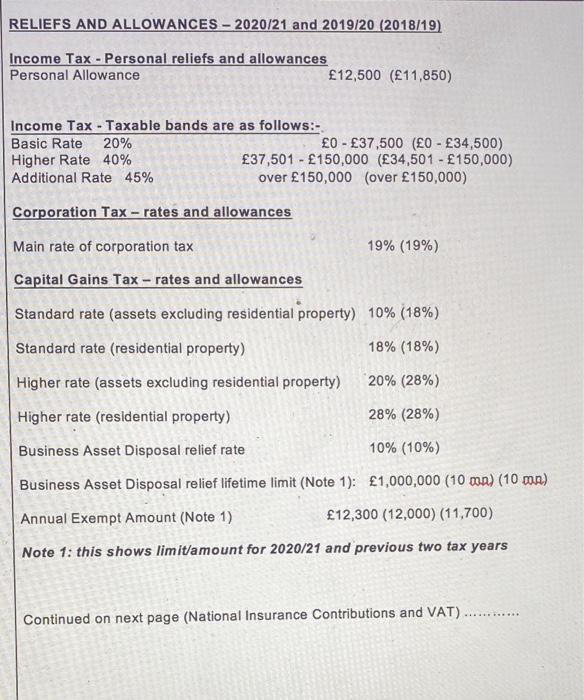

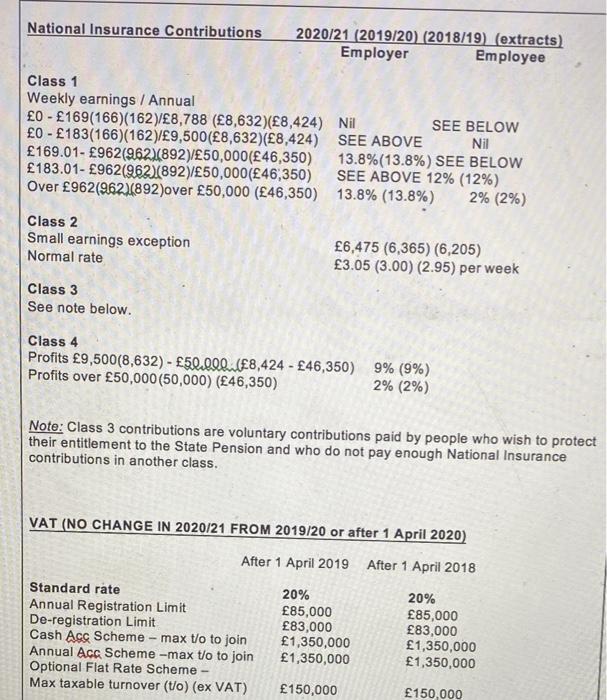

Schmeichel Limited has a twelve month chargeable accounting period ('CAP') running from 1 April 2020 to 31 March 2021. The adjusted trading profit for this CAP has already been calculated at £2,000,000 before deduction of capital allowances for plant and machinery. The capital allowance computation for the last CAP closed with written down values as follows: Main Pool £120,000 Special rate pool* £80,000 Short life single asset pool** £30,000 * The special rate pool balance relates to a Range Rover car (emission 199g/km) bought in April 2018. ** Machine bought to use for short term contract of 18 months During the CAP the following assets were acquired or disposed of: 30 April 2020: 5 Volvo Viking articulated trucks were bought for £900,000 30 June 2020: a new BMW 13 (zero emissions) was bought for £27,000 30 June 2020: a new Audi A6 (emission 152g/km) was bought for £35,000 31 July 2020: a manufacturing system was bought for £200,000 31 October 2020: the machine in the short life pool was sold for £16,000 31 December 2020 a machine in the main pool was sold for £18,000 28 February 2021: a Mercedes van was bought for £27,000 All disposal proceeds were less than the original cost. Required: write a letter to the directors of Schmeichel Limited (you are their tax advisor) outlining the UK tax policy motivation for capital allowances and their importance in tax planning and then providing an explanation of the detailed tax computation (marks will be allocated as follows): Outline of the UK tax policy motivation for capital allowances and the calculation of a) the allowances for the CAP y/e 31 March 2021 (in order to do this please use a plant and machinery capital allowances computation table that you should include as the Appendix 1 to the letter). (20 marks) Calculation of the assessable trading income for the CAP and the Corporation Tax b) payable on the assumption that the company had no further profits chargeable to Corporation Tax for the yle 31 March 2021 - this should be referred to in the letter and the detailed computation may be shown as Appendix 2 to the letter. (5 marks) (Total 25 marks) RELIEFS AND ALLOWANCES - 2020/21 and 2019/20 (2018/19) Income Tax - Personal reliefs and allowances Personal Allowance £12,500 (£11,850) Income Tax - Taxable bands are as follows:- Basic Rate 20% Higher Rate 40% Additional Rate 45% £0 - £37,500 (£O - £34,500) £37,501 - £150,000 (£34,501 - £150,000) over £150,000 (over £150,000) Corporation Tax - rates and allowances Main rate of corporation tax 19% (19%) Capital Gains Tax - rates and allowances Standard rate (assets excluding residential property) 10% (18%) Standard rate (residential property) 18% (18%) Higher rate (assets excluding residential property) 20% (28%) Higher rate (residential property) 28% (28%) Business Asset Disposal relief rate 10% (10%) Business Asset Disposal relief lifetime limit (Note 1): £1,000,000 (10 mn) (10 mn) Annual Exempt Amount (Note 1) £12,300 (12,000) (11,700) Note 1: this shows limit/amount for 2020/21 and previous two tax years Continued on next page (National Insurance Contributions and VAT) National Insurance Contributions 2020/21 (2019/20) (2018/19) (extracts) Employer Employee Class 1 Weekly earnings / Annual £0 - £169(166)(162)/£8,788 (£8,632)(£8,424) Nil £0 - £183(166)(162)/£9,500(£8,632)(£8,424) SEE ABOVE £169.01- £962(962)(892)/£50,000(£46,350) £183.01- £962(962)(892)/£50,000(£46,350) Over £962(962)(892)over £50,000 (£46,350) 13.8% (13.8%) SEE BELOW Nil 13.8%(13.8%) SEE BELOW SEE ABOVE 12% (12%) 2% (2%) Class 2 Small earnings exception £6,475 (6,365) (6,205) £3.05 (3.00) (2.95) per week Normal rate Class 3 See note below. Class 4 Profits £9,500(8,632) - £50.000 (£8,424 - £46,350) 9% (9%) Profits over £50,000 (50,000) (£46,350) 2% (2%) Note: Class 3 contributions are voluntary contributions paid by people who wish to protect their entitlement to the State Pension and who do not pay enough National Insurance contributions in another class. VAT (NO CHANGE IN 2020/21 FROM 2019/20 or after 1 April 2020) After 1 April 2019 After 1 April 2018 Standard rate 20% 20% Annual Registration Limit De-registration Limit Cash Acc Scheme - max t/o to join Annual Ac Scheme -max t/o to join Optional Flat Rate Scheme Max taxable turnover (t/o) (ex VAT) £85,000 £83,000 £85,000 £83,000 £1,350,000 £1,350,000 £1,350,000 £1,350,000 £150,000 £150,000 Schmeichel Limited has a twelve month chargeable accounting period ('CAP') running from 1 April 2020 to 31 March 2021. The adjusted trading profit for this CAP has already been calculated at £2,000,000 before deduction of capital allowances for plant and machinery. The capital allowance computation for the last CAP closed with written down values as follows: Main Pool £120,000 Special rate pool* £80,000 Short life single asset pool** £30,000 * The special rate pool balance relates to a Range Rover car (emission 199g/km) bought in April 2018. ** Machine bought to use for short term contract of 18 months During the CAP the following assets were acquired or disposed of: 30 April 2020: 5 Volvo Viking articulated trucks were bought for £900,000 30 June 2020: a new BMW 13 (zero emissions) was bought for £27,000 30 June 2020: a new Audi A6 (emission 152g/km) was bought for £35,000 31 July 2020: a manufacturing system was bought for £200,000 31 October 2020: the machine in the short life pool was sold for £16,000 31 December 2020 a machine in the main pool was sold for £18,000 28 February 2021: a Mercedes van was bought for £27,000 All disposal proceeds were less than the original cost. Required: write a letter to the directors of Schmeichel Limited (you are their tax advisor) outlining the UK tax policy motivation for capital allowances and their importance in tax planning and then providing an explanation of the detailed tax computation (marks will be allocated as follows): Outline of the UK tax policy motivation for capital allowances and the calculation of a) the allowances for the CAP y/e 31 March 2021 (in order to do this please use a plant and machinery capital allowances computation table that you should include as the Appendix 1 to the letter). (20 marks) Calculation of the assessable trading income for the CAP and the Corporation Tax b) payable on the assumption that the company had no further profits chargeable to Corporation Tax for the yle 31 March 2021 - this should be referred to in the letter and the detailed computation may be shown as Appendix 2 to the letter. (5 marks) (Total 25 marks) RELIEFS AND ALLOWANCES - 2020/21 and 2019/20 (2018/19) Income Tax - Personal reliefs and allowances Personal Allowance £12,500 (£11,850) Income Tax - Taxable bands are as follows:- Basic Rate 20% Higher Rate 40% Additional Rate 45% £0 - £37,500 (£O - £34,500) £37,501 - £150,000 (£34,501 - £150,000) over £150,000 (over £150,000) Corporation Tax - rates and allowances Main rate of corporation tax 19% (19%) Capital Gains Tax - rates and allowances Standard rate (assets excluding residential property) 10% (18%) Standard rate (residential property) 18% (18%) Higher rate (assets excluding residential property) 20% (28%) Higher rate (residential property) 28% (28%) Business Asset Disposal relief rate 10% (10%) Business Asset Disposal relief lifetime limit (Note 1): £1,000,000 (10 mn) (10 mn) Annual Exempt Amount (Note 1) £12,300 (12,000) (11,700) Note 1: this shows limit/amount for 2020/21 and previous two tax years Continued on next page (National Insurance Contributions and VAT) National Insurance Contributions 2020/21 (2019/20) (2018/19) (extracts) Employer Employee Class 1 Weekly earnings / Annual £0 - £169(166)(162)/£8,788 (£8,632)(£8,424) Nil £0 - £183(166)(162)/£9,500(£8,632)(£8,424) SEE ABOVE £169.01- £962(962)(892)/£50,000(£46,350) £183.01- £962(962)(892)/£50,000(£46,350) Over £962(962)(892)over £50,000 (£46,350) 13.8% (13.8%) SEE BELOW Nil 13.8%(13.8%) SEE BELOW SEE ABOVE 12% (12%) 2% (2%) Class 2 Small earnings exception £6,475 (6,365) (6,205) £3.05 (3.00) (2.95) per week Normal rate Class 3 See note below. Class 4 Profits £9,500(8,632) - £50.000 (£8,424 - £46,350) 9% (9%) Profits over £50,000 (50,000) (£46,350) 2% (2%) Note: Class 3 contributions are voluntary contributions paid by people who wish to protect their entitlement to the State Pension and who do not pay enough National Insurance contributions in another class. VAT (NO CHANGE IN 2020/21 FROM 2019/20 or after 1 April 2020) After 1 April 2019 After 1 April 2018 Standard rate 20% 20% Annual Registration Limit De-registration Limit Cash Acc Scheme - max t/o to join Annual Ac Scheme -max t/o to join Optional Flat Rate Scheme Max taxable turnover (t/o) (ex VAT) £85,000 £83,000 £85,000 £83,000 £1,350,000 £1,350,000 £1,350,000 £1,350,000 £150,000 £150,000 Schmeichel Limited has a twelve month chargeable accounting period ('CAP') running from 1 April 2020 to 31 March 2021. The adjusted trading profit for this CAP has already been calculated at £2,000,000 before deduction of capital allowances for plant and machinery. The capital allowance computation for the last CAP closed with written down values as follows: Main Pool £120,000 Special rate pool* £80,000 Short life single asset pool** £30,000 * The special rate pool balance relates to a Range Rover car (emission 199g/km) bought in April 2018. ** Machine bought to use for short term contract of 18 months During the CAP the following assets were acquired or disposed of: 30 April 2020: 5 Volvo Viking articulated trucks were bought for £900,000 30 June 2020: a new BMW 13 (zero emissions) was bought for £27,000 30 June 2020: a new Audi A6 (emission 152g/km) was bought for £35,000 31 July 2020: a manufacturing system was bought for £200,000 31 October 2020: the machine in the short life pool was sold for £16,000 31 December 2020 a machine in the main pool was sold for £18,000 28 February 2021: a Mercedes van was bought for £27,000 All disposal proceeds were less than the original cost. Required: write a letter to the directors of Schmeichel Limited (you are their tax advisor) outlining the UK tax policy motivation for capital allowances and their importance in tax planning and then providing an explanation of the detailed tax computation (marks will be allocated as follows): Outline of the UK tax policy motivation for capital allowances and the calculation of a) the allowances for the CAP y/e 31 March 2021 (in order to do this please use a plant and machinery capital allowances computation table that you should include as the Appendix 1 to the letter). (20 marks) Calculation of the assessable trading income for the CAP and the Corporation Tax b) payable on the assumption that the company had no further profits chargeable to Corporation Tax for the yle 31 March 2021 - this should be referred to in the letter and the detailed computation may be shown as Appendix 2 to the letter. (5 marks) (Total 25 marks) RELIEFS AND ALLOWANCES - 2020/21 and 2019/20 (2018/19) Income Tax - Personal reliefs and allowances Personal Allowance £12,500 (£11,850) Income Tax - Taxable bands are as follows:- Basic Rate 20% Higher Rate 40% Additional Rate 45% £0 - £37,500 (£O - £34,500) £37,501 - £150,000 (£34,501 - £150,000) over £150,000 (over £150,000) Corporation Tax - rates and allowances Main rate of corporation tax 19% (19%) Capital Gains Tax - rates and allowances Standard rate (assets excluding residential property) 10% (18%) Standard rate (residential property) 18% (18%) Higher rate (assets excluding residential property) 20% (28%) Higher rate (residential property) 28% (28%) Business Asset Disposal relief rate 10% (10%) Business Asset Disposal relief lifetime limit (Note 1): £1,000,000 (10 mn) (10 mn) Annual Exempt Amount (Note 1) £12,300 (12,000) (11,700) Note 1: this shows limit/amount for 2020/21 and previous two tax years Continued on next page (National Insurance Contributions and VAT) National Insurance Contributions 2020/21 (2019/20) (2018/19) (extracts) Employer Employee Class 1 Weekly earnings / Annual £0 - £169(166)(162)/£8,788 (£8,632)(£8,424) Nil £0 - £183(166)(162)/£9,500(£8,632)(£8,424) SEE ABOVE £169.01- £962(962)(892)/£50,000(£46,350) £183.01- £962(962)(892)/£50,000(£46,350) Over £962(962)(892)over £50,000 (£46,350) 13.8% (13.8%) SEE BELOW Nil 13.8%(13.8%) SEE BELOW SEE ABOVE 12% (12%) 2% (2%) Class 2 Small earnings exception £6,475 (6,365) (6,205) £3.05 (3.00) (2.95) per week Normal rate Class 3 See note below. Class 4 Profits £9,500(8,632) - £50.000 (£8,424 - £46,350) 9% (9%) Profits over £50,000 (50,000) (£46,350) 2% (2%) Note: Class 3 contributions are voluntary contributions paid by people who wish to protect their entitlement to the State Pension and who do not pay enough National Insurance contributions in another class. VAT (NO CHANGE IN 2020/21 FROM 2019/20 or after 1 April 2020) After 1 April 2019 After 1 April 2018 Standard rate 20% 20% Annual Registration Limit De-registration Limit Cash Acc Scheme - max t/o to join Annual Ac Scheme -max t/o to join Optional Flat Rate Scheme Max taxable turnover (t/o) (ex VAT) £85,000 £83,000 £85,000 £83,000 £1,350,000 £1,350,000 £1,350,000 £1,350,000 £150,000 £150,000 Schmeichel Limited has a twelve month chargeable accounting period ('CAP') running from 1 April 2020 to 31 March 2021. The adjusted trading profit for this CAP has already been calculated at £2,000,000 before deduction of capital allowances for plant and machinery. The capital allowance computation for the last CAP closed with written down values as follows: Main Pool £120,000 Special rate pool* £80,000 Short life single asset pool** £30,000 * The special rate pool balance relates to a Range Rover car (emission 199g/km) bought in April 2018. ** Machine bought to use for short term contract of 18 months During the CAP the following assets were acquired or disposed of: 30 April 2020: 5 Volvo Viking articulated trucks were bought for £900,000 30 June 2020: a new BMW 13 (zero emissions) was bought for £27,000 30 June 2020: a new Audi A6 (emission 152g/km) was bought for £35,000 31 July 2020: a manufacturing system was bought for £200,000 31 October 2020: the machine in the short life pool was sold for £16,000 31 December 2020 a machine in the main pool was sold for £18,000 28 February 2021: a Mercedes van was bought for £27,000 All disposal proceeds were less than the original cost. Required: write a letter to the directors of Schmeichel Limited (you are their tax advisor) outlining the UK tax policy motivation for capital allowances and their importance in tax planning and then providing an explanation of the detailed tax computation (marks will be allocated as follows): Outline of the UK tax policy motivation for capital allowances and the calculation of a) the allowances for the CAP y/e 31 March 2021 (in order to do this please use a plant and machinery capital allowances computation table that you should include as the Appendix 1 to the letter). (20 marks) Calculation of the assessable trading income for the CAP and the Corporation Tax b) payable on the assumption that the company had no further profits chargeable to Corporation Tax for the yle 31 March 2021 - this should be referred to in the letter and the detailed computation may be shown as Appendix 2 to the letter. (5 marks) (Total 25 marks) RELIEFS AND ALLOWANCES - 2020/21 and 2019/20 (2018/19) Income Tax - Personal reliefs and allowances Personal Allowance £12,500 (£11,850) Income Tax - Taxable bands are as follows:- Basic Rate 20% Higher Rate 40% Additional Rate 45% £0 - £37,500 (£O - £34,500) £37,501 - £150,000 (£34,501 - £150,000) over £150,000 (over £150,000) Corporation Tax - rates and allowances Main rate of corporation tax 19% (19%) Capital Gains Tax - rates and allowances Standard rate (assets excluding residential property) 10% (18%) Standard rate (residential property) 18% (18%) Higher rate (assets excluding residential property) 20% (28%) Higher rate (residential property) 28% (28%) Business Asset Disposal relief rate 10% (10%) Business Asset Disposal relief lifetime limit (Note 1): £1,000,000 (10 mn) (10 mn) Annual Exempt Amount (Note 1) £12,300 (12,000) (11,700) Note 1: this shows limit/amount for 2020/21 and previous two tax years Continued on next page (National Insurance Contributions and VAT) National Insurance Contributions 2020/21 (2019/20) (2018/19) (extracts) Employer Employee Class 1 Weekly earnings / Annual £0 - £169(166)(162)/£8,788 (£8,632)(£8,424) Nil £0 - £183(166)(162)/£9,500(£8,632)(£8,424) SEE ABOVE £169.01- £962(962)(892)/£50,000(£46,350) £183.01- £962(962)(892)/£50,000(£46,350) Over £962(962)(892)over £50,000 (£46,350) 13.8% (13.8%) SEE BELOW Nil 13.8%(13.8%) SEE BELOW SEE ABOVE 12% (12%) 2% (2%) Class 2 Small earnings exception £6,475 (6,365) (6,205) £3.05 (3.00) (2.95) per week Normal rate Class 3 See note below. Class 4 Profits £9,500(8,632) - £50.000 (£8,424 - £46,350) 9% (9%) Profits over £50,000 (50,000) (£46,350) 2% (2%) Note: Class 3 contributions are voluntary contributions paid by people who wish to protect their entitlement to the State Pension and who do not pay enough National Insurance contributions in another class. VAT (NO CHANGE IN 2020/21 FROM 2019/20 or after 1 April 2020) After 1 April 2019 After 1 April 2018 Standard rate 20% 20% Annual Registration Limit De-registration Limit Cash Acc Scheme - max t/o to join Annual Ac Scheme -max t/o to join Optional Flat Rate Scheme Max taxable turnover (t/o) (ex VAT) £85,000 £83,000 £85,000 £83,000 £1,350,000 £1,350,000 £1,350,000 £1,350,000 £150,000 £150,000 Schmeichel Limited has a twelve month chargeable accounting period ('CAP') running from 1 April 2020 to 31 March 2021. The adjusted trading profit for this CAP has already been calculated at £2,000,000 before deduction of capital allowances for plant and machinery. The capital allowance computation for the last CAP closed with written down values as follows: Main Pool £120,000 Special rate pool* £80,000 Short life single asset pool** £30,000 * The special rate pool balance relates to a Range Rover car (emission 199g/km) bought in April 2018. ** Machine bought to use for short term contract of 18 months During the CAP the following assets were acquired or disposed of: 30 April 2020: 5 Volvo Viking articulated trucks were bought for £900,000 30 June 2020: a new BMW 13 (zero emissions) was bought for £27,000 30 June 2020: a new Audi A6 (emission 152g/km) was bought for £35,000 31 July 2020: a manufacturing system was bought for £200,000 31 October 2020: the machine in the short life pool was sold for £16,000 31 December 2020 a machine in the main pool was sold for £18,000 28 February 2021: a Mercedes van was bought for £27,000 All disposal proceeds were less than the original cost. Required: write a letter to the directors of Schmeichel Limited (you are their tax advisor) outlining the UK tax policy motivation for capital allowances and their importance in tax planning and then providing an explanation of the detailed tax computation (marks will be allocated as follows): Outline of the UK tax policy motivation for capital allowances and the calculation of a) the allowances for the CAP y/e 31 March 2021 (in order to do this please use a plant and machinery capital allowances computation table that you should include as the Appendix 1 to the letter). (20 marks) Calculation of the assessable trading income for the CAP and the Corporation Tax b) payable on the assumption that the company had no further profits chargeable to Corporation Tax for the yle 31 March 2021 - this should be referred to in the letter and the detailed computation may be shown as Appendix 2 to the letter. (5 marks) (Total 25 marks) RELIEFS AND ALLOWANCES - 2020/21 and 2019/20 (2018/19) Income Tax - Personal reliefs and allowances Personal Allowance £12,500 (£11,850) Income Tax - Taxable bands are as follows:- Basic Rate 20% Higher Rate 40% Additional Rate 45% £0 - £37,500 (£O - £34,500) £37,501 - £150,000 (£34,501 - £150,000) over £150,000 (over £150,000) Corporation Tax - rates and allowances Main rate of corporation tax 19% (19%) Capital Gains Tax - rates and allowances Standard rate (assets excluding residential property) 10% (18%) Standard rate (residential property) 18% (18%) Higher rate (assets excluding residential property) 20% (28%) Higher rate (residential property) 28% (28%) Business Asset Disposal relief rate 10% (10%) Business Asset Disposal relief lifetime limit (Note 1): £1,000,000 (10 mn) (10 mn) Annual Exempt Amount (Note 1) £12,300 (12,000) (11,700) Note 1: this shows limit/amount for 2020/21 and previous two tax years Continued on next page (National Insurance Contributions and VAT) National Insurance Contributions 2020/21 (2019/20) (2018/19) (extracts) Employer Employee Class 1 Weekly earnings / Annual £0 - £169(166)(162)/£8,788 (£8,632)(£8,424) Nil £0 - £183(166)(162)/£9,500(£8,632)(£8,424) SEE ABOVE £169.01- £962(962)(892)/£50,000(£46,350) £183.01- £962(962)(892)/£50,000(£46,350) Over £962(962)(892)over £50,000 (£46,350) 13.8% (13.8%) SEE BELOW Nil 13.8%(13.8%) SEE BELOW SEE ABOVE 12% (12%) 2% (2%) Class 2 Small earnings exception £6,475 (6,365) (6,205) £3.05 (3.00) (2.95) per week Normal rate Class 3 See note below. Class 4 Profits £9,500(8,632) - £50.000 (£8,424 - £46,350) 9% (9%) Profits over £50,000 (50,000) (£46,350) 2% (2%) Note: Class 3 contributions are voluntary contributions paid by people who wish to protect their entitlement to the State Pension and who do not pay enough National Insurance contributions in another class. VAT (NO CHANGE IN 2020/21 FROM 2019/20 or after 1 April 2020) After 1 April 2019 After 1 April 2018 Standard rate 20% 20% Annual Registration Limit De-registration Limit Cash Acc Scheme - max t/o to join Annual Ac Scheme -max t/o to join Optional Flat Rate Scheme Max taxable turnover (t/o) (ex VAT) £85,000 £83,000 £85,000 £83,000 £1,350,000 £1,350,000 £1,350,000 £1,350,000 £150,000 £150,000 Schmeichel Limited has a twelve month chargeable accounting period ('CAP') running from 1 April 2020 to 31 March 2021. The adjusted trading profit for this CAP has already been calculated at £2,000,000 before deduction of capital allowances for plant and machinery. The capital allowance computation for the last CAP closed with written down values as follows: Main Pool £120,000 Special rate pool* £80,000 Short life single asset pool** £30,000 * The special rate pool balance relates to a Range Rover car (emission 199g/km) bought in April 2018. ** Machine bought to use for short term contract of 18 months During the CAP the following assets were acquired or disposed of: 30 April 2020: 5 Volvo Viking articulated trucks were bought for £900,000 30 June 2020: a new BMW 13 (zero emissions) was bought for £27,000 30 June 2020: a new Audi A6 (emission 152g/km) was bought for £35,000 31 July 2020: a manufacturing system was bought for £200,000 31 October 2020: the machine in the short life pool was sold for £16,000 31 December 2020 a machine in the main pool was sold for £18,000 28 February 2021: a Mercedes van was bought for £27,000 All disposal proceeds were less than the original cost. Required: write a letter to the directors of Schmeichel Limited (you are their tax advisor) outlining the UK tax policy motivation for capital allowances and their importance in tax planning and then providing an explanation of the detailed tax computation (marks will be allocated as follows): Outline of the UK tax policy motivation for capital allowances and the calculation of a) the allowances for the CAP y/e 31 March 2021 (in order to do this please use a plant and machinery capital allowances computation table that you should include as the Appendix 1 to the letter). (20 marks) Calculation of the assessable trading income for the CAP and the Corporation Tax b) payable on the assumption that the company had no further profits chargeable to Corporation Tax for the yle 31 March 2021 - this should be referred to in the letter and the detailed computation may be shown as Appendix 2 to the letter. (5 marks) (Total 25 marks) RELIEFS AND ALLOWANCES - 2020/21 and 2019/20 (2018/19) Income Tax - Personal reliefs and allowances Personal Allowance £12,500 (£11,850) Income Tax - Taxable bands are as follows:- Basic Rate 20% Higher Rate 40% Additional Rate 45% £0 - £37,500 (£O - £34,500) £37,501 - £150,000 (£34,501 - £150,000) over £150,000 (over £150,000) Corporation Tax - rates and allowances Main rate of corporation tax 19% (19%) Capital Gains Tax - rates and allowances Standard rate (assets excluding residential property) 10% (18%) Standard rate (residential property) 18% (18%) Higher rate (assets excluding residential property) 20% (28%) Higher rate (residential property) 28% (28%) Business Asset Disposal relief rate 10% (10%) Business Asset Disposal relief lifetime limit (Note 1): £1,000,000 (10 mn) (10 mn) Annual Exempt Amount (Note 1) £12,300 (12,000) (11,700) Note 1: this shows limit/amount for 2020/21 and previous two tax years Continued on next page (National Insurance Contributions and VAT) National Insurance Contributions 2020/21 (2019/20) (2018/19) (extracts) Employer Employee Class 1 Weekly earnings / Annual £0 - £169(166)(162)/£8,788 (£8,632)(£8,424) Nil £0 - £183(166)(162)/£9,500(£8,632)(£8,424) SEE ABOVE £169.01- £962(962)(892)/£50,000(£46,350) £183.01- £962(962)(892)/£50,000(£46,350) Over £962(962)(892)over £50,000 (£46,350) 13.8% (13.8%) SEE BELOW Nil 13.8%(13.8%) SEE BELOW SEE ABOVE 12% (12%) 2% (2%) Class 2 Small earnings exception £6,475 (6,365) (6,205) £3.05 (3.00) (2.95) per week Normal rate Class 3 See note below. Class 4 Profits £9,500(8,632) - £50.000 (£8,424 - £46,350) 9% (9%) Profits over £50,000 (50,000) (£46,350) 2% (2%) Note: Class 3 contributions are voluntary contributions paid by people who wish to protect their entitlement to the State Pension and who do not pay enough National Insurance contributions in another class. VAT (NO CHANGE IN 2020/21 FROM 2019/20 or after 1 April 2020) After 1 April 2019 After 1 April 2018 Standard rate 20% 20% Annual Registration Limit De-registration Limit Cash Acc Scheme - max t/o to join Annual Ac Scheme -max t/o to join Optional Flat Rate Scheme Max taxable turnover (t/o) (ex VAT) £85,000 £83,000 £85,000 £83,000 £1,350,000 £1,350,000 £1,350,000 £1,350,000 £150,000 £150,000

Expert Answer:

Answer rating: 100% (QA)

Dear Directors I am writing to outline the UK tax policy motivation for capital allowances and the calculation of the allowances for the twelve month ... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

On 30 June 2020 Sunny Ltd acquired all assets (except for cash), and assumed the accounts payable of Snowy Ltd. At this date, the carrying amounts of assets and liabilities of Snowy Ltd were: Cash...

-

In April 2014, Lenape Corporation acquired new business machinery with a total cost of $775,000. Assuming the machinery qualifies for both the Section 179 deduction and bonus depreciation, calculate...

-

A new machine was bought for $9,000 with a life of six years and no salvage value . Its annual operating costs were as follows: $7,000, $7,350, $7,717.50,..., $8,933.97. If the MARR = 12%, what was...

-

First Ownership orders merchandise from several suppliers from around the world. Each of the suppliers has different shipping or transportation terms. At the end of December, First Ownership had the...

-

In Behind the Wave of Corporate Fraud: A Change in How Auditors Work, the Wall Street Journal detailed several of the recent accounting scandals and the techniques management used to deceive both the...

-

Suppose you land your first job with Columbia Records in New York City and, after your first week at work, you deposit $100 in your checking account at Chase Manhattan Bank. If the reserve...

-

Persistent Earnings Identify each of the following items as either (P) persistent, or (T) transitory. a. Sale of merchandise. b. Settlement of a lawsuit. c. Interest income. d. Payment to vendors. e....

-

Using the income statement and balance sheet presented here, compute the following ratios. Compare your results with the industry averages. What strengths and weaknesses are apparent? Ratio Industry...

-

Chancer, a SA resident, occupied a position that required him to be entrusted with funds to be used for secret operations. Over a number of years he appropriated funds to himself and, in total, took...

-

List the MNCs key stakeholders and describe their stake in the firm.

-

Respond to the following: What is a situation when you were stereotyped or stereotyped someone? What happened, what was the stereotype, and how it affected communication in the situation? How the...

-

On august 18 , 2018 Blue loaned to his sister Berry P200,000 at an interest rate of 12 % per annum payable in 1 year thereafter . One month before the debt becomes due Berry's husband died ....

-

As you have reviewed in this week's readings, there are several ways a company can secure long-term financing. Your role this week is to advocate for one of these forms of financing and argue against...

-

A global consumer packaged goods (CPG) company has set an ambitious goal for itself: double revenues while keeping the costs minimal within eight years. Of course, the leadership knows that such...

-

SQL Functions are what I'm looking for. Write function called GET_JOBTITLE where it accepts (receive) job_id as INPUT and return CHARACTER value ... You will provide job as CHARACTER input and it...

-

A Composite opportunity cost metric b Simple opportunity cost metric c Non-stochastic discount rate under all circumstances d Risk-adjusted discount rate under all circumstances Question 2 An...

-

Problem 4-13 To correct a birth defect, the tibia of the leg is straightened using three wires that are attached through holes made in the bone and then to an external brace that is worn by the...

-

How can you tell from the vertex form y = a(x - h) 2 + k whether a quadratic function has no real zeros?

-

A Zogby poll found that 75% of Americans can name all of The Three StoogesMoe, Curly, and Larry. Assuming this finding to be based on a simple random sample of 1200 Americans, construct and interpret...

-

A regression model has 3 independent variables and 20 observations, and the calculated Durbin-Watson d statistic is 0.91. What, if any, conclusion will be reached in testing for autocorrelation of...

-

During a summer visit to Cancun, Mexico, you stay in an air-conditioned room. Getting ready to leave your room for the beach, you put on your sunglasses. The minute you step outside, your sunglasses...

-

On January 1, 2018, Ranier, Inc., issued \(\$ 300,000\) of ten percent, 15 -year bonds for \(\$ 351,876\), yielding an effective interest rate of eight percent. Semiannual interest is payable on June...

-

The Peoples National Bank raised capital through the sale of \(\$ 100\) million face value of four percent coupon rate, ten-year bonds. The bonds paid interest semiannually and were sold at a time...

-

The financial statements for the Columbia Sportswear Company can be found in Appendix A at the end of this book. Required Answer the following questions: a. How much were Columbia's current...

Study smarter with the SolutionInn App