Question: se 1: 2 3 -4 5 6 Question 9 (1 point) Given: - The CAPM holds The market has an expected return of 10% -

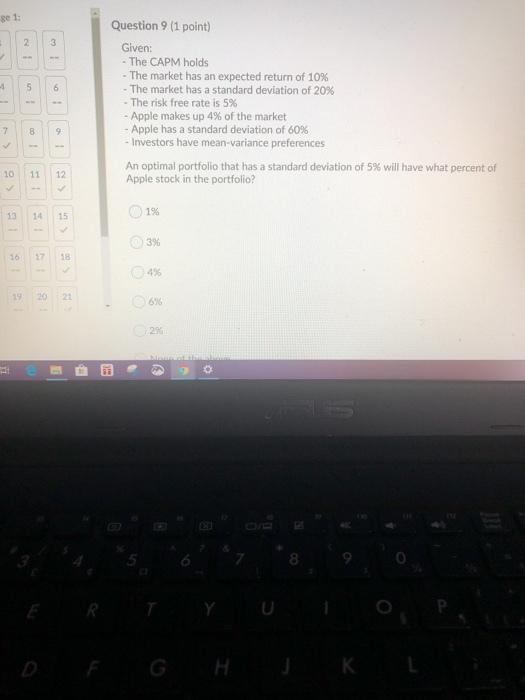

se 1: 2 3 -4 5 6 Question 9 (1 point) Given: - The CAPM holds The market has an expected return of 10% - The market has a standard deviation of 20% - The risk free rate is 5% - Apple makes up 4% of the market - Apple has a standard deviation of 60% - Investors have mean-variance preferences An optimal portfolio that has a standard deviation of 5% will have what percent of Apple stock in the portfolio? 7 8 9 10 11 12 13 1% 15 3% 16 17 18 4% 19 20 21 . 8 R. F G H K

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock