1) Based on your observation, do you satisfy with the level of competency that is being...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

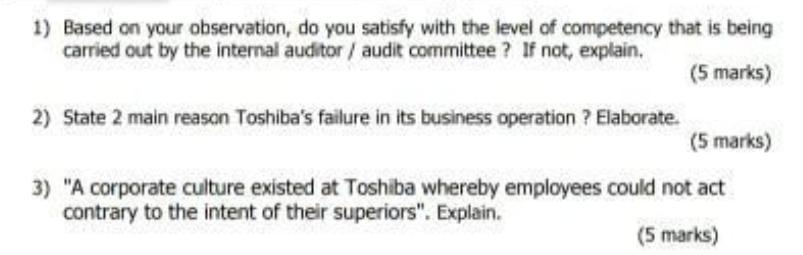

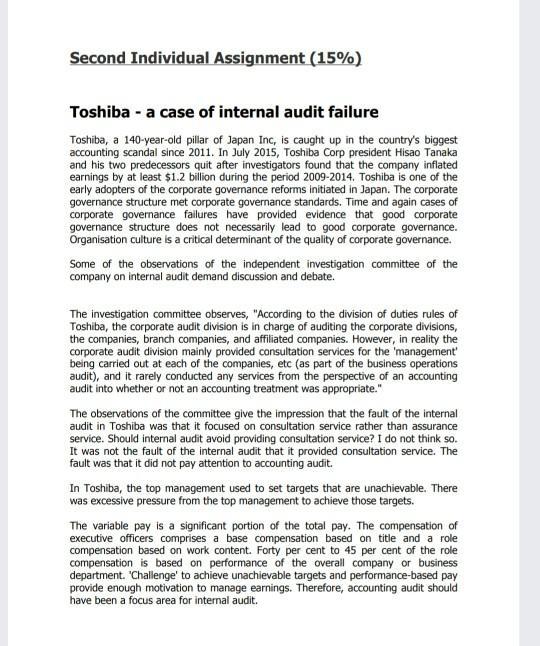

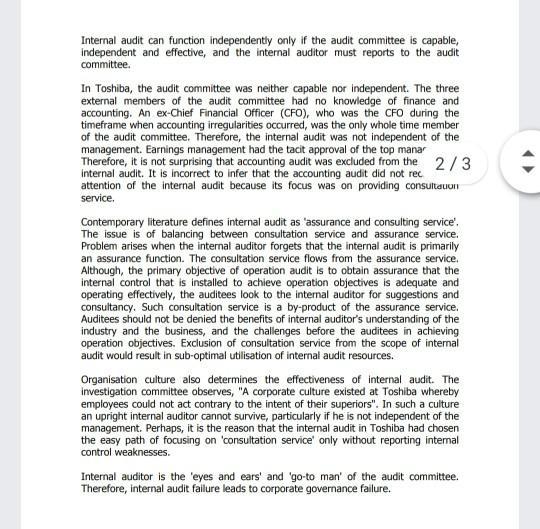

1) Based on your observation, do you satisfy with the level of competency that is being carried out by the internal auditor/ audit committee ? If not, explain. (5 marks) 2) State 2 main reason Toshiba's failure in its business operation ? Elaborate. (5 marks) 3) "A corporate culture existed at Toshiba whereby employees could not act contrary to the intent of their superiors". Explain. (5 marks) Second Individual Assignment (15%) Toshiba - a case of internal audit failure Toshiba, a 140-year-old pillar of Japan Inc, is caught up in the country's biggest accounting scandal since 2011. In July 2015, Toshiba Corp president Hisao Tanaka and his two predecessors quit after investigators found that the company inflated earnings by at least $1.2 billion during the period 2009-2014. Toshiba is one of the early adopters of the corporate governance reforms initiated in Japan. The corporate governance structure met corporate governance standards. Time and again cases of corporate governance failures have provided evidence that good corporate governance structure does not necessarily lead to good corporate governance. Organisation culture is a critical determinant of the quality of corporate governance. Some of the observations of the independent investigation committee of the company on internal audit demand discussion and debate. The investigation committee observes, "According to the division of duties rules of Toshiba, the corporate audit division is in charge of auditing the corporate divisions, the companies, branch companies, and affiliated companies. However, in reality the corporate audit division mainly provided consultation services for the 'management being carried out at each of the companies, etc (as part of the business operations audit), and it rarely conducted any services from the perspective of an accounting audit into whether or not an accounting treatment was appropriate." The observations of the committee give the impression that the fault of the internal audit in Toshiba was that it focused on consultation service rather than assurance service. Should internal audit avoid providing consultation service? I do not think so. It was not the fault of the internal audit that it provided consultation service. The fault was that it did not pay attention to accounting audit. In Toshiba, the top management used to set targets that are unachievable. There was excessive pressure from the top management to achieve those targets. The variable pay is a significant portion of the total pay. The compensation of executive officers comprises a base compensation based on title and a role compensation based on work content. Forty per cent to 45 per cent of the role compensation is based on performance of the overall company or business department. 'Challenge' to achieve unachievable targets and performance-based pay provide enough motivation to manage earnings. Therefore, accounting audit should have been a focus area for internal audit. Internal audit can function independently only if the audit committee is capable, independent and effective, and the internal auditor must reports to the audit committee. In Toshiba, the audit committee was neither capable nor independent. The three external members of the audit committee had no knowledge of finance and accounting. An ex-Chief Financial Officer (CFO), who was the CFO during the timeframe when accounting irregularities occurred, was the only whole time member of the audit committee. Therefore, the internal audit was not independent of the management. Earnings management had the tacit approval of the top manar Therefore, it is not surprising that accounting audit was excluded from the 2/3 internal audit. It is incorrect to infer that the accounting audit did not rec. attention of the internal audit because its focus was on providing consultaun service. Contemporary literature defines internal audit as 'assurance and consulting service'. The issue is of balancing between consultation service and assurance service. Problem arises when the internal auditor forgets that the internal audit is primarily an assurance function. The consultation service flows from the assurance service. Although, the primary objective of operation audit is to obtain assurance that the internal control that is installed to achieve operation objectives is adequate and operating effectively, the auditees look to the intermal auditor for suggestions and consultancy. Such consultation service is a by-product of the assurance service. Auditees should not be denied the benefits of internal auditor's understanding of the industry and the business, and the challenges before the auditees in achieving operation objectives. Exclusion of consultation service from the scope of internal audit would result in sub-optimal utilisation of internal audit resources. Organisation culture also determines the effectiveness of internal audit. The investigation committee observes, "A corporate culture existed at Toshiba whereby employees could not act contrary to the intent of their superiors". In such a culture an upright internal auditor cannot survive, particularly if he is not independent of the management. Perhaps, it is the reason that the internal audit in Toshiba had chosen the easy path of focusing on 'consultation service' only without reporting intemal control weaknesses. Internal auditor is the 'eyes and ears' and 'go-to man' of the audit committee. Therefore, internal audit failure leads to corporate governance failure. 1) Based on your observation, do you satisfy with the level of competency that is being carried out by the internal auditor/ audit committee ? If not, explain. (5 marks) 2) State 2 main reason Toshiba's failure in its business operation ? Elaborate. (5 marks) 3) "A corporate culture existed at Toshiba whereby employees could not act contrary to the intent of their superiors". Explain. (5 marks) Second Individual Assignment (15%) Toshiba - a case of internal audit failure Toshiba, a 140-year-old pillar of Japan Inc, is caught up in the country's biggest accounting scandal since 2011. In July 2015, Toshiba Corp president Hisao Tanaka and his two predecessors quit after investigators found that the company inflated earnings by at least $1.2 billion during the period 2009-2014. Toshiba is one of the early adopters of the corporate governance reforms initiated in Japan. The corporate governance structure met corporate governance standards. Time and again cases of corporate governance failures have provided evidence that good corporate governance structure does not necessarily lead to good corporate governance. Organisation culture is a critical determinant of the quality of corporate governance. Some of the observations of the independent investigation committee of the company on internal audit demand discussion and debate. The investigation committee observes, "According to the division of duties rules of Toshiba, the corporate audit division is in charge of auditing the corporate divisions, the companies, branch companies, and affiliated companies. However, in reality the corporate audit division mainly provided consultation services for the 'management being carried out at each of the companies, etc (as part of the business operations audit), and it rarely conducted any services from the perspective of an accounting audit into whether or not an accounting treatment was appropriate." The observations of the committee give the impression that the fault of the internal audit in Toshiba was that it focused on consultation service rather than assurance service. Should internal audit avoid providing consultation service? I do not think so. It was not the fault of the internal audit that it provided consultation service. The fault was that it did not pay attention to accounting audit. In Toshiba, the top management used to set targets that are unachievable. There was excessive pressure from the top management to achieve those targets. The variable pay is a significant portion of the total pay. The compensation of executive officers comprises a base compensation based on title and a role compensation based on work content. Forty per cent to 45 per cent of the role compensation is based on performance of the overall company or business department. 'Challenge' to achieve unachievable targets and performance-based pay provide enough motivation to manage earnings. Therefore, accounting audit should have been a focus area for internal audit. Internal audit can function independently only if the audit committee is capable, independent and effective, and the internal auditor must reports to the audit committee. In Toshiba, the audit committee was neither capable nor independent. The three external members of the audit committee had no knowledge of finance and accounting. An ex-Chief Financial Officer (CFO), who was the CFO during the timeframe when accounting irregularities occurred, was the only whole time member of the audit committee. Therefore, the internal audit was not independent of the management. Earnings management had the tacit approval of the top manar Therefore, it is not surprising that accounting audit was excluded from the 2/3 internal audit. It is incorrect to infer that the accounting audit did not rec. attention of the internal audit because its focus was on providing consultaun service. Contemporary literature defines internal audit as 'assurance and consulting service'. The issue is of balancing between consultation service and assurance service. Problem arises when the internal auditor forgets that the internal audit is primarily an assurance function. The consultation service flows from the assurance service. Although, the primary objective of operation audit is to obtain assurance that the internal control that is installed to achieve operation objectives is adequate and operating effectively, the auditees look to the intermal auditor for suggestions and consultancy. Such consultation service is a by-product of the assurance service. Auditees should not be denied the benefits of internal auditor's understanding of the industry and the business, and the challenges before the auditees in achieving operation objectives. Exclusion of consultation service from the scope of internal audit would result in sub-optimal utilisation of internal audit resources. Organisation culture also determines the effectiveness of internal audit. The investigation committee observes, "A corporate culture existed at Toshiba whereby employees could not act contrary to the intent of their superiors". In such a culture an upright internal auditor cannot survive, particularly if he is not independent of the management. Perhaps, it is the reason that the internal audit in Toshiba had chosen the easy path of focusing on 'consultation service' only without reporting intemal control weaknesses. Internal auditor is the 'eyes and ears' and 'go-to man' of the audit committee. Therefore, internal audit failure leads to corporate governance failure.

Expert Answer:

Answer rating: 100% (QA)

1 Based on my observations I am not satisfy with the competency that is carried by internal audit audit committee because in my analysis I have find o... View the full answer

Related Book For

Auditing a business risk appraoch

ISBN: 978-0324375589

6th Edition

Authors: larry e. rittenberg, bradley j. schwieger, karla m. johnston

Posted Date:

Students also viewed these accounting questions

-

A bond that matures in 17 years has a $1,000 par value. The annual coupon interest rate is 13 percent and the market's required yield to maturity on a comparable-risk bond is 16 percent. What would...

-

Internal controls, an internal audit function, and an audit committee are all elements of a strong corporate governance system. Mow should an external auditor evaluate these elements in making a risk...

-

A college professor can see objects clearly only if they are between 70 and 500 cm from her eyes. Her optometrist prescribes bifocals (Fig. 25.23) that enable her to see distant objects through the...

-

1. Review the six (6) goals of performance based acquisition(s); choose two and discuss how your choices can be implemented for effective management of contracts, using an actual or theoretical...

-

The graph of the acceleration a(t) of a car measured in ft/s is shown. Use Simpson's Rule to estimate the increase in the velocity of the car during the 6-second time interval. 12 4 0 2 4 6 (seconds)

-

You are riding a bus and thinking about the number of passengers on board. (a) Is the number of passengers an extensive or intensive quantity? (b) Draw a system diagram to help account for the number...

-

For the original 4340 steel-reinforced concrete post design of Problem 1.13 and the new IM9 carbon fiber-reinforced concrete post design of Problem 1.16, compare the tensile stress-to-tensile...

-

In an Adecco Staffing survey of 1,000 adults in the United States, 140 (or 14%) said that salary was the most important feature of their job. The sample proportion of 0.14 cannot be a good estimate...

-

John and Mike work in the same department. Mike is a new employee. John has worked at the company for a long time. John and Mike do the same job. They have the same job title. They have to work...

-

Determine the zero-force members in the Pratt roof truss. Explain your answers using appropriate joint free-body diagrams. A B 300 N C 400 N D L K J E F I H 12 m, 6 @ 2 m- 3 m

-

Consider the differential equation: xy" + (3x-1)y' + y = 0 for x > 0. (14a) Show that x = 0 is an irregular singular point of the above differential equation. (14b) Let us, nevertheless, attempt a...

-

Using Figure 11.1, illustrate the probability that someone will obtain insurance for treatment for (a) A hangnail. (b) A broken arm. (c) A bad hair day. (d) Viral meningitis. A. Expected Total...

-

What is a reputation good? What are examples of reputation goods outside the health care sector? Show what Pauly and Satterthwaite predict will happen to the demand curve for health services as a...

-

The use of professional and independent buyer-agents to help individuals purchase automobiles or houses is becoming a more common phenomenon. Given the confl ict of interest facing the...

-

Contrast technical and allocative effi ciency. How can technical and allocative ineffi ciency in health care fi rms affect patient welfare?

-

Why is the depreciation of a capital good a cost to society? In what ways does a persons health depreciate?

-

Each quarter, Carla Vista, Inc., pays a dividend on its perpetual preferred stock. Today the stock is selling at $ 6 4 . 0 0 . If the required rate of return for such stocks is 1 3 . 0 0 percent ,...

-

A non-charmed baryon has strangeness S = 2 and electric charge Q = 0. What are the possible values of its isospin I and of its third component I z ? What is it usually called if I = 1/2?

-

Multiple Choice Questions 1. Which of the following statements regarding the incidence of fraud is incorrect? a. Fraud is estimated to costs U.S. businesses less than 1 cent of every dollar of sales....

-

Why does the auditor examine travel and entertainment expenses? What would poor controls regarding executive reimbursements say about the "tone at the top" for purposes of evaluating and reporting on...

-

It was stated that each account balance contains assertions about the nature of the item reflected on the financial statements. Required Identify the accounting assertions that are contained in the...

-

What is the relation between degrees Fahrenheit and degrees Rankine? And the relation between degrees Celsius and Kelvin?

-

State Newton's second law as you would apply it to a control mass.

-

Explain the significance of \(g_{c}\) in Newton's second law. What are the magnitude and units of \(g_{c}\) in the English Engineering system? In the SI system?

Study smarter with the SolutionInn App